Thermal power generation holds a central place in India’s energy landscape, accounting for 49.74 per cent (243,789.62 MW) of the country’s total installed capacity as of July 2025. Industrial operations, infrastructure development and rural electrification continue to rely on the baseload electricity that thermal power provides. Its continuous and scalable supply is critical to supporting India’s accelerated economic and population growth.

However, the role of coal-based capacity is expected to evolve significantly over the next decade, driven by the increasing penetration of renewables and storage solutions. Going forward, the segment is expected to see greater focus on cleaner technologies and decarbonisation.

A look at the key trends and developments shaping the thermal power generation segment…

Segment growth and performance

India’s installed thermal generation capacity stood at 242.03 GW as of June 2025, accounting for a 50 per cent share in the overall energy mix. Of this, coal dominated at 214.69 GW (44.28 per cent) while lignite-based capacity stood at 6.62 GW (1.36 per cent), gas at 20.13 GW (4.15 per cent) and diesel at 589 MW (0.12 per cent).

The thermal power segment has witnessed a mixed trend in terms of capacity addition. In 2024-25, thermal capacity addition stood at 3.8 GW, against the target of 15.3 GW. In 2023-24, it increased to 6.1 GW, though still short of the 14.7 GW target. In 2025-26, up to June, 1.5 GW of new capacity was added against the target of 12.8 GW.

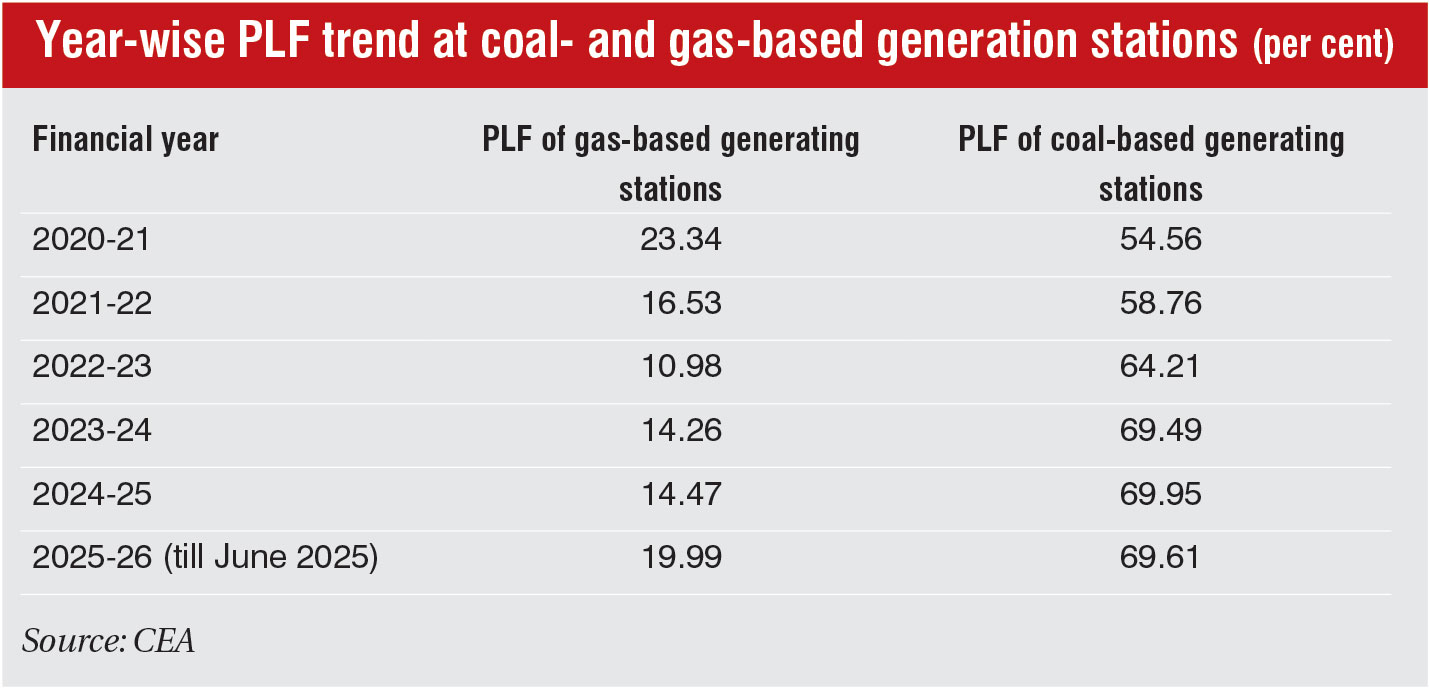

On a year-on-year basis, the plant load factor (PLF) of thermal generating stations has declined. During 2024-25, the average thermal PLF was 67.15 per cent compared to 67.90 per cent in 2023-24. During June 2025, the PLF stood at 66.62 per cent, down from 74.82 per cent in June 2024. The decline can be attributed to reduced utilisation of state-owned thermal power plants (TPPs), along with early-onset and above-average rainfall, which reduced electricity demand from cooling and agricultural activities.

