India ratified the Paris Agreement on Climate Change in 2016, committing to limit the global average temperature rise to below 2 °C by the end of the century. As part of its first Nationally Determined Contributions, India pledged to reduce the greenhouse gas (GHG) emissions intensity of its economy by 33-35 per cent by 2030 from 2005 levels, which was later increased to 45 per cent in August 2022.

With ambitious climate goals under the Paris Agreement amid the push for decarbonisation, India is creating a foundation for a carbon trading system, aiming to reduce emissions through pricing and mitigation.

As per the World Bank’s annual “State and Trends of Carbon Pricing 2024”, carbon pricing revenues reached a record $104 billion in 2023. These revenues were generated from over 75 carbon pricing instruments globally and have been invested in climate and nature-related programmes. Carbon markets put a price on emissions, thereby incentivising the reduction of emissions. Carbon trading facilitates the reduction of emissions through trading, where players can sell their “credits” as a profit.

The US government launched an early cap-and-trade system in the 1990s, driving the evolution of carbon markets. This set a precedent for global carbon trading discussions. Finally, it was after the 1997 Kyoto Protocol that the first international carbon market was formed with the mission to reduce GHGs. Later, the European Union (EU) launched the Emissions Trading System in 2005, giving space to emissions trading schemes in the EU.

Carbon trading instruments are primarily of two kinds – compliance mechanisms and voluntary mechanisms. The government manages compliance mechanisms, which include emissions trading systems. This is done by setting a cap on emissions and allowing entities to trade allowances to meet their targets. On the other hand, voluntary mechanisms are managed independently to offset emissions by purchasing carbon credits. In some countries such as China, South Korea, Australia and Japan, there are government-operated voluntary mechanisms.

India’s experience so far

Indian industries have experience with both compliance markets (perform, achieve and trade energy saving certificates [PAT-ESCerts] and renewable energy certificates), and voluntary (offset) projects such as the clean development mechanism (CDM) and other instruments. Indian agencies have registered the second largest number of CDM projects globally.

Voluntary initiatives later evolved into the PAT scheme in 2012, launched by the Bureau of Energy Efficiency (BEE). The PAT scheme was launched under the National Mission for Enhanced Energy Efficiency as part of the eight core missions outlined in India’s National Action Plan on Climate Change. The PAT scheme operates in such a way that when a consumer exceeds the specified consumption targets, the central government issues ESCerts for the surplus energy savings achieved. Conversely, designated consumers who fall short of their specific energy consumption targets are required to purchase ESCerts equivalent to their shortfall. This trading mechanism ensures compliance while promoting energy efficiency. The PAT scheme was India’s first market-based mechanism to improve energy efficiency in energy-intensive industries. The scheme also mandated consumers of energy intensive sectors such as thermal power, cement, steel and aluminium to stick within specific energy consumption reduction targets. Under the PAT scheme alone, Indian industrial units have collectively achieved CO2 emissions savings of over 106 million tonnes between 2015 and June 2024. Currently, the compliance mechanism covers the aluminium, cement, iron and steel, petrochemicals, petroleum refinery, pulp and paper, and textile sectors.

In both cases (voluntary and compliance), the entities are rewarded for their additional savings, through credits or certificates. Hence, there is sufficient capacity available in the country to support a full-fledged domestic carbon market framework. A market-based mechanism approach is not new to entities in India.

CCTS

CCTS

In view of the above justification and the need for the country to meet its ambitious climate goals, a robust national framework for the Indian carbon market is being developed through a reliable national carbon credit electronic platform. This framework aims to complement and support various entities undertaking projects to decarbonise the Indian economy by pricing their additional actions towards GHG emissions reduction.

The Ministry of Power (MoP) released a draft on the Carbon Credit Trading Scheme (CCTS) on March 27, 2023, with the aim of establishing a framework for the Indian carbon market. The country’s carbon market is based on the amendments to the Energy Conservation Act, 2001, adopted by the Indian legislature in December 2022.

The CCTS was officially notified in June 2023 and amended in December 2023 under the Energy Conservation Act, 2001. In July 2024, the Indian government adopted detailed regulations for the planned compliance carbon market under the CCTS.

