To achieve climate-resilient economies, financial resources need to be directed towards environment-friendly projects and activities. Therefore, as green finance gains traction in the public and private sectors across global economies, the Reserve Bank of India (RBI) has announced plans to establish a framework for the acceptance of green deposits.

As a financial instrument, a “green deposit” is an interest-bearing deposit received by regulated entities (REs) for a fixed period. The proceeds from these deposits would be used for green financing, which involves lending and investing in projects that address climate risk mitigation and other climate-related or environmental goals.

This initiative has been promoted by RBI as deposits are a major source for mobilising funds by REs in India. The REs listed by RBI include banks, primary cooperative banks, non-banking financial companies, credit information companies and institutions such as the Exim Bank, NABARD, NBFID, the National Housing Bank, and the Small Industries Development Bank of India. Private banks in India such as HDFC bank, IndusInd Bank, Federal Bank, DBS Bank and HSBC are already offering green deposits.

Green deposits not only help investors achieve their sustainability goals, but also provide stable principal and predictable returns. They are placed through a process similar to that of a regular term deposit.

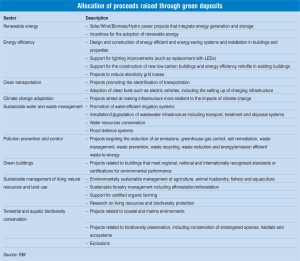

The concept of green deposits is based on banks providing loans to fund projects in various fields such as energy efficiency, renewable energy, clean transportation, waste management, greenhouse gas reduction, sustainable agriculture and natural resource management. As such, they offer businesses an easy and low-cost way to participate in the environment, social and governance (ESG) movement. RBI’s framework for green deposits will come into effect from June 1, 2023.

Key highlights

The following are the key features of the framework highlighted by RBI for green deposits:

- Denomination, interest rates and tenor of deposits: REs will issue green deposits as cumulative or non-cumulative deposits. On maturity, green deposits can be renewed or withdrawn by the depositor and will be denominated in Indian rupees only. The tenor, size, interest rate and other terms and conditions of these deposits will be applicable to REs as defined in the RBI Master Directions on Interest Rate on Deposits.

- Policy and financing framework: REs will put in place a comprehensive board-approved policy on green deposits, covering all aspects of their issuance and allocation. Also, REs will establish a board-approved financing framework for the effective allocation of green deposits.

- Third-party verification and impact assessment: The allocation of funds raised through green deposits by REs during a financial year will be subject to an independent third-party verification on an annual basis. However, this verification does not relieve an RE of its responsibility for ensuring the appropriate end-use of the funds.

- Reporting and disclosures: A review report will be presented by the RE to its board of directors within three months of the end of the financial year. It will cover details such as the amount raised under green deposits during the previous financial year, a list of green activities and projects to which the proceeds have been allocated, the amounts allocated to eligible projects, and copies of the third-party verification report and impact assessment report.

Outlook

According to RBI, there has been progress in public awareness and financing options related to green investments in India. However, some challenges remain, such as high borrowing costs, false claims of environmental compliance, a multitude of green loan definitions, and maturity mismatches between long-term green investments and investors’ relatively short-term interests. Furthermore, most ESG investing alternatives expose investors to the volatility and potential loss of principal associated with the securities markets. Therefore, green deposits function similarly to standard bank deposits. They may incentivise REs to offer them to consumers, protect depositors’ interests, assist customers in reaching their sustainability goals, address greenwashing concerns, and help increase credit flow to green activities and projects.

Going forward, it is essential to adopt integrated policy approaches to promote green finance and achieve the decarbonisation goals of the government, corporates, public sector companies and other entities.

Nikita Choubey