Notably, the PLF of gas-based power plants stood at 14.47 per cent in 2024-25, higher than the 14.26 per cent reported in 2023-24. Meanwhile, coal-based power plants operated at 69.95 per cent PLF in 2024-25, compared to 69.49 per cent in 2023-24.

Thermal generation trends

Thermal energy generation has recorded an upward trend in recent years. In 2023-24, thermal generation stood at 1,326 BUs, contributing 70 per cent to the energy mix, up from 1,206 BUs (67 per cent) in 2022-23. In 2024-25, it reached around 1,364 BUs, accounting for 74 per cent of total energy generation. Between 2018-19 and 2024-25, thermal generation grew at a compound annual growth rate of 4 per cent. This momentum is expected to continue as thermal power remains crucial for meeting the country’s growing electricity demand despite its long-term goals of diversifying the energy mix and reducing dependence on fossil fuels.

Recent policy developments

Recent policy developments

In May 2025, the Cabinet Committee on Economic Affairs approved the revised SHAKTI policy for granting fresh coal linkages to TPPs in the central/state/independent power producer (IPP) sectors. The revised policy highlights two key elements – Window I: coal linkage for central/state power generating stations at the notified price; and Window II: coal linkage for all power generating stations at a premium above the notified price. The amended policy aims to streamline the coal linking process, enable IPPs and private entities to expand thermal power capacity, and remove the requirement for power purchase agreements (PPAs) for electricity generated from coal acquired under Window II.

In April 2025, the Ministry of Power (MoP) proposed draft amendments to the model bidding documents for long-term power procurement from thermal power stations set up on a design, build, finance, operate and own basis, and invited public comments.

Meanwhile, to meet the surge in demand in summer months, the MoP, under Section 11 of the Electricity Act, 2003, directed the entire gas-based power fleet in the country to be operational from May 26, 2025 to June 30, 2025, in order to ascertain round-the-clock power supply in a peak demand and high temperature scenario. A similar notification required imported coal-based power plants to run at full capacity until June 30, 2025.

Emission control

A critical policy development in the thermal segment has been the relaxation of flue gas desulphurisation (FGD) norms for TPPs. In July 2025, the Ministry of Environment, Forests and Climate Change (MoEFCC) exempted 78 per cent of India’s TPPs from installing FGD systems. Only TPPs falling under Category A-located in densely populated areas or situated within 10 km in the NCR region – are required to install FGD.

Previously, in 2015, the MoEFCC had rolled out stringent environmental standards for SO2, NOX and mercury emissions alongside a mandate to curtail water consumption. Coal-based TPPs were required to comply with the norms by 2017, which involved installing FGD systems to reduce SOX emissions, implementing burner enhancements to reduce NOX emissions and adopting PM control technologies. However, compliance was delayed due to various techno-economic and logistical constraints. Since 2017, the government has granted three extensions, the latest in December 2024, revising the compliance timeline to 2027-2030.

Category A covers coal-based plants within a 10 km radius of the NCR or cities with a population of over 1 million. These plants are required to comply by 2027. Category B plants, are eligible for exemption on a “case-by-case” basis, following a joint review by the Central Electricity Authority or the Central Pollution Control Board. There are 72 plants in this category, of which only four have installed FGD units. These plants have a deadline of 2028. The remaining 462 plants come under Category C, of which 32 have installed FGD units. These plants have a 2029 deadline.

Recent project announcements

Several new thermal projects have been announced in the past few months, with states inviting tenders to set up new coal-based power plants. In August 2025, the Tamil Nadu Power Generation Corporation submitted a proposal for the development of the Ennore Thermal Power Station (ETPS) expansion project via a tariff-based competitive bidding process under the public-private partnership model. Under the revised SHAKTI policy, the ETPS expansion project has been recommended for fresh coal linkage.

