Despite having significant potential, hydropower development in India has been rather slow. Against an estimated potential of 148.7 GW, the installed capacity is only 44.48 GW (projects of 25 MW and above capacity) and projects of 10.84 GW capacity are under construction. Further, as per the Ministry of Power (MoP), out of the 44 under-construction hydropower projects in the country, about 20 projects aggregating 6,329 MW are presently stalled/stressed. An investment of Rs 310.5 billion has already been incurred on these projects.

With the increasing share of renewables, the changing power scenario in India calls for more hydro capacity. Hydropower generation is one of the most preferred options to manage the intermittent nature of renewables, in view of its quick start-up time. The government is undertaking a number of measures to promote growth in the segment such as the reassessment of hydro potential considering additional site constraints. It is also working on a new hydro policy. The MoP is evaluating options to provide cheap credit to hydropower projects in order to reduce tariffs. It is in discussions with the Central Electricity Regulatory Commission to evaluate the modalities to reduce tariffs by rationalising certain parameters like depreciation and other costs. Power Line takes a look at the key developments in the hydro segment…

Size and growth

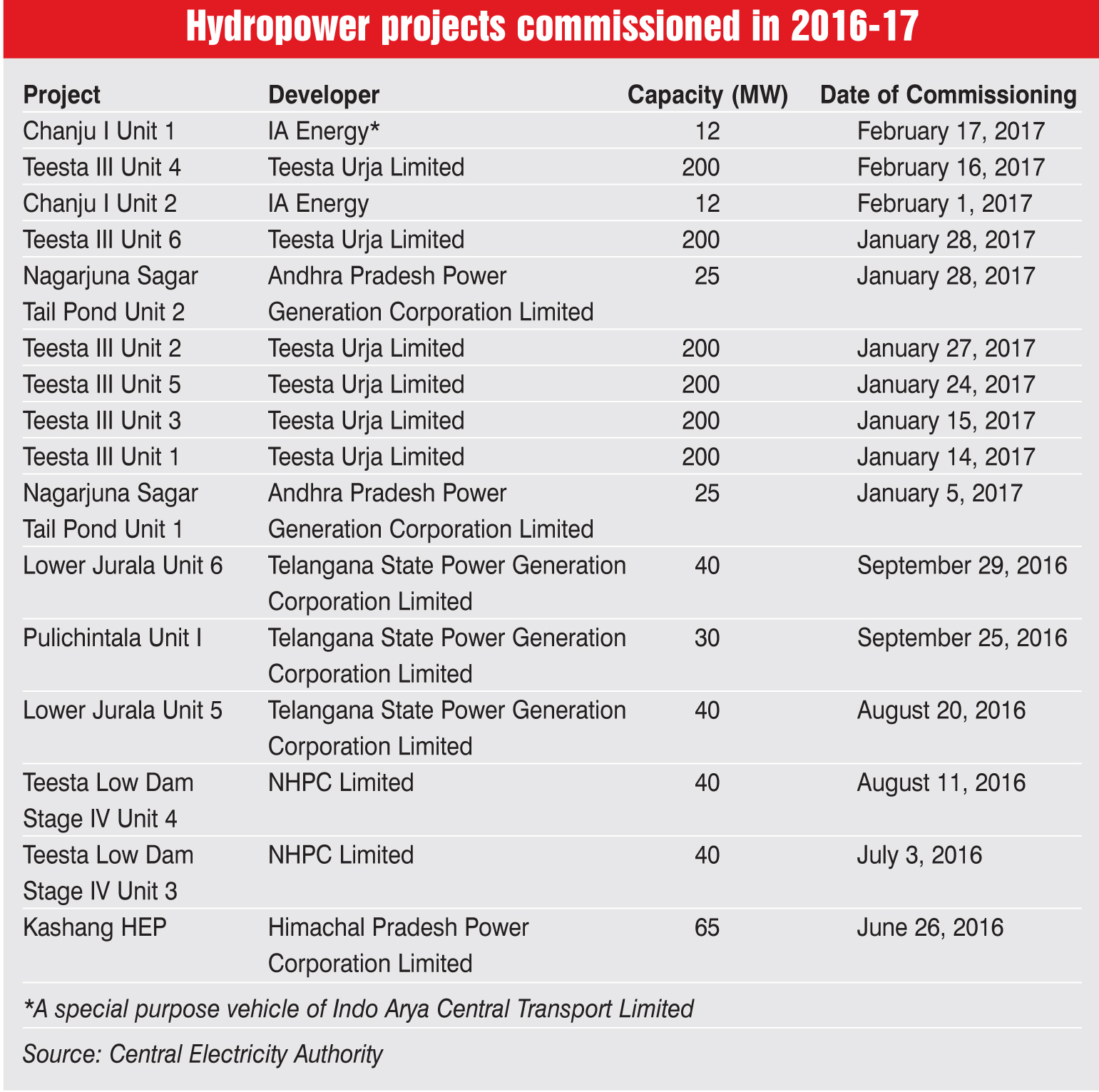

As of March 2017, the installed hydropower generation capacity stood at 44.48 GW, accounting for 13.9 per cent of the total installed capacity (319.6 GW) in India. On a year-on-year basis, the capacity increased by almost 4 per cent in 2016-17, the highest growth witnessed in the past five years. However, the share of hydropower in the total installed capacity has been declining consistently, from 17.7 per cent as of March 2013, to 13.9 per cent as of March 2017. This is because of significantly lower growth of hydropower capacity (compound annual growth rate [CAGR] of 3.01 per cent) in comparison with the growth in the country’s total installed capacity (CAGR of 9.37 per cent) during this period.

