The issue of stressed assets is not new for the power sector. However, developments in the past 12 months have made it imperative for the stakeholders to take immediate steps. With a view to improve credit culture and address the problem of bad loans, the Reserve Bank of India (RBI) issued a circular on February 12, 2018, which withdrew all the traditional debt restructuring schemes and mandated a one-day default in loan repayment as the trigger for the resolution of stressed assets. For the power sector, the new rules meant bringing almost 40 GW of power plants to the brink of insolvency, if they failed to come up with resolution plans by August 2018.

Since then, power producers as well as the power ministry have been lobbying with the central bank to relax the deadline and dilute some of the norms. In a key recent development in September 2018, the Supreme Court stayed RBI’s new guidelines, bringing temporary relief to the sector. Another relief measure was the setting up of a high-powered committee under the cabinet secretary to look into the power sector’s stressed assets in line with the recommendations of the 37th Report of Parliamentary Standing Committee on Energy released in August 2018.

Power Line presents a round-up of the major finance-related developments in the power sector in the past year…

Stressed assets developments

Giving a breather to the stressed power assets, the Supreme Court, on September 11, 2018, stayed RBI’s circular until November 14, 2018, the next hearing date. The court has stated that, in the interim, the status quo will be maintained on all the cases that have been referred to the National Company Law Tribunal, and no new cases will be referred to the tribunal. Besides, the court has directed all the 12 cases related to stressed assets that are pending before different high courts to be transferred to the Supreme Court.

The industry has welcomed the apex court’s decision and a resolution plan for a number of stressed projects is likely to be finalised before the next hearing. Reportedly, the State Bank of India (SBI) hopes to resolve around eight stressed power assets with an exposure of about Rs 170 billion and the Power Finance Corporation (PFC) is likely to save around seven coal-based projects aggregating 10,190 MW.

As identified by the Department of Financial Services in March 2018, there were 34 power projects aggregating over 40 GW of capacity and entailing a cumulative debt of Rs 1,744 billion, that were stressed/non-performing assets. As per the latest news sources, while 14 projects aggregating Rs 550 billion have already been referred to the insolvency court, difficulties in eight more with Rs 350 billion of dues have been resolved.

Earlier, in end August, the Allahabad High Court, which was hearing the plea of power producers on the circular, had rejected the Association of Power Producer’s petition seeking relief for the power sector and directed the central government to follow a consultative approach with RBI. In another petition, the Madras High Court has recently granted a stay on referring for insolvency proceedings IL&FS’s 1,200 MW Cuddalore thermal power plant and RKM Powergen’s 1,440 MW Ucchpinda thermal power plant. The developers (of the plants) had sought extra time to finalise the resolution plan.

The 37th Report of the Parliamentary Standing Committee on Energy, which discusses the impact of the RBI’s circular on the power sector, notes that about 66 GW of conventional energy [including 54,805 MW of coal-based power (44 assets), 6,831 MW of gas-based power (9 assets) and 4,571 MW of hydropower (13 assets)] is facing financial stress to various degrees. The committee notes that the outcomes of RBI’s revised framework with respect to the electricity sector has been very disappointing, with major lenders to independent power producers displaying significant accretion to non-performing assets (bad loans) and their slippages exceeding Rs 1.8 trillion during the period January-March 2018. Besides, debt restructuring for certain projects could attract a haircut of as much as 70 per cent.

The committee also recommended setting up a high-powered committee headed by the cabinet secretary and including representatives from the ministries of railways, finance, power and coal, and lenders with major exposure to look into issues that have contributed to the stress in the sector. Meanwhile, various strategies have also been proposed by banks and power sector financiers in the past few months to address the issue. For instance, SBI has formulated the Scheme of Asset Management and Debt Change Structure (Samadhan) wherein the unsustainable debt would be converted to equity and investors would take 51 per cent equity stake in the project along with the sustainable debt. Besides, the Rural Electrification Corporation (REC) has formulated the Power Asset Revival through Warehousing and Rehabilitation (Pariwartan) scheme wherein an asset warehouse may be established to protect value and revitalise assets.

