Hydropower continues to play a critical role in India’s energy transition, offering a reliable and renewable source of electricity, with grid-balancing capabilities. As of June 2025, India’s total installed hydropower capacity stood at 54,480.21 MW. While capacity additions have been modest in recent years, the segment has shown steady growth, with increasing policy support and a renewed emphasis on pumped storage projects (PSPs). These developments signal a shift towards hydropower not just for baseload generation but also for flexible, round-the-clock renewable energy integration. With multiple projects under construction and a substantial capacity in the pipeline, the hydropower sector is poised for significant expansion in the coming years.

Segment size and growth

As of June 2025, the country’s installed hydropower capacity stood at 49,378.16 MW for large hydro and 5,102.05 MW for small hydro. The northern region has the highest installed hydropower capacity, totalling 21,794.73 MW.

During 2024-25, 799.99 MW of hydropower capacity (large hydro) was added, as against the 60 MW added in 2023-24. Key projects commissioned in 2024–25 were NHPC’s Parbati-II HPS Units 1, 2 and 3 (each 200 MW); Beas Valley Power Corporation Limited’s Uhl-III HPS Units 1, 2 and 3 (each 33.33 MW); KSEB’s Pallivasal Extension HPS Units 1 and 2 (each 30 MW); and KSEB’s Thottiyar HEP Unit 1 (10 MW) and Unit 2 (30 MW).

During 2025-26, a total of 1,650 MW of large hydro power capacity has been added as of June 2025. This includes NHPC’s Parbati-II HPS Unit 4 (200 MW), THDC’s Tehri PSP Unit 1 (250 MW), and Greenko’s Pinnapuram HPS Units 1 to 5 (5×240 MW).

Large hydro generation during April-June 2025 reached 39,658.25 MUs, reflecting a 13.41 per cent increase, compared to the same period in the previous year. During April-May 2025, small-hydro generation rose by 10.57 per cent to 1,468.39 MUs.

During 2024-25, the share of hydropower (large and small) in the total renewable energy generation was 40 per cent, while the hydropower share in the total power generation in 2024-25 was 8.76 per cent.

PSP segment

Given their long-duration storage capabilities, PSPs are expected to play a pivotal role in sustainably integrating intermittent renewable sources, while maintaining grid stability. This technology will be particularly important in meeting the rising demand for round-the-clock renewable energy by utilities and industrial consumers.

As of June 2025, 10 PSPs, with a combined capacity of 6,195.6 MW, are operational, eight (8,500 MW) are under construction, five (5,780 MW) have been accorded concurrence by the Central Electricity Authority (CEA) and two (2,240 MW) are under examination. India has nine on-river PSPs with a combined capacity of 4,995.6 MW, spread across Telangana, Maharashtra, Gujarat, Tamil Nadu, Uttarakhand and West Bengal, and one 1,200 MW off-river PSP in Andhra Pradesh. However, only eight plants with a total capacity of 4,755.6 MW operate in pumped mode, while 1,440 MW of capacity across two sites in Gujarat remain non-operational in pumped mode. Additionally, 4,600 MW of on-river and 3,900 MW of off-river PSPs are under construction, while another 2,500 MW of on-river and 3,280 MW of off-river PSPs have been approved by the CEA. Survey and investigation activities are under way for 46 PSPs with a total capacity of 64,790 MW.

Recent policy initiatives

There has been a policy push to promote the construction of PSPs at the national and state levels to meet energy storage requirements.

In June 2025, the Ministry of Power (MoP) issued a clarification on the waiver of interstate transmission system (ISTS) charges for hydro PSPs. As per the latest provisions, 100 per cent ISTS charges waiver will apply to hydro PSPs awarded on or before June 30, 2028. However, hydro PSPs awarded after June 30, 2028, will not be eligible for the waiver.

In May 2025, the Ministry of New and Renewable Energy issued revised guidelines for small-hydro power schemes. The revised guidelines apply to all small-hydro projects sanctioned under the previous schemes and aim to address ongoing sectoral challenges faced by stakeholders. For release of the balance central financial assistance (CFA), projects now need to achieve at least 80 per cent of the projected generation for any one corresponding month as per the detailed project report (DPR). If not, the second instalment of CFA will be proportionally reduced. If a project achieves 73 per cent of the projected generation for the cumulative of three consecutive months or cumulative annual generation for one year as envisaged in the DPR, the second instalment of CFA will be calculated on a pro-rata basis, with the methodology being provided in the policy document.

In February 2025, the MoP released new tariff-based competitive bidding guidelines for procuring storage capacity and stored energy from PSPs. Applicable to both developers and procurers (end and intermediary), guidelines cover new, under-construction and existing PSPs. Procurement follows a single-stage, two-part bidding process and can be done through two modes – Mode 1 for sites identified by the procurer (with government-owned sites developed on a build-own-operate-transfer basis), and Mode 2 for sites proposed by the developer or from ongoing projects, developed on a build-own-operate basis. Developers are responsible for statutory clearances and power purchase agreements must be signed within six months of the letter of award. The framework also outlines responsibilities for transmission, tariff adoption and post-PPA project operation, ensuring transparency and accountability throughout the procurement process.