Slowdown in capacity addition has been a major challenge for the segment. Every year, the capacity addition has fallen short of the target in varying magnitude. While the actual capacity addition was 37.5 per cent less than the target in 2012-13, it was underachieved by only 1.1 per cent in 2016-17. The capacity addition has also missed the overall target for the 12th Five Year Plan ended in March 2017. Against a targeted addition of 10.9 GW during 2012-17, the actual achievement was around 5.5 GW only.

Region-wise, about 43 per cent of the capacity is located in the northern region, 26 per cent in the southern, 17 per cent in the western, 11 per cent in the eastern, and only 3 per cent in the north-eastern region. With respect to ownership, as of March 2017, 67 per cent of the installed hydropower capacity is owned by the state sector, followed by the central sector with 26 per cent share. Private sector has had a limited participation in the segment with only 7 per cent share in the installed hydropower capacity. About 59 per cent of the capacity is in the form of storage-based plants and 22 per cent in the run-of-river (RoR) plants. The remaining capacity is installed as RoR plants with pondage. The hydro-thermal mix has declined over the years and continues to be much lower than the desired mix of 40:60 from the system availability and reliability point of view. The current hydro-thermal stands at about 86:14, pointing towards the lack of flexible generation required to meet the peak demand.

Hydropower generation

Hydropower generation has showed a mixed performance in the recent years. While the generation has generally been lower than the targets, it was more than the targeted generation in 2013-14 and 2014-15. Over the past five years, the growth in generation has been rather low, with a CAGR of 1.83 per cent. In 2016-17, the generation from hydropower plants was about 122 BUs, only 0.77 per cent higher than that in 2015-16. The share of hydro in the total generation (excluding renewable-based generation) has declined over the past five years, from 12.5 per cent in 2012-13 to 10.5 per cent in 2016-17. The segment’s performance in terms of generation per unit of installed capacity (MUs per MW) has witnessed a cyclical performance in the last five years. However, the overall ratio has declined between 2012-13 and 2016-17. In 2016-17, the MUs per MW stood at 2.75 as against 2.87 in 2012-13.

Pumped storage plants

Given the increasing share of renewable energy in the total generation, and thereby, the need to balance the intermittent generation, the focus on pumped storage plants (PSPs) in India has increased. While the first PSP in India was built in 1970, there has been a limited capacity addition since then. As of March 2017, the installed PSP capacity stood at 4,785.6 MW, of which 2,600 MW is operational across six states and nine plants. These include 240 MW Kadana Stage I and II; and 1,200 MW Sardar Sarovar in Gujarat, 705 MW Nagarjuna Sagar and 900 MW Srisailam in Telangana, 400 MW Kadamparai in Tamil Nadu, 40 MW Panchet Hill in Jharkhand, 150 MW Bhira and 250 MW Ghatgar in Maharashtra and 900 MW Purulia in West Bengal. Further, two projects, namely Tehri Stage-II (1,000 MW) in Uttarakhand and Koyna Left Bank (80 MW) in Maharashtra are under construction and are likely to be commissioned by 2019-20.

Issues and challenges

The challenges deterring the development of hydropower segment include land acquisition issues, environmental impact, opposition from the local population, issues related to rehabilitation and resettlement, lack of enabling infrastructure for power evacuation, and inter-state issues and disputes on water sharing. Delays in the acquisition of land for hydropower projects and opposition from local population have been the major factors causing delays in construction activities. This also leads to significant cost overruns for the projects.

As a result, hydropower plants, which are considered to have the lowest tariffs, have witnessed an upward tariff trend, making state utilities reluctant to buy power from them. Other major bottlenecks in the execution of hydropower projects are the lack of transmission network and other basic supporting infrastructure such as roads and bridges, specifically, in the north-eastern region, where the maximum unexploited potential lies. Owing to the uncertainties associated with hydropower projects, financing activity in the sector has also remained slow. From the financers’ perspective, construction guarantees and performance bonds are required in order to mitigate the risks associated with these projects.

Outlook

About 10.8 GW of hydropower capacity is under construction as of March 2017 and is expected to be completed by 2021-22. About half of this is being developed by the central government. More than 25 per cent (2.8 GW) of the capacity under construction is located in Andhra Pradesh. Other key contributing states include Himachal Pradesh (1.99 GW), Uttarakhand (1.43 GW), Sikkim (1.32 GW) and Jammu & Kashmir (1.26 GW).

To address the challenges facing hydropower and to support its development, the government is working on a comprehensive hydro policy through which it is exploring the possibility of categorising hydro projects as renewable energy. This would help the segment access the incentives being provided to renewable projects such as viability gap funding and compulsory hydro purchase obligations, similar to renewable power obligations. However, it has been in discussions for some time already and remains uncertain when it will be actually notified. Further, the basin-wise review of hydro potential being undertaken by the MoP will provide updated data and will assist planners and developers in hydro development.

In order to bail out hydropower plants that are facing cost and time overruns and do not have adequate funds, the Power Finance Corporation (PFC) is taking various actions such as higher debt-equity ratio of funding (up to 80:20) subject to the viability of the project and depending on its progress; allowing last mile equity to ensure timely completion of the project; restructuring of repayment schedule, in line with the revised project timelines, to allow suitable moratorium period for commissioning and stabilisation of operation (as per the RBI guidelines); and structured repayment options (ballooning/EMI-based, etc.) aligned with the cash flow of the project.

With these measures, the segment is expected to get the desired boost and access to competitive capital. This, in turn, will scale up the development of the segment.