Debt market updates

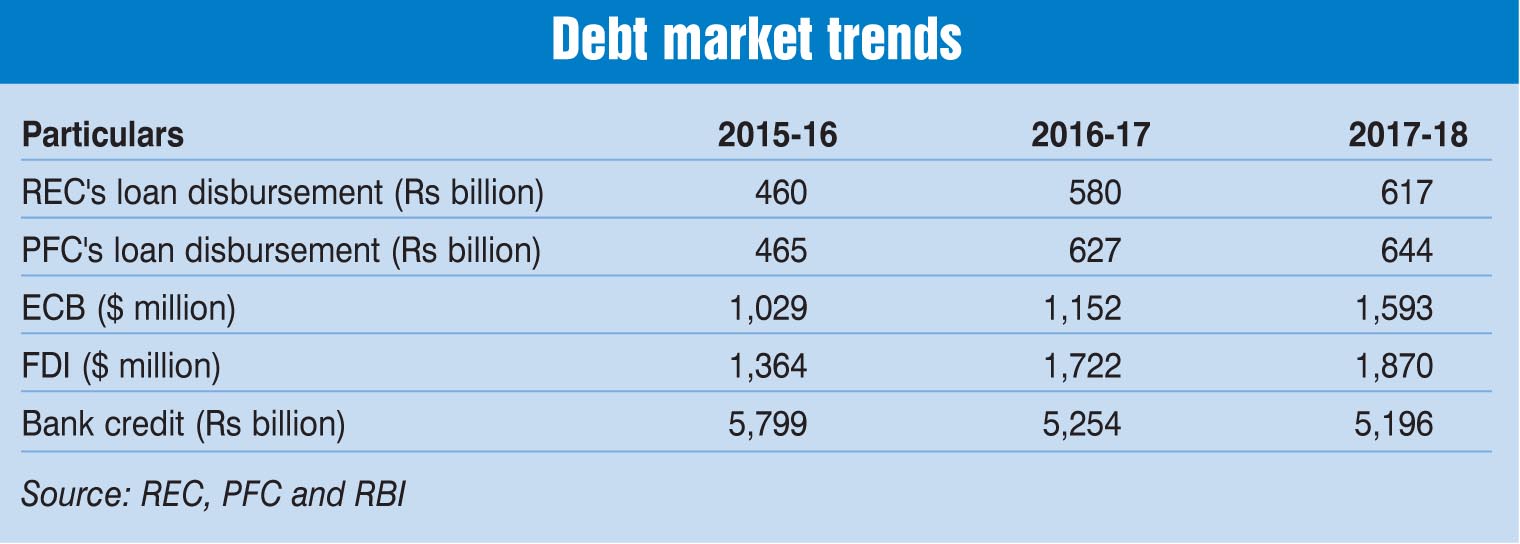

In 2017-18, the loans sanctioned by the key power sector financiers, namely, REC and the Power Finance Corporation (PFC), witnessed an increase of over 15 per cent each on a year-on-year basis.

In 2017-18, REC sanctioned loans worth Rs 1,075.3 billion, recording an increase of 28.2 per cent over the previous year. Meanwhile, during the year, REC’s disbursements stood at Rs 617.12 billion, an increase of 6.3 per cent over the previous year. On the other hand, in 2017-18, PFC sanctioned loans worth Rs 1,162 billion, an increase of 15.54 per cent over the previous year. On the other hand, PFC’s loan disbursements stood at Rs 644.14 billion during the year, marking an increase of 2.57 per cent over the previous year.

