India’s power sector is undergoing a transformative phase, characterised by surging power demand, substantial investments, and a significant shift towards sustainable energy solutions. In 2022-23, the sector witnessed a remarkable surge in cumulative disbursements and sanctions, primarily fuelled by the resumption of projects that were stalled due to Covid-19 restrictions. This surge, toalling a staggering Rs 1,826 billion, demonstrates India’s resilience and determination in meeting its growing energy requirements. Notably, initiatives taken by the Power Finance Corporation (PFC) and REC Limited played a pivotal role in sustaining this momentum, with substantial loans granted, particularly in the renewable energy sector.

India’s power sector is undergoing a transformative phase, characterised by surging power demand, substantial investments, and a significant shift towards sustainable energy solutions. In 2022-23, the sector witnessed a remarkable surge in cumulative disbursements and sanctions, primarily fuelled by the resumption of projects that were stalled due to Covid-19 restrictions. This surge, toalling a staggering Rs 1,826 billion, demonstrates India’s resilience and determination in meeting its growing energy requirements. Notably, initiatives taken by the Power Finance Corporation (PFC) and REC Limited played a pivotal role in sustaining this momentum, with substantial loans granted, particularly in the renewable energy sector.

Amid this growth, India is embracing a green future. Investments in clean energy, particularly in renewables, have attracted significant attention, with FDI in the renewable energy sector reaching an all-time high of $2.5 billion. The government’s issuance of sovereign green bonds (SGBs) further reinforced this commitment, providing a unique avenue for funding eco-friendly projects. As India charts its path towards a net-zero emissions future by 2070, innovative financing models and efficient fund allocation will be imperative going ahead.

Power Line takes a look at the key trends and developments in the power financing segment over the past year…

Debt market trends

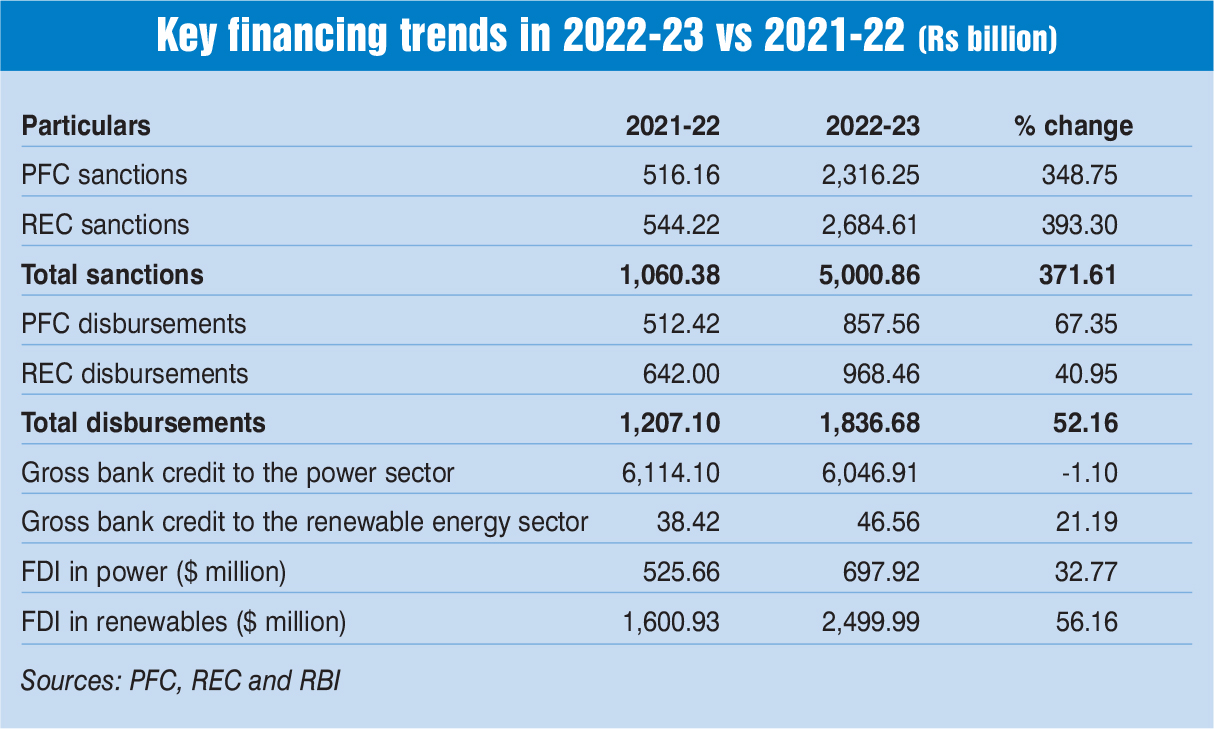

In 2022-23, the cumulative disbursements by PFC and REC amounted to nearly Rs 1,826 billion, an increase of over 58 per cent over the Rs 1,154 billion recorded in the previous year. The cumulative sanctions also witnessed a significant growth of 372 per cent, from Rs 1,060 billion in 2021-22 to Rs 5,001 billion in 2022-23. The increase in sanctions and disbursements can be attributed to the commencement of work at several power projects that had previously witnessed delays or had been put on hold due to the Covid-19 pandemic. The pandemic disrupted many construction and infrastructure projects across the world, including those in the power sector. As restrictions were lifted and economic activities resumed, there was a surge in electricity demand, necessitating investment in power generation and distribution infrastructure. Therefore, the increase in sanctions and disbursements can be seen as a sign of economic recovery and concerted efforts to meet the country’s growing power requirements.

