The nuclear power generation segment in India has witnessed slow growth until now. However, recent developments, including the government’s aim to secure $26 billion in private investment, indicate that there could be winds of change ahead. This is driven by a greater interest in exploring the use of small modular reactors (SMRs) and an overall increased focus on the sector. It is anticipated that new nuclear power projects will be carefully planned to balance the interests of all stakeholders.

Notably, nuclear power has a significant role to play in the energy transition. It stands out as one of the energy technologies with the lowest greenhouse gas emissions, producing only 15 gm of carbon dioxide equivalent per kWh over the entire lifecycle of a plant. In addition, nuclear power serves as a crucial baseload source of power generation, especially in view of the growing renewable energy generation. With the emergence of advanced nuclear reactors such as SMRs, new opportunities in nuclear energy are expected to come to the fore. In the future, nuclear power could play a major role in producing hydrogen because it is clean energy.

Current capacity

India currently has an installed nuclear power capacity of 8,180 MW. Most recently, in 2023-24, the 1,400 MW Kakrapar Atomic Power Project Units 3 and 4 (KAPP 3 and 4) in Surat, Gujarat, have been added to the country’s fleet of commissioned nuclear power plants. These pressurised heavy water reactors (PHWRs) (700 MW each) were indigenously designed, constructed and commissioned, and are India’s first indigenously developed nuclear power reactors. The country’s largest nuclear power plant, the 2,440 MW Kudankulam Nuclear Power Plant (KKNPP) located in Tamil Nadu, accounts for 24 per cent of the total nuclear capacity. India’s nuclear power plants are completely owned by Nuclear Power Corporation of India Limited (NPCIL), which is 100 per cent owned by the government and operates under the administrative control of the Department of Atomic Energy (DAE).

In terms of power generation, in 2023-24, nuclear generation has risen 4.6 per cent to 47,971 MUs compared to 45,855 MUs in the previous year. NPCIL’s generation performance has been supported by fuel tie-ups with domestic and international players. It relies on domestic and imported uranium for its plants, which have been placed under the International Atomic Energy Agency’s safeguards, ensuring smooth operations.

Recent developments

Recent developments

Private investment: For the first time, the government is expected to invite private investment of approximately $26 billion in its nuclear energy sector. Reliance Industries Limited, Tata Power Company Limited, Adani Power and Vedanta Limited are among the private companies that are reportedly in discussions to invest around Rs 440 billion each ($5.3 billion) in the sector. With the investments, 11,000 MW of new nuclear power generation capacity is expected to be built by 2040. Regarding the operating model, it is expected that while the private companies will invest, acquire land and water, and undertake construction outside the reactor complex, the rights to build the reactors, run the stations and manage fuel will remain with NPCIL. Under this unique hybrid model, the private companies are expected to generate revenue from the power plant’s electricity sales and NPCIL would operate the plant for a fee.

Foreign collaborations: India is in discussions with Russia’s Rosatom State Atomic Energy Corporation for the construction of high capacity nuclear power units at a new site in the country, in addition to the under-construction atomic power project at Kudankulam in Tamil Nadu. Rosatom has also expressed willingness to support India in the implementation of land-based and floating low-power nuclear generation projects as well as to collaborate on the nuclear fuel cycle area and on non-power applications of nuclear technologies. Earlier, in December 2023, India and Russia signed an agreement for the construction of future units at the Kudankulam Nuclear Power Plant, which is being set up in collaboration between the two countries. Two Russian VVER 1,000 MWe pressurised water reactors are operational at the site, while four units are currently under construction in two phases, and two more units have been proposed for the fourth phase of the plant. Apart from this, India is also in discussions for deploying SMRs in the country.

