Indian power scenario – Overestimated demand and rise of renewables

Indian power scenario – Overestimated demand and rise of renewables

On the back of rapid capacity addition, India’s total installed capacity has reached 320 GW this March, with coal-based thermal power and renewable energy accounting for 192 GW and 50 GW respectively.

While capacity additions have been largely as per government plans, electricity demand has not grown as much as expected. India’s peak electricity demand was only 160 GW in financial year 2017. The 19th Electric Power Survey indicates a lower peak electricity demand of 245 GW in financial year 2022 as against 298 GW estimated in the 2011 survey. Due to lower demand growth and the consequent excess capacity, the average plant load factor (PLF) of thermal power plants has fallen to 62 per cent in financial year 2016 from about 73 per cent in financial year 2012, and is expected to drop further.

Fuelled by the government’s ambitious target and supported by factors such as payment security, clear land acquisition, etc., renewable power is rapidly becoming economical in India. This has led to a rapid addition in renewable capacity in the last few years. In early 2017, winning bids for solar power hit a record low of Rs 2.44 per kWh, while wind reached Rs 3.46 per kWh as a levellised 25-year tariff, and are likely to fall further. These are prices that both current and upcoming thermal plants will struggle to compete with.

Disruptive change in thermal power and coal mining industry

The Central Electricity Authority (CEA) expects no new coal-based thermal power capacity addition during the period 2017-22. The 50 GW that is already under construction would suffice even for financial years 2022-27. In fact, the under-construction capacity could be under threat of not seeing the light of day. China, which is facing a similar situation, recently stopped the construction of coal-based thermal power plants worth 17 GW.

The complete value chain of coal-based thermal power is getting disrupted with these changes. Power producers and engineering, procurement, and construction (EPC) contractors are embracing renewables relatively easily. However, equipment manufacturers would be the hardest hit. These manufacturers enjoyed orders worth about Rs 85,000 crores per year in the last five years due to continuous capacity additions. With a steep drop in capacity additions to zero, new orders would fall to about Rs 20,000 per year till financial year 2020, with no visibility thereafter. Further, growth in coal mining activity would reduce, thereby constraining the demand for mining equipment, material handling equipment and specialised rolling stock.

Avenues for equipment manufacturers

We have identified four avenues that need to be explored for the survival and growth of equipment manufacturing businesses that are currently dependent on demand from coal-based thermal power generation.

Grow revenue from installed equipment base

Without new orders for equipment, manufacturers need to leverage their installed equipment base to generate revenues. Most Indian equipment manufacturers generate less than 10 per cent of their total revenue from spares, service and maintenance. Best-in-class global engineering companies like FLSmidth generate close to 35 per cent of their revenue from spares, service and maintenance.

