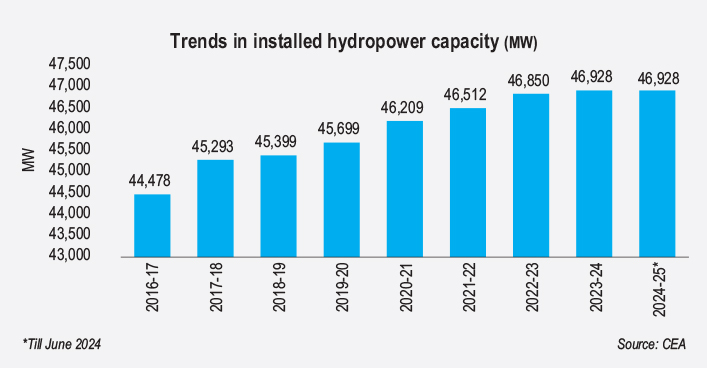

India’s hydropower sector, crucial for providing reliable and flexible power, has an installed capacity of 46,928 MW as of June 2024, accounting for 10.6 per cent of the total capacity. Despite a potential of 145,320 MW, only 32 per cent has been utilised. Recent capacity additions have been limited, with just 1,229 MW added over five years and 78 MW commissioned in 2023-24. The small-hydro power (SHP) potential of 19,749 MW remains underutilised, while pumped storage projects (PSPs) are becoming increasingly important for integrating renewables.

Recent policy changes and developments, including streamlined guidelines and transmission charge waivers, aim to provide an impetus to the sector. Several MoUs have been signed to advance PSP projects. However, challenges such as water rights, environmental concerns and financial issues must be addressed to fully realise the sector’s potential. Strategic expansion and policy support reflect a strong commitment to enhancing hydropower’s role in achieving India’s renewable energy and energy security goals.

Trends in the hydropower segment

The installed large hydropower capacity (above 25 MW) in the country stands at 46,928 MW as of June 2024. The share of hydropower in the country’s total installed capacity is 10.6 per cent. The CEA estimates the hydroelectric potential at 145,320 MW, of which only 32 per cent has been tapped. During the past five years (2019-20 to 2023-24), only 1,229 MW of hydropower capacity has been added. In 2023-24, 78 MW of capacity was commissioned through SJVN Limited’s Naitwar Mori Units 1 and 2 (2×30 MW) and the uprating of BBMB’s Bhakra Left HEP Unit 1 from 108 MW to 126 MW.

According to the CEA data, erratic rainfall caused hydropower generation to drop by 17.76 per cent in 2023-24, and it produced only 134.05 BUs, down from 162.99 BUs the previous year, reducing its share in the total power generation from 11 per cent to 9 per cent. However, in 2024-25 (up to June), hydropower generation slightly increased by 1.03 per cent to 34,878 MUs. Falling reservoir levels are raising concerns about reduced hydropower output this summer, which could increase reliance on coal and other non-renewable energy sources, highlighting the need for better water management and diversified energy strategies.

India’s SHP potential is 19,749 MW, but less than 20 per cent has been utilised due to remote locations and transmission costs. As of June 2024, the installed SHP capacity is 5,005.25 MW. SHP generation in 2023-24 fell 15 per cent to 9,485.04 MUs, but in 2024-25 (up to June), it rose 2.68 per cent to 2,104 MUs, compared to the same period last year.

PSPs will have a vital role to play in future green grids, providing the required storage and balancing services to keep the clean energy supply stable and reliable. India has about 4,745.6 MW of pumped storage capacity in operation as of June 2024, installed in various locations across the country including Telangana (Nagarjuna Sagar PSP and Srisailam LBPH PSP), Maharashtra (Bhira PSP and Ghatgar PSP), Tamil Nadu (Kadamparai PSP), West Bengal (Purulia PSP) and Gujarat (Kadana PSP and Sardar Sarovar PSP). However, only six plants with an installed capacity of 3,305.6 MW are working in pumped mode. The remaining 1,440 MW of capacity across two sites in Gujarat is currently not operating in pumped mode due to delays in the construction of the tail reservoir and vibration-related issues in the system. Further, around 61,060 MW of pumped storage capacity is at various stages of investigation and construction.

Growing focus on PSP

Growing focus on PSP

In August 2024, the CEA approved two hydro PSPs, namely, the 600 MW Upper Indravati in Odisha, being developed by Odisha Hydro Power Corporation Limited, and the 2,000 MW Sharavathy in Karnataka, being developed by Karnataka Power Corporation Limited, in record time. Meanwhile, important MoUs have been signed in the past year to set up PSPs. These include an MoU signed between NHPC and Gujarat Power Corporation Limited for a substantial investment in the proposed 750 MW Kuppa pumped hydro storage project; an MoU between the Uttarakhand government and JSW Energy to establish two PSPs with a combined capacity of 1,500 MW in Almora over the next six years; an MoU between Tata Power and the Maharashtra government for two PSPs with a combined 2,800 MW of capacity; and an MoU between NHPC Limited and Andhra Pradesh Power Generation Corporation Limited for two PSPs.

