To address the coal supply issues of stressed projects, the power ministry has recently notified a methodology for conducting coal auctions for thermal power projects without PPAs. Industry experts comment on this order and its impact on the sector…

Is the government’s recent decision to allow coal auctions for power plants without PPAs a positive move? Does it adequately address the concerns of the industry?

Rohit Bajaj

The government’s decision will definitely give power plants the much-needed relief as uncertainty in coal availability will go away. So far, power plants without PPAs have been dependent on auctioned and imported coal, which are priced significantly higher than linkage coal. The government’s recent move will also help reduce the price of electricity in the short-term market as well as on the power exchanges. The generators sell power on the exchange platform at a variable cost. If linkage coal is made available to generators without PPAs, the cost of coal would go down, which will bring down the variable cost of generation and thus the price on the exchange will also reduce. Further, power plants will have an accurate visibility of their revenue stream, which will help them in making prudent operational and commercial decisions. This decision is also a step towards deepening the power market and the exchange market. It will benefit the whole ecosystem. The implementation of this decision should also be fast-tracked so that benefits can be realised at the earliest.

Ashok Khurana

The recent decision of the government to allow coal linkage auctions for power plants without PPAs has flowed from the recommendation made by the high-level empowered committee (HLEC) constituted by the government in July 2018 to consider issues related to stressed thermal power projects. The HLEC, chaired by the cabinet secretary, had put forward certain recommendations to improve the financial viability and operational efficiency of stressed generating assets. One of the observations made by the HLEC was that many coal-based power plants have coal linkages in the form of fuel supply agreements (FSAs) or letters of assurance (LoAs), but do not have medium- or long-term PPAs. In the absence of PPAs, they are unable to utilise their coal linkage because linkage coal is not allowed to be utilised for the short-term sale of power. Therefore, the HLEC recommended that there should not be any restriction on the sale of power generated from linkage coal in the short-term market or through the power exchange. The HLEC also recommended that short-term linkage coal (for a minimum period) may be made available to plants without PPAs.

Unfortunately, the government’s decision to allow coal linkage auctions for plants without PPAs does not help the category of plants for which the HLEC recommendation was made, that is, stressed projects that already have linkages but are unable to utilise their linkages. It may be recalled that power plants without PPAs already have an existing avenue for procuring coal – the special forward e-auctions conducted by Coal India Limited (CIL) subsidiaries. Therefore, this announcement of a separate coal linkage auction for plants without PPAs will have a limited positive impact, especially with the restriction imposed by the Ministry of Power (MoP) that only plants with untied capacity of more than 50 per cent of installed capacity will be eligible for the auctions. What is really required is to completely remove the end-use restriction for linkage coal. It may be noted that when coal linkages were awarded, there was no end-use restriction. This condition was introduced later to restrict the access to coal in view of the large amount of linkages sanctioned by the standing linkage committee (long term) without taking into account the production capacity of CIL and its subsidiaries.

T.N. Arun Kumar

Apart from delays in payment by power distribution companies, a critical issue in the power sector has been the shortage of coal supply. As per former power secretary S.C. Garg, investment worth Rs 5 trillion is at risk due to coal scarcity. Against this backdrop, the government’s recent decision to allow coal auctions for power plants that do not have PPAs is a positive one. The move is part of the amendments to the SHAKTI policy. According to the latest guidelines, the said auctions will be carried out every quarter and the power company offering the highest premium over the notified price of CIL will sign the FSA for three months. The power generated through this linkage is to be sold in the day-ahead market through the power exchanges or in the short-term market under a transparent bidding process through the DEEP portal. The move is likely to ease the cash flow situation of commissioned plants that are supplying power in the short-term market and do not have access to coal. Also, as per the scheme, the net surplus generated by a company (using such coal) is to be used for meeting its debt service obligation. It is likely to aid the debt servicing capability of the entity. Thus, seen in conjunction with the previous rounds of SHAKTI auctions, the scheme has tried to address some concerns of the industry. However, a multi-pronged sustained strategy will be required to steer the sector out of stress.