Meanwhile, the Assam government has announced plans to establish a 3,400 MW TPP in the Bilashipara area of Dhubri district. Under the Assam Thermal Power Generation Promotion Policy, 2025, the state aims to develop 2,000 MW of thermal generation capacity by 2030 and 5,000 MW by 2035, with private sector participation.

The segment has also witnessed the signing of fresh thermal PPAs after a long hiatus. In May 2025, Adani Power Limited signed a power supply agreement with Uttar Pradesh Power Corporation Limited to dispatch power from its forthcoming ultra-supercritical coal-fired power plant in Mirzapur, Uttar Pradesh. The project will help meet the state’s electricity demand surge of about 11,000 MW by 2033-34.

Further, in August 2025, Adani Power Limited (APL) announced the setting up of a new 2,400 MW greenfield ultra-supercritical TPP in Bhagalpur, Bihar. As per the letter of intent obtained from Bihar State Power Generation Company Limited, APL is likely to supply power to two distribution companies in Bihar, namely North Bihar Power Distribution Company Limited and South Bihar Power Distribution Company Limited, at a price of Rs 6.075 per kWh.

In April 2025, JSW Energy announced an investment of around Rs 160 billion for the development of a 1,600 MW ultra-supercritical TPP at Salboni, West Bengal. The company has signed a 25-year PPA with West Bengal State Electricity Distribution Company Limited for supply from the project.

Sector major NTPC also has a significant project pipeline. The company has earmarked a total capital expenditure of Rs 559.2 billion for 2025-26 to add 11.8 GW of generation capacity, including 3.5 GW of thermal power.

Flexibilisation

A key emerging trend in the thermal power segment is the flexibilisation of TPPs. As renewable energy penetration increases, maintaining grid stability becomes more challenging due to the intermittency of renewable energy sources. Hence, flexibilisation of TPPs is critical to ensure frequent and rapid ramping of power capacity. To prepare plants for flexibilisation, modification in components and chemical regimes, and operational practices are being undertaken.

Flexibilising coal-fired power plants allows them to quickly adjust output to meet variable grid demand to complement intermittent renewable energy. However, this has created operational challenges for TPPs as they must adjust their generation schedules and ramp rates to accommodate renewable energy output fluctuations while ensuring grid stability and reliability.

Operational techniques for flexibilisation aim to improve plant safety, efficiency and flexibility under varying load conditions. As per the report “Flexibilisation of Coal-Fired Power Plants”, a phased method has been proposed to retrofit and upgrade thermal units to enable operation at a technical minimum load of 40 per cent, compared to traditionally higher levels.

Further, a specialised training programme is required for plant operators to safely manage flexible operations, as flexible operations demand a higher level of vigilance. The key interventions include two-shift operations or frequent cycling, advance operational planning to balance demand and reduce wear, and maintaining consistent coal quality to minimise operational disruptions.

Meanwhile, technical retrofits and equipment upgrades such as boiler combustion systems, heat rate improvements and condition monitoring are being explored to increase flexibility.

Control and digital technologies are also critical interventions. For example, the use of digital tools improves unit availability, ramp rates, and start-up and shutdown times. Meanwhile, bypass systems and control valves enable rapid load changes in line with grid requirements. Further, technologies such as condensate limiting provide immediate generation response for grid frequency stabilisation.

As India accelerates renewable energy integration, flexibilisation of coal-based assets will be critical for enabling efficient partial load operation and minimising untimely retirements.

Future outlook

As per the National Electricity Plan (Generation), 2023, India’s installed generation capacity is projected to reach 874 GW by 2031-32. Meanwhile, the country’s thermal capacity requirement is estimated to reach 307 GW by 2034-35. The MoP plans to establish an additional 97,000 MW of new coal and lignite-based thermal capacity. As per a recent MoP update to Parliament, around 11.68 GW of thermal capacity was commissioned between April 2023 and June 2025. Further, 38.93 GW of thermal capacity, including 5.69 GW of distressed TPPs, is currently under construction. In 2024-25, new contracts for 15.44 GW of thermal capacity were awarded and are awaiting construction. Another 35.46 GW of coal and lignite-based prospective capacity has been identified, which is currently at various stages of planning.

Given the expected rise in energy demand, the Central Electricity Authority issued an advisory in 2023 to all thermal power utilities, directing them not to retire or repurpose their coal-based power stations before 2030 and to ensure the availability of thermal units through renovation and modernisation activities.

India is pursuing a phased transition path that involves rapidly adding renewable energy while ensuring that coal capacity, which is the backbone of its electricity generation portfolio, continues to play a critical role.