Recently, in April 2024, NPCIL and France’s EDF initiated discussions on the financing mechanism and localisation of components for the upcoming 9,900 MW Jaitapur Nuclear Power Psroject in Maharashtra. To recall, in 2016, EDF and NPCIL had signed an agreement for developing the project, and later in 2020, EDF had submitted the techno-commercial offer. As per the agreement, EDF will supply six European pressurised reactors of 1,650 MW each for the project. In another development, in 2023, India and France agreed to collaborate on setting up low-and medium-power modular reactors, including SMRs, and advanced modular reactors, furthering the previously established agreement for the development of nuclear technologies.

Other developments

Anushakti Vidhyut Nigam Limited, a joint venture (JV) of NTPC Limited and NPCIL, has announced plans to invite bids for the development of the 2,800 MW Mahi-Banswara Rajasthan Atomic Power Project (MBRAPP) Units 1-4 in Rajasthan in this fiscal. The JV company will initially develop two PHWR projects – the 2×700 MW Chutka Atomic Power Project in Madhya Pradesh and the MBRAPP – which were identified to be developed under the fleet mode.

In the nuclear energy space, SMRs are expected to play a significant role in the energy transition. NTPC is in discussions with American, French and Russian companies for collaborating on the development of SMRs. The company is also exploring installing SMRs on retired coal-based power plant sites. In another development, in April 2024, Indian Oil Corporation Limited entered into discussions with NPCIL for setting up SMRs at its refineries to meet its energy needs. Further, Neyveli Lignite Corporation India Limited is in discussions with NPCIL for setting up SMRs at its coal mines.

Capacity addition projections

Capacity addition projections

Based on the National Electricity Plan prepared by the Central Electricity Authority, the installed nuclear power capacity is expected to be 13,080 MW by 2027 and 19,680 MW by the end of 2031-32, constituting roughly 2 per cent of the total installed capacity. The share of nuclear in the country’s gross power generation by 2031-32 is projected to be 4.4 per cent or 117.6 BUs.

Currently, there is a pipeline of over 14,000 MW under construction and another 32,000 MW at various stages of pre-construction. These projects are expected to be built primarily by NPCIL and its JVs with other public sector undertakings such as NTPC, involving large reactors and entailing an estimated cost of Rs 120 million-Rs 150 million per MW.