Another key measure to support the segment was the budgetary support scheme aimed at creating “enabling infrastructure for HEPs” with a total outlay of Rs 124.61 billion. The scheme will be implemented from 2024-25 to 2031-32. It is applicable to PSPs and hydroelectric projects (HEPs) above 25 MW, with a cumulative generation capacity of about 31,350 MW and a letter of award received before June 30, 2028. The scheme will be implemented from 2024-25 to 2031-32. PSPs with an aggregate 15,000 MW of capacity will be supported under the scheme.

Cross-border projects

Apart from domestic projects, Indian hydro players are actively investing in cross-border projects. NHPC Limited is involved in three major HEPs – West Seti (750 MW), Seti River-6 (SR6) (450 MW) and Phukot Karnali (480 MW). NHPC is also in advanced discussions with the Government of Bhutan for the potential development of a hydropower project on the Puna Tsang Chu river.

NHPC Limited is involved in three major HEPs – West Seti (750 MW), Seti River-6 (SR6) (450 MW) and Phukot Karnali (480 MW). NHPC is also in advanced discussions with the Government of Bhutan for the potential development of a hydropower project on the Puna Tsang Chu river.

SJVN Limited has been actively expanding its hydropower portfolio in Nepal. The company is currently engaged in three major projects – the 900 MW Arun-3 HEP, which is under construction; the 669 MW Lower Arun HEP, which is in the pre-construction phase; and the 490 MW Arun-4 HEP, which is under survey and investigation.

Meanwhile, in June 2024, the Adani Group expanded its footprint in Bhutan by signing an MoU with Druk Green Power Corporation to develop a 570 MW hydropower project in Chukha province. Additionally, Adani is exploring the development of a 700 MW project at Chamkarchhu, where all necessary approvals are already in place, allowing for immediate commencement of work.

Tata Power has also entered the Bhutanese hydropower sector through a partnership with Druk Green Power Corporation Limited. This collaboration aims to develop 5,000 MW of clean energy capacity, including 4,500 MW from hydropower sources. The projects to be developed in phases include the 1,125 MW Dorjilung HEP, the 740 MW Gongri reservoir project, the 1,800 MW Jeri PSP and the 364 MW Chamkharchhu IV Project.

The way forward

As the efforts towards energy transition intensify, hydropower is emerging as a prominent source of energy that can improve system flexibility. Backed by policy support and ongoing project development, the segment is poised for significant growth.

India’s current installed hydro capacity of 54 GW accounts for an 11 per cent share in the energy mix. PSPs are expected to lead the growth of the hydropower segment, going forward. This mature and proven technology with long-duration storage capabilities has garnered positive interest from private and public sector players. Characterised by a low gestation period and fewer risks, off-river PSPs are getting greater attention.

Going forward, as per the CEA’s National Electricity Plan 2023, the installed hydro capacity is projected to reach 88 GW by 2031-32, including 26 GW from PSPs. This expansion is estimated to require a total investment of approximately Rs 3.2 trillion.

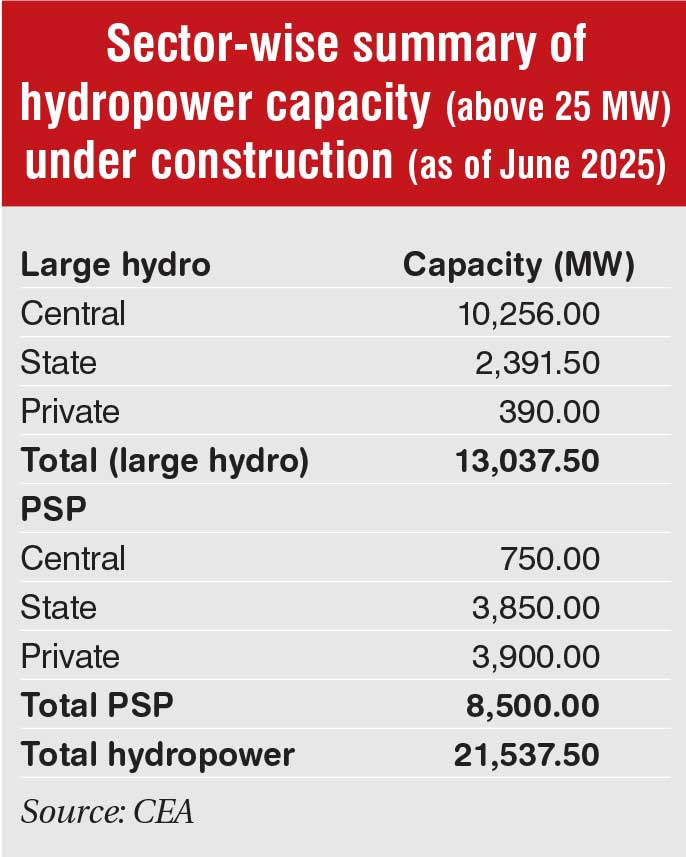

As of June 2025, large hydro power projects (including PSPs) with a total capacity of 21,537 MW are under construction. Of this, 11,006 MW is in the central sector, 6,241.5 MW in the state sector and 4,290 MW in the private sector. Of the total capacity, around 1,820 MW of hydropower capacity is anticipated to be commissioned in 2025-26.

To expedite this growth, it is crucial to overcome the legacy challenges facing the segment such as prolonged construction timelines, delays in environmental clearances and difficulties in land acquisition. Besides, measures such as a remuneration mechanism specifically for hydropower (especially PSPs), affordable financing options for hydropower development and modernisation of ageing hydropower projects are needed in the segment.