Nuclear power contributes roughly around 3 per cent of India’s total power generation and less than 2 per cent of installed capacity. Despite starting operations in 1969, the nuclear power segment has failed to take off significantly in India. To meet its commitment under the Paris agreement, India is aiming for 40 per cent of its installed capacity to be based on non-fossil sources such as nuclear, hydro and renewables by 2030. The government has set an ambitious target to increase India’s nuclear capacity from 6.7 GW at present to 22.4 GW by 2031. An overview of the nuclear power segment in the country…

Capacity and generation trends

As of April 2020, India has 22 nuclear reactors, with an installed nuclear capacity of 6,780 MW, held by central sector genco Nuclear Power Corporation of India Limited. India has a largely indigenous nuclear power programme. Due to earlier trade bans and lack of indigenous uranium, India has developed a unique nuclear fuel cycle to exploit its reserves of thorium. Of its total capacity, 14 reactors with an installed capacity of 4,280 MW are under International Atomic Energy Agency safeguards and use imported fuel. The remaining eight reactors with an installed capacity of 2,400 MW use indigenous fuel.

The total installed capacity is distributed across seven plants. These are the 1,400 MW Tarapur Atomic Power Station in Maharashtra, the 1,180 MW Rajasthan Atomic Power Station, the 2,000 MW Kudankulam Nuclear Power Project in Tamil Nadu, the 880 MW Kaiga Generating Station in Karnataka, and the 440 MW each Madras Atomic Power Station in Tamil Nadu, Narora Atomic Power Station in Uttar Pradesh and Kakrapar Atomic Power Station in Gujarat. During 2016-17, 1,000 MW of nuclear capacity was added in March, when the second unit at Kudankulam began operations. However, between March 2017 and March 2020, there was no capacity addition in the segment. As per the CEA, nuclear capacity addition of 700 MW was targeted for 2019-20, which has not been met. In 2019-20, gross nuclear power generation increased by 22.66 per cent, from 37.8 BUs in 2018-19 to 46.38 BUs in 2019-20. The capacity and availability factors of nuclear power plants in 2019-20 (up to February 2020) stood at 82 per cent and 88 per cent respectively, as against 70 per cent and 73 per cent during 2018-19.

Upcoming projects

Upcoming projects

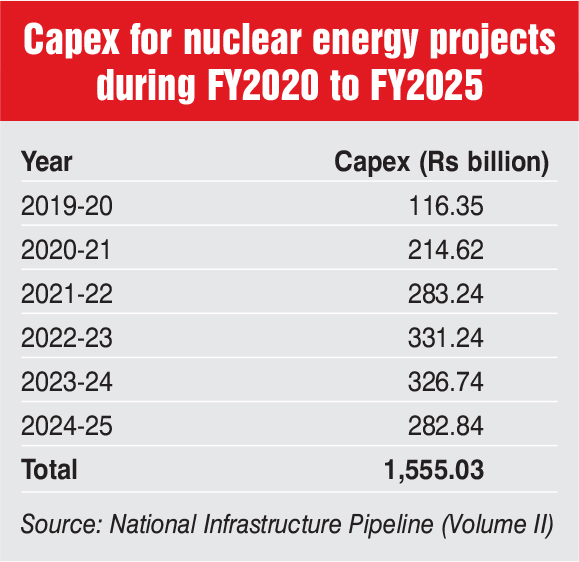

Currently, a total of nine nuclear power reactors with an aggregate capacity of 6,700 MW are under construction. These are Units 7 and 8 of the Rajasthan Atomic Power Station (2×700 MW) at Rawatbhata, Units 3 and 4 of the Kakrapar Atomic Power Station (2×700 MW) in Gujarat, Units 3 and 4 of the Kudankulam Nuclear Power Station (2×1,000 MW) in Tamil Nadu, Units 1 and 2 of the Gorakhpur Haryana AnuVidyutPariyojna (GHAVP) (2×700 MW) in Haryana, and a 500 MW prototype fast breeder reactor at Kalpakkam, Tamil Nadu, being implemented by BHAVINI, a PSU of the Department of Atomic Energy.

In addition, the government has granted administrative approval and financial sanction for setting up 12 more nuclear power reactors with a total capacity of 9,000 MW. These are Units 1 and 2 at Chutka, the Madhya Pradesh (2×700 MW), Units 5 and 6 at Kaiga in Karnataka (2×700 MW), Units 1, 2, 3 and 4 at MahiBanswara in Rajasthan (4×700 MW), Units 3 and 4 of the GHAVP in Haryana (2×700 MW), and Units 5 and 6 of the Kudankulam Nuclear Power Station in Tamil Nadu (2×1,000 MW). Of these, one of the marquee projects identified by the government is the Kudankulam Nuclear Power Project Units 3, 4, 5 and 6, which are being built at an estimated total project cost of Rs 894.7 billion and are expected to be completed by December 2025.

The government has also granted in-principle approval for setting up nuclear power reactors at the following sites – Units 1 to 6 of 1,650 MW each at Jaitapur (Maharashtra), Units 1 to 6 of 1,208 MW each at Kovvada (Andhra Pradesh), Units 1 to 6 of 1,000 MW each at ChhayaMithiVirdi (Gujarat), Units 1 to 6 of 1,000 MW each at Haripur (West Bengal), and Units 1 to 4 of 700 MW each at Bhimpur (Madhya Pradesh).

Outlook and the way forward

As per the CEA’s draft report on the optimal generation capacity mix for 2029-30, it is likely that the installed capacity by the end of 2029-30 will be around 831,502 MW, of which 16,880 MW will come from nuclear. It further expects that the projected gross electricity generation during 2029-30 is likely to be 2,508 BUs, with nuclear power accounting for 101 BUs.

Nuclear power development in India has suffered multiple setbacks in recent years due to strong public opposition, liability issues and the interpretation of the Civil Liability Nuclear Damage Act by foreign and domestic suppliers. Going forward, the risk perception of suppliers will determine future development in the sector.

Nikita Gupta