Sabyasachi Majumdar

The provision of domestic linkage coal against short-term PPAs remains positive for the power generation segment, especially for about 15 GW of operational coal-based capacity that does not have long-term PPAs. As per the approved methodology, power plants availing of coal under this linkage are required to sell power generated either through the day-ahead market on the power exchanges or under short-term contracts, wherein the tariff was discovered through the DEEP portal as per the guidelines issued by the MoP. Such coal linkages will be allocated through an auction process with a premium quoted over the CIL-notified price as the bid parameter.

While this measure will enable stressed coal-based capacities to run projects under short-term PPAs using linkage coal, the availability of adequate working capital funding remains crucial to operate such projects. Also, profitability under these PPAs remains sensitive to the quoted premium on the notified coal prices and tariffs in the short-term market given the subdued tariff rates at the power exchanges, following the slowdown in the electricity demand growth. The all-India electricity demand growth declined to 1.2 per cent in the first eight months of FY 2020 on a year-on-year basis against the 6.4 per cent growth reported in the corresponding period of FY 2019. This can be attributed to low demand from households and the agricultural segment following higher-than-usual rains during August-October 2019 and moderate demand from the industrial segment. The reduced demand for thermal power generation has led to a decline in the plant load factor in FY 2020. Apart from policy measures, the revival of electricity demand remains crucial for the resolution of stressed assets. The coal production of CIL declined by 8.5 per cent in the first seven months of 2019-20, on a year-on-year basis. However, the impact of this decline on thermal power generation remains limited so far given the slowdown in electricity demand growth as well as higher supply from other generation sources like hydro, nuclear and renewables. As a result, coal stock levels at thermal power stations remain higher on a year-on-year basis. However, the revival of domestic coal production remains crucial to reduce the dependence on coal imports and enable power generation companies to offer competitive tariff rates in the long-term and short-term markets.

Dr. S.L. Rao

The decision will certainly benefit the industry a great deal because developers do not have to wait to see how the business is going and they can buy and stock coal as they wish. This also means that they can take advantage of low prices. I am not so worried about their ability to buy and hold stocks as I am about the fact that this is further encouragement for using coal. I think the broader pattern of the Indian energy market in the future will be defined by less use of coal and more use of renewables, gas, etc. We should put in a great deal of effort and money on finding fresh sources of gas and new ways to produce and store more cheap renewable energy. Coal will always be important for generators because with coal a substantially large quantity of power can be continuously generated without having to worry about availability. That said, coal has a very serious negative impact on the environment and we are going to come under tremendous pressure in the coming years from the rest of the world against the use of coal. Hence, any policy that encourages the use of coal is not in the best interest of the country in the long term.

What must be the other immediate policy priorities related to fuel supply to put the stressed projects back on track?

Rohit Bajaj

Another priority should be fast-tracking commercial mining. Unless the availability of coal increases, the benefits will not get passed on to consumers. Commercial mining of coal will increase coal availability and help bring down the cost of power generation.

Ashok Khurana

It is high time for a serious reconsideration of the SHAKTI framework for coal allocation. It was introduced on May 22, 2017, and prior to this, the coal allocation policy was governed by the New Coal Distribution Policy (NCDP). The NCDP, which had a single stream for allocation, treated all projects equitably and it stated that CIL will meet the full normative requirement of coal for power producers. These distinguishing features have been removed in the SHAKTI policy. Unlike its predecessor, the SHAKTI policy introduced differentiation in allocation and pricing mechanisms on the basis of ownership of the power plant. For PSU gencos, the SHAKTI scheme continues with the practice of allocation on the notified price based on nomination/recommendation from the MoP. For independent power producers (IPPs) though, it abolishes the earlier linkage allocation process and creates multiple categories of plants while prescribing different methods of auction (with eight variants and five sub-variants), thereby turning a simple allocation process into a complex and confusing web of different modalities.

