India aspires to become a $30 trillion economy by 2047, but achieving this vision will require major structural shifts in the energy sector to meet rising demand and climate targets. As part of its global climate commitments, India has pledged to achieve net-zero emissions by 2070. It is estimated that by 2047, over 80 per cent of installed electricity generation capacity and nearly two-thirds of electricity generation will need to come from non-fossil fuel sources.

A recent report the Central Electricity Authority (CEA), titled “Target of 100 GW Nuclear Capacity by 2047: The Road Map”, by outlines India’s nuclear ambitions and the multi-pronged strategy required to expand current capacity from the current 8.88 GW to 100 GW by 2047. Given that it has the lowest life-cycle CO2 emissions among major sources, nuclear energy remains one of the cleanest generation technologies available.

As a result, the central government has allocated Rs 200 billion for the development of at least five indigenously designed small modular reactors (SMRs) by 2033. The proposed Nuclear Energy Mission will be supported by legislative reforms, including amendments to the Atomic Energy Act and the Civil Liability for Nuclear Damage Act to facilitate private sector participation and streamline project development.

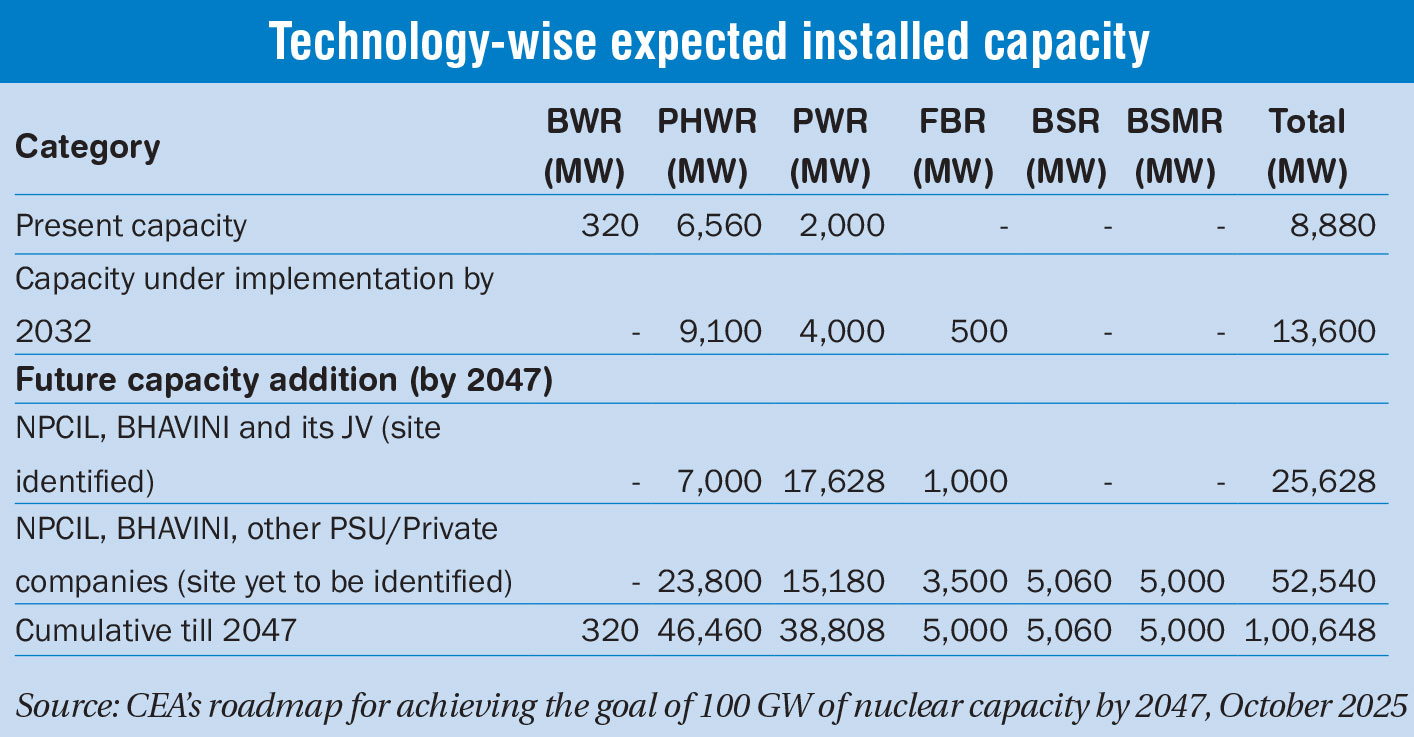

Present capacity

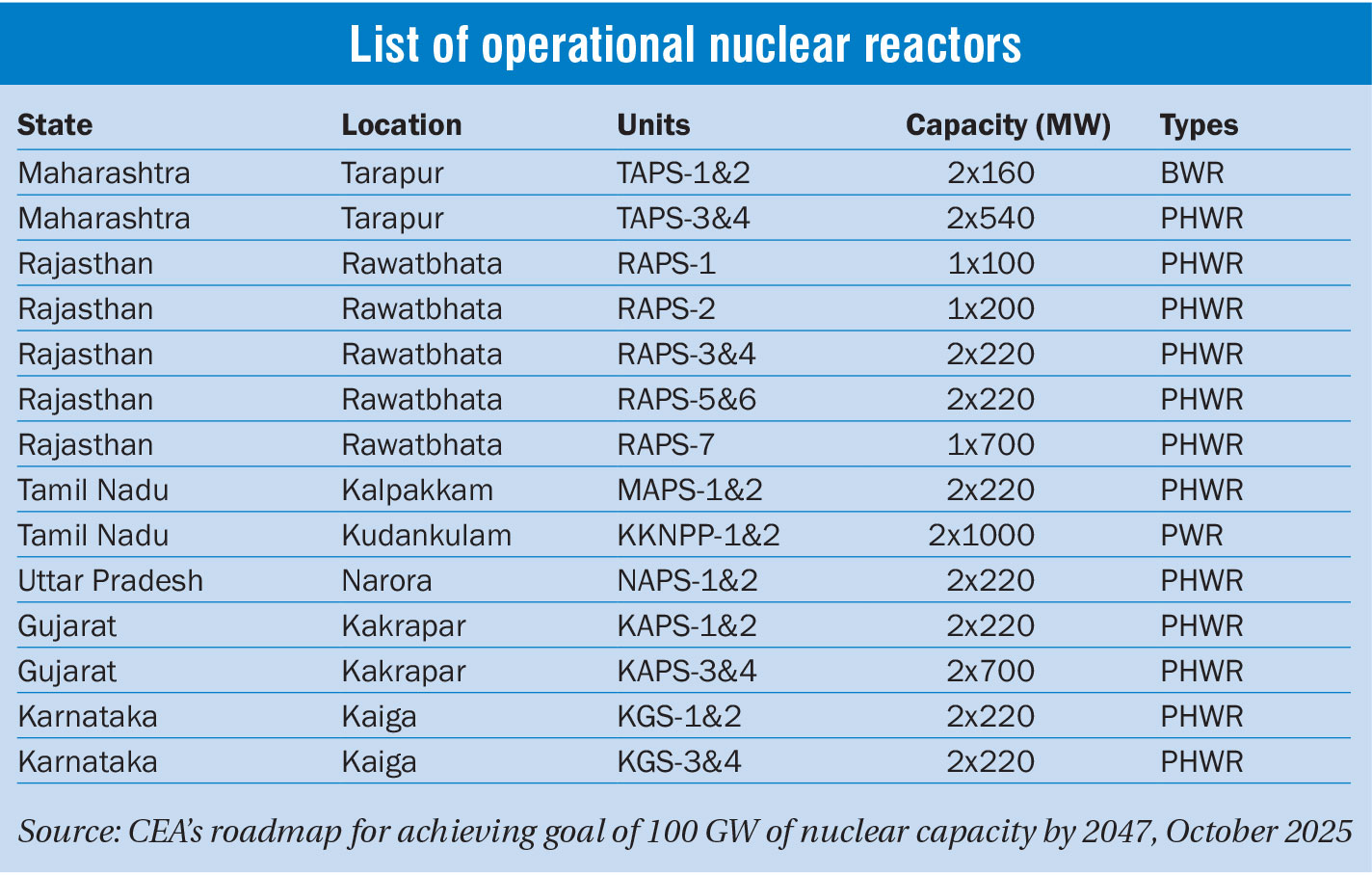

As of October 2025, India has 25 nuclear reactors operational across seven nuclear power plants, with a total installed capacity of 8,880 MW. In addition to the operating fleet, eight nuclear reactors aggregating 6,600 MW are under construction. This includes the 500 MW prototype fast breeder reactor being developed by Bharatiya Nabhikiya Vidyut Nigam Limited (BHAVINI). A further ten reactors, with a combined capacity of 7,000 MW, are in the advanced stages of pre-project activities.

How nuclear power can meet industrial growth

According to NITI Aayog’s India Energy Security Scenarios, industrial output must increase significantly to achieve the “Viksit Bharat 2047” vision. By 2047, crude steel production is expected to rise from 144 million tonnes in 2023-24 to 530 million tonnes. Cement output is projected to more than double from 426 million tonnes to 910 million tonnes, while aluminium production is expected to grow more than fivefold, from 5.5 million tonnes to 30 million tonnes.