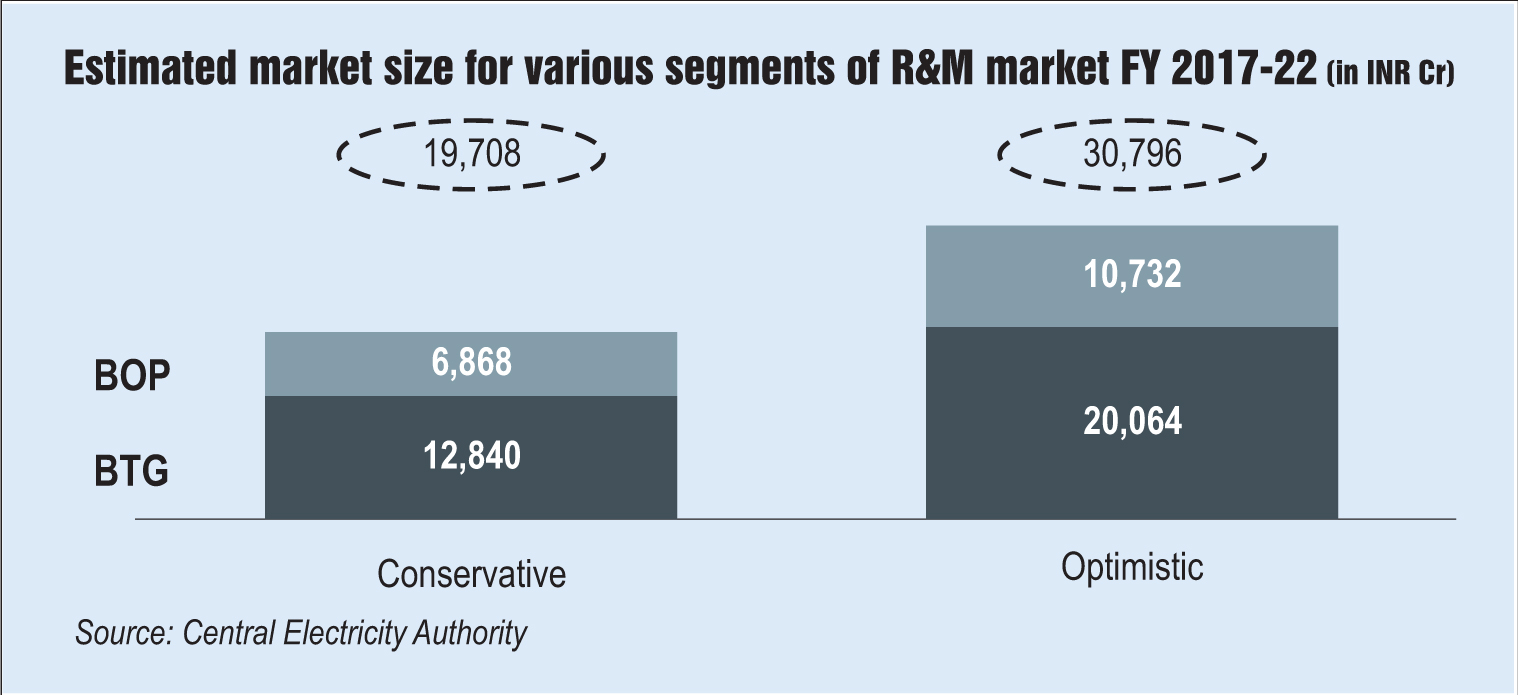

Companies should also focus on aftermarket/replacement demand. Many coal-based thermal power plants in India are old and due for overhaul. Renovation and modernisation (R&M) and life extension (LE) could be attractive opportunities. The CEA estimates the total potential of R&M and LE to be between Rs 20,000 crores and Rs 30,000 crores during financial years 2017-22.

Serve new customer segments with similar products

Companies can leverage the existing know-how to serve new customer segments. For bulk material equipment manufacturers, the attractive areas are steel, non-coal mining, cement and port equipment. Similarly, boiler, turbine and generator (BTG) players can target process plant equipment industry. Companies need to formulate a strategy to consciously increase penetration in these segments.

Secure new export markets

Chinese manufacturers, when faced with overcapacity in power plant equipment manufacturing, exported equipment to India, leveraging their scale, cost and delivery advantages. Indian companies could now adopt a similar strategy. Specific countries in Africa, Central Asia and Latin America could be the major export markets for India for power plant equipment. Working closely with domestic players in these markets could improve competitiveness.

Diversify to new industries

Based on their current capability, bulk material equipment manufacturers need to evaluate new applications like mounting structures for solar projects. BTG manufacturers can explore opportunities in growing sectors such as defence, airport ground handling equipment and railways.

Conclusion

All participants in the coal-based power value chain, from mining to generation, are staring at zero generation capacity addition beyond financial year 2022. Each company will have to customise its response based on its current product portfolio, customer segments served, installed base, synergies with the existing business and the ease with which it can build new capabilities. Companies that embrace this new reality and reinvent themselves will survive and thrive.