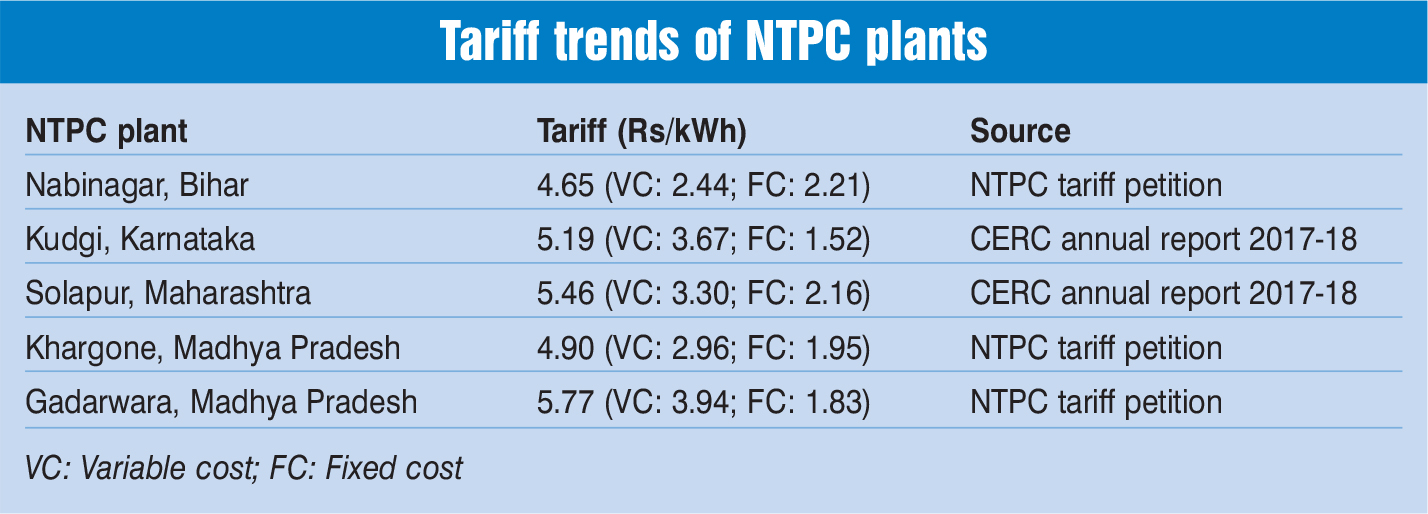

By virtue of this preferential treatment to PSU generators, 10-12 GW of recently commissioned and more efficient private generation capacity is currently lying unutilised due to the lack of coal while coal that could have generated cheaper power from these plants is instead being supplied to more expensive and inefficient PSU gencos. The accompanying table illustrates that all the recent NTPC plants have higher tariff than the tariff discovered under the recently held pilot Scheme II bid (Rs 4.41 per kWh). This is despite the many risk factors associated with the pilot Scheme II tender such as lack of coverage for coal linkage deficit, coal grade slippage, low materialisation of coal supply and the risk of curtailment of fixed charges depending on the demand variation of the utility. Apart from the preferential allotment of coal, the PSU plants enjoy preferential supply from CIL, priority in coal transportation through rail, permission to pool and divert coal, and preferential payment terms. Therefore, an immediate policy priority should be the removal of the discriminatory framework to make fuel supply efficient and ownership-neutral.

T.N. Arun Kumar

The government should expeditiously implement the recommendations of the HLEC (November 2018) to address the issues of stressed thermal power plants in the short to medium term. A few of the committee’s recommendations included continued coal supply in case of termination of the PPA due to default by the discom, increase in the quantity of coal for special forward e-auction for the power sector, etc. In the medium to long term, the commercialisation of coal mining will have a far-reaching impact in terms of improvement in coal availability. The government has allowed 100 per cent FDI under the automatic route and expects a few large global coal miners to be a part of the coal value chain. The FDI in commercial coal mining will facilitate the much-needed investments in the coal sector and bring new technologies and mechanisation to the sector. This should help provide adequate coal supplies to stressed power plants, which are otherwise dependent on CIL and its subsidiaries.

Dr. S.L. Rao

Dr. S.L. Rao

The most important thing is gas. We have a very significant amount of gas-based capacity that is lying unutilised due to unavailability. The government allowed investment in gas-based plants on the assumption that gas will be available. This is a very serious mistake because suppliers such as Reliance Industries Limited that had earlier expected to find a great deal of gas, later said that there is no gas available. We now have a substantial amount of money locked up in that unused capacity. Hence, we must first ensure availability of gas. I don’t think we are doing enough to search for gas and we need to do that. The second area of priority is renewable energy, where we are making good progress. However, we need to spend a lot of money to be able to store the energy since renewable energy depends on the sun and the wind and there are times when there is no energy being generated. The third thing is the use of renewable energy. We need to do everything possible to conserve energy and use less so that the energy can be used more efficiently.