On a year-on-year basis, REC’s disbursements increased by 51 per cent to reach Rs 968.46 billion and PFC’s disbursements increased by 67 per cent to reach Rs 857.56 billion in 2022-23. During the year, REC sanctioned loans worth about Rs 2,684 billion, recording an increase of 393 per cent over the previous year, while PFC’s sanctions increased by 349 per cent to Rs 2,316.25 billion. Further, loans to renewable power projects constituted eight per cent of the total loans sanctioned by REC in 2022-23. PFC’s gross loan assets included Rs 481.98 billion in renewable energy, with Rs 162.51 billion allocated to large hydro projects (>25 MW) and Rs 319.47 billion for projects other than large hydro.

In terms of sectoral deployment of bank credit, loans to the power sector stood at Rs 6,143.06 billion as of August 2023, compared to Rs 6,211.93 billion in August 2022, a decline of 1.1 per cent. Further, bank credit to the renewable energy sector, which comes under priority sector lending, increased by 12 per cent, from Rs 42.53 billion to Rs 47.66 billion during the same period.

Clean energy investments

Major investment deals were witnessed in the renewable energy space, as foreign investors seek a share in the high-growth Indian renewables market. FDI in the renewable energy sector stood at $2.5 billion in 2022-23, marking an increase of 56 per cent over the $1.6 billion recorded in the previous year. This is the highest FDI recorded in the renewable energy sector in a single year. The cumulative FDI inflow in the renewable energy sector stood at $13.3 billion from April 2020 to March 2023. Meanwhile, FDI in the conventional power sector increased by a modest 32.76 per cent from $525 million to $697 million.

As per a recently released report titled “India’s Energy Transition Pathways: A Net-zero Perspective” by the Federation of Indian Chambers of Commerce and Industry and Deloitte, India’s journey towards achieving net-zero emissions between 2022 and 2070 will come at a substantial cost of $15 trillion. While the report estimates the average annual spend at $300 billion, it emphasised that a significantly higher outlay will be required in the initial years. Thus, it recommends innovative financing models to attract private investment into the market and bridge the funding gap.

The renewable energy sector presents new and emerging opportunities. On the energy supply side, investment is required to develop renewable capacity and associated evacuation infrastructure (development of hydro and nuclear capacity, and energy storage systems, including pumped and battery storage systems). On the demand side, investment is required to enhance energy efficiency, and develop green hydrogen and carbon capture, utilisation and storage infrastructure in the industry sectors. In the transport sector, investment would be required to transition to low-carbon powertrain, develop electric vehicle charging infrastructure, and build transport infrastructure to enable a modal shift. Channelising public and private finance to fund the capex required for the transition is imperative. However, securing the necessary funds and ensuring their efficient allocation while maintaining the country’s fiscal discipline remain critical hurdles on the path to energy transition.

Over the years, domestic clean energy companies have successfully secured significant funds, both debt and equity, to support their expansion strategies. In terms of debt financing, Indian firms have actively issued green and sustainability-linked bonds and loans. On the equity front, the sector has witnessed a growing interest from mature, long-term passive investors.

Growing focus on green bonds

To achieve its net zero goals, India is focusing on generating additional global financial resources. To lower the carbon emissions of the economy, the union budget for 2022-23 announced the issuance of SGBs. As highlighted by the International Capital Market Association, a green bond differs from a regular bond as it commits to deploy funds raised solely for financing or re-financing “green” projects, assets, or business activities. In February 2023, the Indian government concluded the sale of Rs 160 billion in SGBs. The first tranche was released in January 2023, raising a total of Rs 80 billion. Of this, Rs 40 billion was raised for a five-year tenor (2028) at a yield of 7.1 per cent. The remaining Rs 40 billion was issued for a 10-year tenor (2033) at a yield of 7.29 per cent. The second tranche, totalling Rs 80 billion, was released in February 2023, divided into two tranches of Rs 40 billion each. The tenor and yield were the same as in the first tranche.

A key highlight was that the yield was a few basis points lower than government securities of the same tenor. A lower yield signifies that the green bonds carried a premium – commonly referred to as “greenium” for green bonds – thus increasing the price of the security. The Reserve Bank of India (RBI) set the cut-off yields for the two bonds at 7.23 per cent and 7.29 per cent respectively. These proceeds will be used to fund public sector projects that reduce the economy’s carbon intensity. A green finance working committee, formed by the Ministry of Finance, will select the government projects that will receive green financing and assist in project evaluation and selection. Under the committee’s supervision, an annual report will be published on the allocation of proceeds to eligible projects, the description of projects financed, the status of implementation and unallocated proceeds. The proceeds from the sale of green bonds will be deposited in the Consolidated Fund of India. The Public Debt Management Cell will track the proceeds and monitor the funds allocated to eligible green expenditures.

The way forward

The outlook for investment in the Indian power sector remains robust and promising. India’s growing population and expanding economy continue to drive electricity demand, necessitating substantial investments in generation, transmission and distribution infrastructure. The government’s emphasis on renewable energy sources has attracted significant investments in clean energy projects. Further, efforts to improve grid reliability and efficiency, along with electrification initiatives in rural areas, create ample opportunities for both domestic and foreign investors.

However, regulatory hurdles and discoms’ financial viability issues need to be addressed to unlock the potential of investments in the Indian power sector. Despite these challenges, the sector remains an attractive destination for investors due to its long-term growth potential and the country’s commitment to sustainable energy solutions.

Akanksha Chandrakar