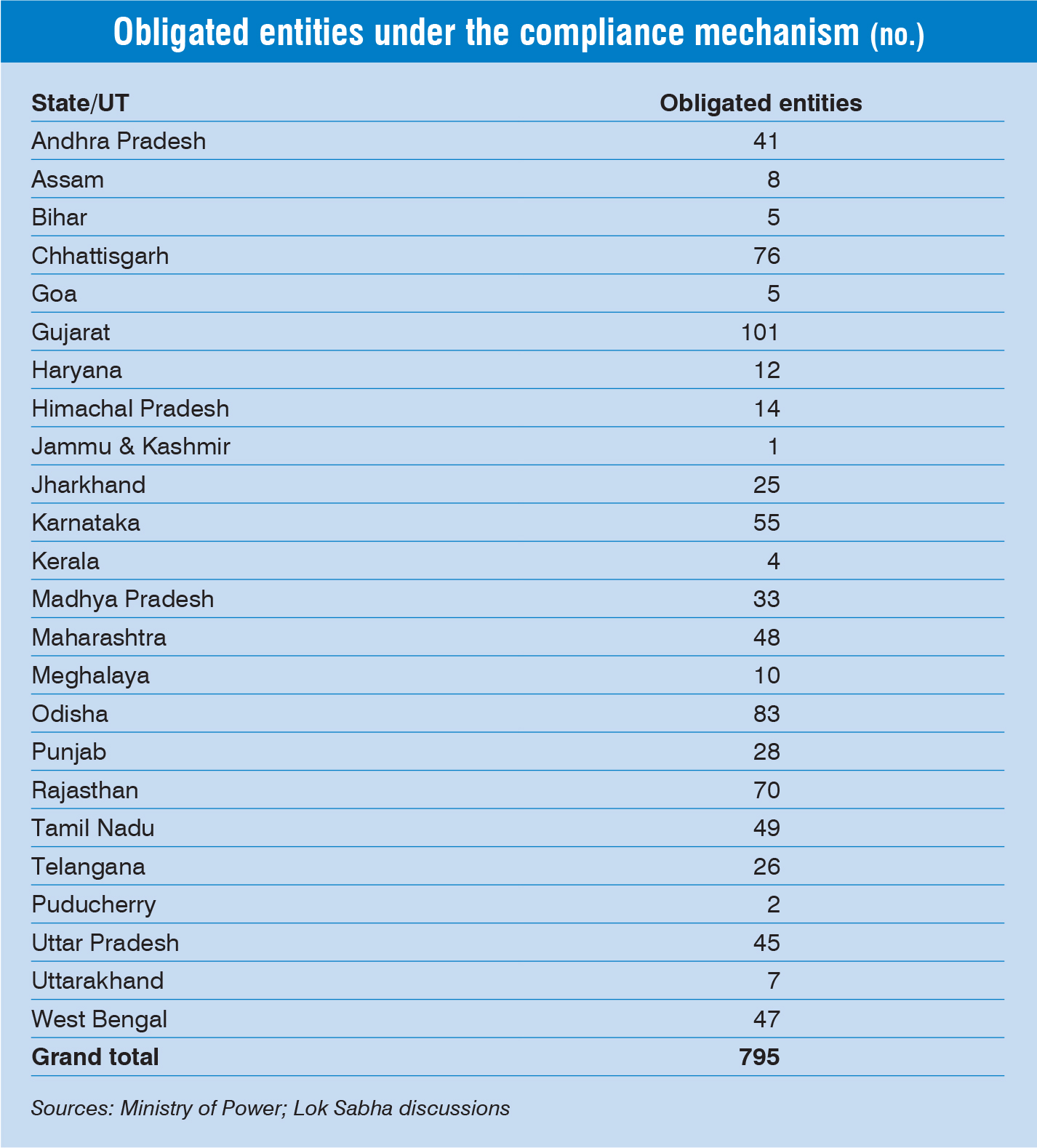

The compliance mechanism includes a mandatory programme for energy-intensive industries, in which the government sets GHG emissions intensity targets (GHG emissions per unit of output) that these entities must comply with. Under the compliance mechanism, the central government specifies the registered entities as obligated entities. For this purpose, BEE will identify sectors with potential for GHG emissions reduction and recommend their inclusion in the Indian carbon market. It will then recommend the targets in terms of tonnes of carbon dioxide equivalent per unit of equivalent product, considering all relevant aspects such as available technologies and the likely cost of their implementation. Across states, over 795 obligated entities are estimated to be included under the compliance mechanism of CCTS. Nine sectors – aluminium, chlor-alkali, cement, fertiliser, iron and steel, pulp and paper, petrochemicals, petroleum refinery, and textile – are considered for gradual transition under the compliance mechanism, and more sectors will be included in the future.

For the offset mechanism, India has identified 10 sectors for its carbon market offset mechanism, including energy, industries, agriculture, waste handling and transport. Under the offset mechanism, non-obligated entities can register their projects for GHG emissions reduction, removal, or avoidance to receive carbon credit certificates (CCCs) upon fulfilling the eligibility requirements, as per the detailed procedure published by BEE based on recommendations of the National Steering Committee for Indian Carbon Market.

The Central Electricity Regulatory Commission (CERC) notified the draft CERC (Terms and Conditions for Purchase and Sale of Carbon Credit Certificates) Regulations, 2024, with the aim of creating a framework for the exchange of CCCs for both obligated and non-obligated entities on power exchanges. As per the draft, the Grid Controller of India will act as the registry for CCC exchanges. BEE will manage the CCCs under the Energy Conservation Act, 2001, working with the CERC on overseeing transactions, ensuring compliance and sharing relevant information with stakeholders.

Outlook and learnings

According to recent reports, the domestic carbon market launch is expected by mid-2026, featuring both voluntary and compliance-based mechanisms.

The experience of the EU Emissions Trading System offers valuable outlook and learnings for the development of Indian carbon markets. An important lesson is how to effectively achieve emissions reduction through the cap-and-trade system and avoid the problem of double counting. This is possible when the policy is supported by a progressive tightening of allowances. Further, India can also explore hybrid approaches, as followed by China, where emissions caps are extended to large electricity consumers based on indirect usage. This strikes a balance between environmental goals and consumer cost protection. Key stakeholders, such as industry representatives, think tanks and policymakers, must collaborate to shape the system’s design and implementation. In conclusion, India must develop a robust carbon market in line with BEE’s outlined plan while implementing safeguards against double counting to drive meaningful emissions reduction.