The pumped storage segment has received significant focus over the past few years, with the announcement of conducive policies and a surge in interest from public and private companies. This interest can be mainly attributed to the increasing integration of intermittent renewable energy into the grid and the seasonal fluctuations in energy demand, which has necessitated the uptake of energy storage solutions. Pumped storage projects (PSPs) have become promising, given their reliability and cost-effectiveness in the long run without the need for sourcing critical raw materials.

The pumped storage segment has received significant focus over the past few years, with the announcement of conducive policies and a surge in interest from public and private companies. This interest can be mainly attributed to the increasing integration of intermittent renewable energy into the grid and the seasonal fluctuations in energy demand, which has necessitated the uptake of energy storage solutions. Pumped storage projects (PSPs) have become promising, given their reliability and cost-effectiveness in the long run without the need for sourcing critical raw materials.

The conversation around increasing the adoption of PSPs has become central, as this technology aids in load levelling, peak load sharing and maintaining the stability of the power grid during periods of fluctuating demand and supply. India is currently exploring off-river storage systems due to their significant advantages, such as lower capital costs, round-the-clock (RTC) operational efficiency, no requirement for river diversion, more site options, shorter construction periods (two to three years) and minimal environmental impact. To this end, the government is currently assessing the potential for off-river PSPs.

As per the Central Electricity Authority (CEA), India has eight on-river PSPs, with a total capacity of 4,745.6 MW as of May 2024, installed in various locations across the country, including two each in Telangana, Maharashtra and Gujarat, and one each in Tamil Nadu and West Bengal. However, only six plants, with a combined installed capacity of 3,305.6 MW, are operating in pumped mode, while the remaining 1,440 MW across two sites in Gujarat are not currently functioning in pumped mode. Further, there are three on-river PSPs under construction with a total capacity of 2,850 MW, and construction on one 80 MW on-river PSP is held up. The off-river 1,200 MW Pinnapuram project is also under construction. The detailed project report (DPR) for the on-river Turga project (4×250 MW) in West Bengal has been approved by the CEA. Currently, survey and investigation is in progress for 39 projects totalling 55,930 MW. Of these, four projects of 5,940 MW are on-river projects and 35 projects of 49,990 MW are off-river projects.

Cost economics

For storage cost to be economically viable for the PSP offtaker, it is essential that the cost of storage is lower than the difference between peak and off-peak electricity rates. As per ICRA Limited, the storage cost, which includes energy loss during conversion, is expected to be in the range of Rs 4-Rs 6 per unit as the capital cost for PSP projects ranges from Rs 50 million-Rs 75 million per MW. These calculations are based on certain assumptions, including a capacity of 1,000 MW, operations for 8 hours daily throughout the year, annual availability of 95 per cent, round trip efficiency of 75 per cent, a project life of 40 years, auxiliary consumption of 1.2 per cent, a debt equity ratio of 75:25, cost of debt of 9 per cent, debt repayment over 18 years, a 15 per cent return on equity, a 25.17 per cent tax, operations and maintenance (O&M) cost of 3.5 per cent of the initial project cost, and O&M cost escalation of 4 per cent annually.

Furthermore, based on the assumption of Rs 65 million per MW as the capital cost over a 40-year period, the cumulative debt service coverage ratio (DSCR) will be 1.84 at a conversion tariff of Rs 6 per unit and an interest rate of 8 per cent. The DSCR falls to 0.8 at a conversion tariff of Rs 3.50 per unit and an interest rate of 10.5 per cent. Similarly, at a conversion tariff of Rs 3.50 per unit and a capital cost of Rs 75 million per MW, the DSCR will be low at 0.72. The DSCR rises to 2.3 with a conversion tariff of Rs 6 per unit and capital cost of Rs 50 million per MW. Therefore, with a gradual increase in conversion tariff and a decrease in capital costs and interest rates, the cumulative DSCR will be better.