Nuclear power plants are well-suited to meet this need. As base load stations, they operate at steady-rated capacities with minimal interruptions. Pressurised water reactors (PWRs) typically run at full load for 12-18 months before refuelling, while Indian PHWRs equipped with online refuelling capabilities have demonstrated continuous operation for over two years in several instances. With low variable operating costs and high plant load factors, nuclear plants offer dependable supply for 24×7 industrial operations. Further, nuclear energy is virtually zero-emission during operation and plays a key role in India’s decarbonisation strategy. It is particularly relevant for hard-to-abate sectors such as cement, steel, chemicals, aviation and shipping, which face technological and financial barriers to electrification. Given these attributes, the expansion of nuclear capacity is vital not only for ensuring round-the-clock power, but also for advancing India’s net-zero ambitions by 2070.

The roadmap for nuclear capacity expansion

The roadmap for nuclear capacity expansion

To achieve the target of 100 GW of nuclear installed capacity by 2047, the committee constituted to examine the issue has outlined a multi-pronged roadmap. This includes four key elements: a realistic trajectory of future capacity additions, a breakdown of the critical inputs required, identification of the challenges likely to arise and actionable recommendations to address these hurdles.

The committee has observed that PHWR technology will remain the primary driver of capacity expansion over the next decade. Large-scale commissioning of reactors based on PWR technology is expected to take place only after 2035. Further, the adoption of foreign technologies, when they achieve commercial maturity, must be actively pursued. To contain project costs, the committee recommends a phased domestic manufacturing strategy, similar to the approach used for ultra supercritical technology in thermal power. Additionally, diversification of reactor technology sources will strengthen energy security by mitigating geopolitical risks.

Key recommendations

To operationalise the roadmap and support the capacity trajectory envisaged, the committee has made the several strategic recommendations. First of all, the national three-stage programme should remain a cornerstone of nuclear development in India. This calls for enhanced financial and technical support in order to achieve long-term energy independence and greater technological depth, particularly in thorium utilisation. Secondly, PHWRs should continue to be the mainstay of nuclear capacity addition in the current decade, given their indigenous design and existing manufacturing ecosystem. Where feasible, large reactors should be installed to optimise site use, given the limited number of suitable locations for nuclear plants. The committee also suggested the adoption of advanced fuels and technologies that can accelerate thorium utilisation. Finally, investments in R&D for next-generation designs such as advanced high-temperature reactors and SMRs, along with flexibility, should also be a criterion in the selection of foreign nuclear technologies.

Key challenges

Key challenges

Achieving 100 GW of nuclear capacity by 2047 will require addressing several regulatory, financial and operational bottlenecks. A key barrier is the limited scope for private sector participation under the Atomic Energy Act, 1962. The act restricts nuclear power generation to government-owned entities. Amendments have been proposed to the Companies Act to enable compliant entities to hold licences, manufacture and manage nuclear materials and participate in tariff-based bidding. Additionally, changes to the AERB constitution have also been suggested to strengthen regulatory oversight across all reactor types and ownership structures. Another major concern is the supplier liability clause under the Civil Liability for Nuclear Damage Act, 2010 which deviates from international norms and exposes suppliers to potentially unlimited liability, discouraging technology transfer and after-sales services. While the Indian nuclear insurance pool provides partial cover, risk perceptions remain high. Project development timelines are another challenge, with reactor construction typically taking five-and-a-half to six years, and overall project gestation extending to 11–12 years due to delays in site approvals and clearances. Additional constraints include the need to scale up heavy water production, establish a dedicated design and site-support agency, and build a robust domestic vendor ecosystem.

On the financing front, the high capital intensity of nuclear projects necessitates both equity and debt innovations. For example, the Kakarapar-3&4 projects, where interest during construction rose from Rs 15.32 billion to Rs 71.51 billion, highlights the need for timely execution. To fix this challenge, we should reduce GST on nuclear island components from 18 per cent to 12 per cent, raise normative plant load factors to 80 per cent and enable tariff-based competitive bidding after initial experience under cost-plus models.

The Way forward

As India charts a path toward 100 GW of nuclear capacity by 2047, we must build supportive institutional, financial and human resource strategies. This can be done by recognising nuclear power within India’s climate finance taxonomy. The classification of nuclear as a clean energy source could unlock access to long-term, low-cost capital, and improve investor confidence. Second, adopting innovative financing mechanisms will be essential to meet the scale of investment required. Third, the sector must prepare a skilled and diverse nuclear workforce. To reach 100 GW, India will require a significant increase in trained personnel across design, engineering, procurement, construction, operations, decommissioning and waste management. Regulatory bodies, utilities such as NPCIL, private sector developers and the vendor ecosystem will all require capacity building. Specialised expertise in areas such as quality assurance, safety regulation and nuclear transport logistics will also be essential.

Overall, the expansion of nuclear energy offers India a scalable, low-carbon and 24×7 reliable pathway to meet its development and decarbonisation goals. Timely policy reform, institutional strengthening and investment mobilisation will be vital to deliver on this ambition by 2047.