On the policy front, in March 2023, the CEA issued revised guidelines reducing the timeline for DPR concurrence from 90 days to 50 days for certain PSPs. These include PSPs awarded under Section 63 of the Electricity Act, 2003; those integrated with other renewable sources such as wind and solar; and PSPs developed as captive or merchant plants. Further, in April 2023, the Ministry of Power issued guidelines for PSPs to enhance grid stability and meet peak power demand. The guidelines address monetisation of ancillary PSP services, reimbursement of state GST or exemption of land acquisition fees for off-river PSPs, removal of upfront premiums for project allocation, and safe development of exhausted mines as potential PSP sites. Apart from this, in May 2023, the waiver of ISTS charges was extended to PSPs for which construction has been awarded by June 30, 2025, with a partial waiver, phased out between July 2025 and July 2028, for projects awarded by June 30, 2028.

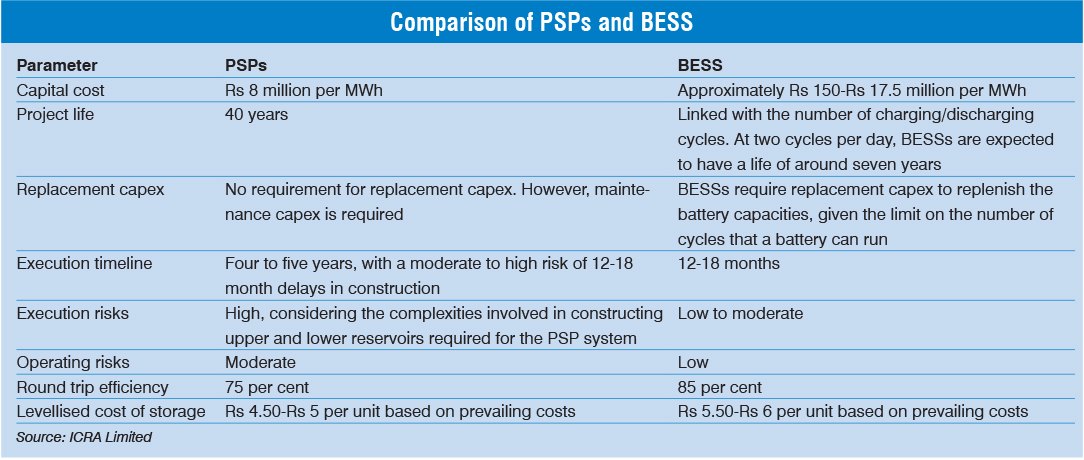

Cost economics of PSPs versus BESS

Cost economics of PSPs versus BESS

For PSPs to be viable, storage costs must be lower than the difference between peak and off-peak electricity rates. ICRA Limited estimates PSP storage costs to be Rs 4-Rs 6 per unit, with capital costs ranging from Rs 50 million to 75 million per MW. The debt service coverage ratio varies based on conversion tariffs and capital costs, ranging from 0.8 to 2.3. PSPs generally have a lower levellised cost of storage of Rs 4.50-Rs 5 per unit compared to battery energy storage systems (BESSs) at Rs 5.50-Rs 6 per unit. However, PSPs are suited for longer discharge periods, while BESSs are better for shorter durations.

Recent drops in battery prices have improved the viability of BESS for round-the-clock renewable projects, reducing the need for government viability gap funding. To boost PSP viability, clearer regulations and greater use of energy exchange markets are necessary.

Challenges and future outlook

According to CEA data, 32 projects with a total capacity of 16,737.5 MW are currently under construction, comprising 12,056 MW from the central sector, 3,091.5 MW from the state sector and 1,590 MW from the private sector. The National Electricity Plan 2023 predicts that large hydro will contribute about 17 per cent to India’s renewable energy capacity by 2026-27. Upcoming capacity includes 10,814 MW of conventional hydro and 2,700 MW of PSPs by 2027, with further additions of 9,982 MW of hydro and 19,240 MW of PSPs by 2032. India is expected to need 7 GW of PSP capacity by 2027, 27 GW by 2032 and 90 GW by 2047, with projected funding of Rs 542 billion for 2022-27 and Rs 752 billion for 2027-32. The country has identified 119 GW of PSP potential, with eight projects (4.7 GW) operational, four (2.8 GW) under construction and 33 (42 GW) under survey for DPR preparation.

To expedite capacity addition in India’s hydropower sector, several challenges must be addressed, including water rights, environmental concerns, financially weak contractors, resettlement issues and unexpected geological conditions, all of which often lead to delays and cost overruns. While the sector has shown growth, significant untapped potential remains. The government’s policy initiatives and ongoing projects reflect a commitment to expanding hydropower, but overcoming these challenges is crucial for sustainable growth. With strategic planning, The hydropower sector can significantly contribute to the country’s renewable energy goals and energy security.

Akanksha Chandrakar