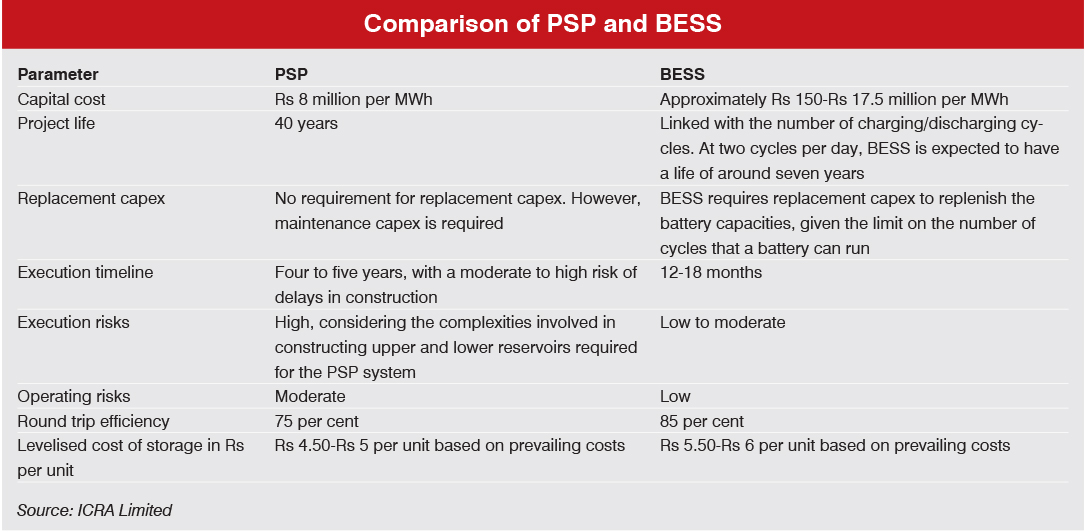

In fact, the levelised cost of storage (LCOS) is low for PSPs (Rs 4.50- Rs 5 per unit) as compared to battery energy storage system (BESS) projects (Rs 5.5 – Rs 6 per unit), making PSPs better from a long-term perspective (explained in the table). Nonetheless, one important thing to note is that PSPs are typically configured for extended discharge periods exceeding six hours, while BESSs are designed for discharge durations of up to four hours. Therefore, comparing LCOS may not accurately indicate which energy storage system is better.

Knowing the cost of storage with RTC renewable energy is key, since these projects are expected to gain traction going forward. Earlier, RTC projects demonstrated relatively better viability with the PSP component compared to BESS projects. However, as per ICRA analysis, based on a few common assumptions across to be the same BESS and PSP projects, the viability for wind-solar hybrid projects with BESS and PSP remains more or less the same. This is mainly due to the recent significant drop in battery prices, which has improved the viability of RTC projects using BESS. The cost for BESS projects fell from Rs 16.7 million per MW per annum in NTPC Limited’s auction for 3,000 MWh BESS held in December 2022 to an all-time low of Rs 4.5 million per MW per annum in Gujarat Urja Vikas Nigam Limited’s recent auction for a 500 MWh BESS in June 2024. This fall in battery prices raises questions about the requirement of viability gap funding approved by the government in September 2023 for the development of BESS projects.

Overall, in order to further enhance the financial viability of PSPs, market reforms such as clear regulations regarding the monetisation of ancillary services and greater use of the energy exchange market should be implemented.

Recent policy developments

Recent policy developments

Recognising the crucial role of PSPs in renewable energy integration, a variety of policy measures have been introduced to encourage its adoption. In June 2023, the CEA launched the guidelines for the formulation of DPRs for hydro PSPs, introducing measures to streamline the concurrence process. According to these guidelines, the preparation timelines for DPRs of PSPs situated in the Himalayan and non-Himalayan regions have been shortened from 900 to 840 and 690 days, respectively, based on geological considerations. Furthermore, the timeline for concurrence of DPRs for certain categories of PSPs has been reduced from 90 days to 50 days. This includes PSPs awarded through tariff-based competitive bidding (TBCB) or as part of integrated or captive plants. The approval timeline for other PSPs has also been reduced from 125 days to 90 days.