With regard to lending by commercial banks to the power sector, as of March 2018, the gross commercial bank credit extended to the sector stood at Rs 5.2 trillion, marking a decline of 1.1 per cent over that in March 2017. On the other hand, between April and July 2018, the banking sector’s exposure to the power sector increased slightly to reach Rs 5.27 trillion, an increase of 1.4 per cent over that in March 2018. Further, as of July 2018, the power sector continues to account for the largest share (19.98 per cent) in banks’ exposure in overall industrial credit (Rs 26.4 trillion).

On the external commercial borrowing (ECB) front, the power companies raised $1,593.94 million in 2017-18, an increase of 38.4 per cent over the previous year. However, between 2013-14 and 2017-18, the ECB by the power companies recorded a negative compound annual growth rate (CAGR) of 13.8 per cent. The declining trend in ECBs in recent years could be attributed to the attractiveness of raising funds through bonds in the overseas market.

For instance, in January 2018, NTPC listed a $6 billion medium-term note programme on the India International Exchange at the International Financial Services Centre in Gujarat, becoming the first Indian quasi-sovereign company to list on the exchange. There has been a steady increase in the foreign direct investment (FDI) inflow into the sector. Between 2013-14 and 2017-18, FDI to the power sector grew at a CAGR of 9.85 per cent to reach $1,870 million. On a year-on-year basis, FDI in the power sector recorded a growth of 8.59 per cent, as against 26.25 per cent in the previous year.

Equity market updates

Equity market updates

The power sector witnessed a number of merger and acquisition (M&A) deals in the past year. One of the biggest M&A deals (in value terms) in the power sector was Adani Transmission Limited’s (ATL) 100 per cent acquisition of Reliance Infrastructure Limited’s electricity generation, transmission and distribution businesses in Mumbai. The total deal value is pegged at Rs 188 billion. The deal, which was announced in December 2017, was completed recently.

In the conventional power generation segment, a key deal was NTPC Limited’s acquisition of Bihar State Power Generation Company Limited’s (BSPGCL) Barauni thermal power station as well as BSPGCL’s stake in its two joint ventures with NTPC – Kanti Bijlee Utpadan Nigam Limited and Nabinagar Power Generating Company (Private) Limited. The deal, valued at Rs 56 billion, entails acquisition of over 3 GW of generation capacity by NTPC.

Apart from this, the renewable energy segment witnessed a number of deals. These included ReNew Power’s acquisition of Ostro Energy in one of the largest renewable deals (for an enterprise value of Rs 108 billion) and Hinduja Power Corporation’s acquisition of Mumbai-based Kiran Energy Solar Power in an all-cash deal of Rs 9 billion-Rs 9.5 billion for 85 MW of operational portfolio. In September 2018, the Canadian pension fund, Caisse de dépôt et placement du Québec, signed an agreement with CLP India Private Limited to acquire 40 per cent stake in the latter for $363.51 million. CLP India’s project portfolio comprises a total generation capacity of 3,000 MW, including renewable energy capacity of 1,000 MW.

The equity market saw the debut of India’s premier power exchange, Indian Energy Exchange (IEX), on the stock exchanges in October 2017. The IEX’s initial public offering (IPO) offered shares of face value of Rs 10 each in the price band of Rs 1,645-Rs 1,650 and was subscribed by 2.28 times on issue closing. Meanwhile, there was a rush for renewable energy IPOs in the year. Sembcorp Energy India [received the approval of the Securities and Exchange Board of India (SEBI) to float a Rs 40.95 billion IPO in August 2018], ReNew Power (received SEBI’s nod for a Rs 26 billion IPO in July 2018) and Indian Renewable Energy Development Agency Limited (filed draft papers with SEBI for the issue of an IPO in December 2017) are some of the renewable energy companies that are lined up to tap the capital market.

Conclusion

To conclude, while the build-up of stressed assets is weighing on the sector, a number of initiatives are under way to tackle the situation. These are also expected to yield lasting results. Deliberations on the issues and challenges facing the power sector by the high-powered committee, and proper implementation of potential solutions are expected to put the power sector back on a growth trajectory.

Priyanka Kwatra