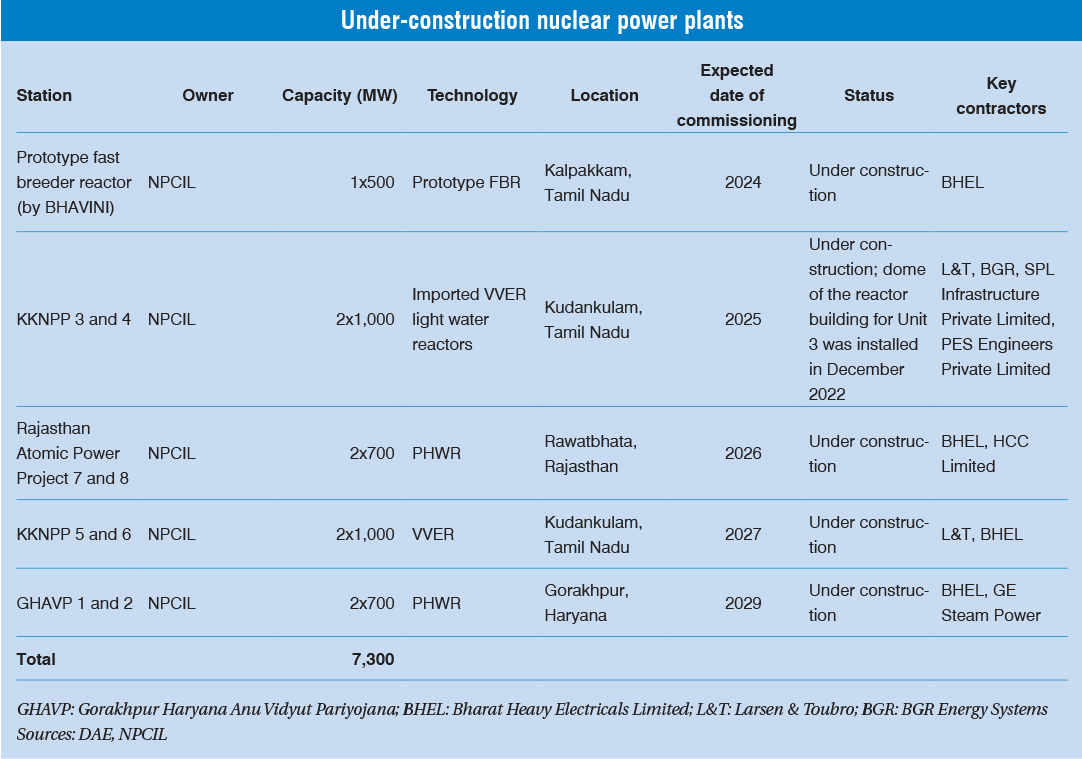

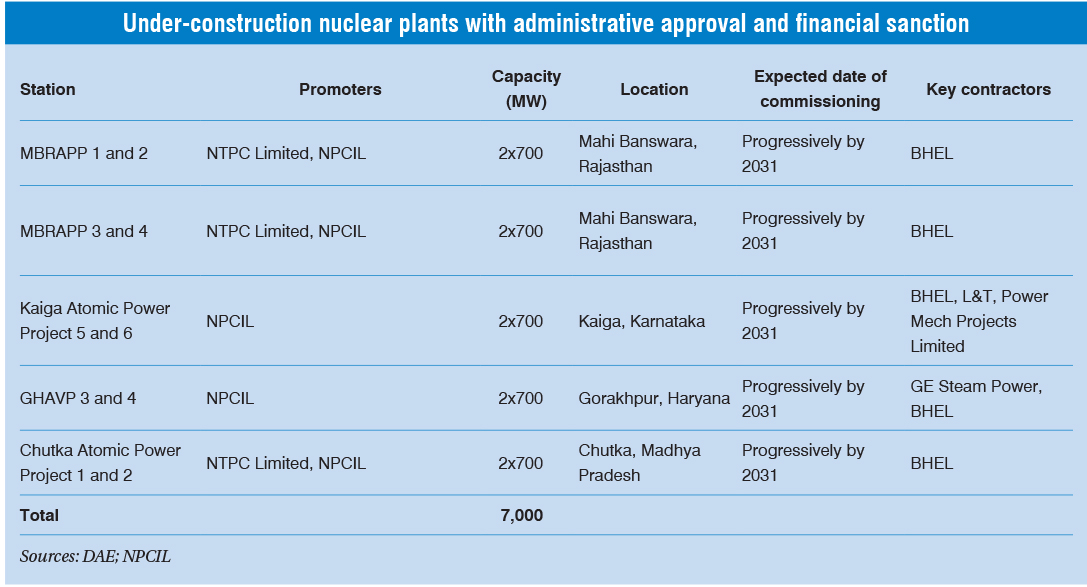

Of the under-construction plants, five nuclear plants aggregating 7,300 MW are expected to be progressively commissioned till 2029. Meanwhile, for another five nuclear power plants aggregating 7,000 MW, administrative approval and financial sanction have been granted and are slated to be commissioned progressively by 2031 (see Table).

With regard to the upcoming projects, the government has granted in-principle approval for setting up nuclear power plants at five new sites in the future. This is to facilitate the early launch of projects. These projects total approximately 30 MW of capacity. Furthermore, the nuclear power pipeline is expected to increase with the adoption of SMRs. Approximately eight to ten SMRs are expected to be built annually at ageing thermal power plant sites within the next four to five years, incorporating an element of localisation.

To conclude, measures such as private funding in the nuclear energy sector and production-linked incentive schemes for SMRs will aid in achieving India’s target of 50 per cent non-fossil fuel capacity by 2030. However, addressing challenges related to supply chain, manufacturing, project risk and public resistance is crucial to accelerate the growth of the segment.