In April 2023, the Ministry of Power issued guidelines to promote PSP development, outlining four modes for the allotment of PSP sites to developers. First, states have the option to directly award projects to central or state public sector undertakings based on their experience and financial strength. Second, private developers can participate in a two-stage competitive bidding process to secure PSPs. Third, developers can acquire PSPs through TBCB. Fourth, developers may also self-identify potential off-stream sites where PSPs can be constructed. Furthermore, it includes aspects such as the monetisation of ancillary PSP services (such as spinning reserves, reactive support, black start, peaking supply, tertiary and ramping support, and faster start-up and shutdown of these projects). Other incentives for the segment include no upfront premium for project allocation, reimbursement of the state GST, exemption of fees on land acquisition for off-river PSPs, exemption from the free power obligation, utilisation of exhausted mines for the development of PSPs, and rationalisation of environmental clearances for off-river PSPs. Additionally, energy storage obligations (ESO) have been notified and the prescribed ESO for 2023-24 is 1 per cent, which will increase up to 4 per cent in 2029-30. Moreover, the waiver of inter state transmission system (ISTS) charges was extended to PSPs for projects where construction work was awarded up to June 30, 2025, subject to certain conditions. Subsequently, a partial waiver of ISTS charges, in steps of 25 per cent per year from July 1, 2025 to July 1, 2028, was extended for PSPs where construction work was awarded up to June 30, 2028. Additionally, PSPs have been declared as renewable sources and budgetary support is being provided for funding the enabling infrastructure for hydropower projects and PSPs.

In fact, two states have already developed state-specific policies for PSPs. In May 2023, Madhya Pradesh released guidelines to promote the development of hydro PSPs in the state. These guidelines clarify the methods for allotment of project sites, tax waivers and project completion timelines. The state has a significant potential of 11.2 GW for hydro PSPs, which can be further increased by developing off-river closed-loop PSPs and retrofitting existing hydropower projects. Furthermore, Andhra Pradesh has identified potential PSP sites aggregating 33,240 MW of capacity near the existing reservoirs and off-river locations. Taking into consideration the renewable energy capacity addition targets, hydro purchase obligation targets and the substantial PSP potential, the Andhra Pradesh government notified the Andhra Pradesh Pumped Storage Hydro Power Projects Policy, 2022, in December 2022. State-specific policies are a positive; however, it is key that they align with the central government’s policy.

The way forward

According to the National Electricity Plan 2023, India is projected to require 7.45 GW/47.6 GWh of PSP capacity by 2026-27, 18.98 GW/128.15 GWh by 2029-30 and 26.69 GW/175.18 GWh by 2031-32. The projected funding for PSPs is estimated at Rs 542.03 billion for the period 2022-27 and Rs 752.4 billion for 2027-32. As per CEA report 2023, a PSP potential of 96,529.6 MW was identifed in different parts of the country. This indicates that there is substantial untapped potential and demand for PSPs in India, highlighting a significant opportunity for enhancing the country’s renewable energy infrastructure.

Going forward, given India’s vast potential and technological advancements, PSPs for smaller capacities of 1-10 MW or 200 MW can be developed. These projects will have shorter execution timelines and can significantly support energy storage applications, meeting the intended requirements effectively. Many projects face substantial cost overruns due to factors such as prolonged environmental and forest clearance processes, poor geological conditions and local unrest. Therefore, a comprehensive techno-commercial assessment should be conducted with due diligence to prevent these cost overruns. Additionally, bids can be invited after securing land, obtaining the DPR and receiving environmental clearance. This would lower bidders’ risk perception, leading to more competitive price bids.

As the Indian government focuses on promoting PSPs, it will be interesting to see how the dynamics revolving around technological innovations, on-ground implementation, sourcing finance and regulatory and policy support will help shape the future landscape of PSPs in the country.

Sakshi Bansal and Nidhi Dua