With increasing order inflows and high capacity utilisation, the transformer industry is currently on the path to recovery. This can be attributed to various reform initiatives taken by the government to accelerate power sector growth. Indian transformer manufacturers, too, have matured over the years and demonstrated noteworthy technological advancements including the development of equipment of 1,200 kV ratings, the highest capacity power transmission system voltage in the world. A changing energy mix due to greater renewable integration and the growing focus on smart infrastructure have also led to technological innovations in the transformer technology landscape. Power Line presents an overview of the transformer market…

Transmission segment growth

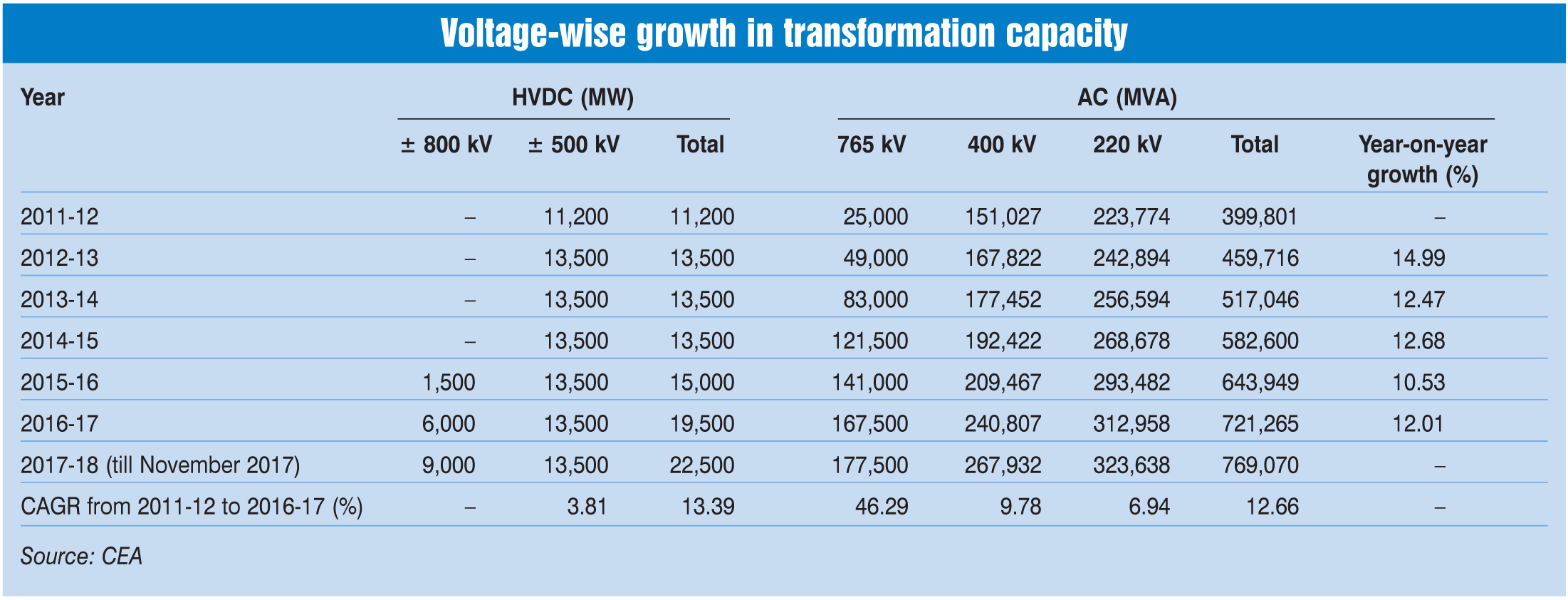

In recent years, the transmission segment has seen significant growth at 220 kV and above voltages. As of November 30, 2017 the total transmission line length stood at 381,671 ckt. km, AC transformer capacity at about 769 GVA and high voltage direct current (HVDC) transformer capacity at 22.5 GVA. Of the total alternating current (AC) transformer capacity, 42 per cent is at the 220 kV level, 35 per cent is at 400 kV and 35 per cent is at the 765 kV level.

The total AC transformer capacity across 765 kV, 400 kV and 220 kV voltages grew at a compound annual growth rate (CAGR) of over 12.6 per cent between 2011-12 and 2016-17. The highest growth was witnessed in the 765 kV category, wherein the transformer capacity increased from 25 GVA to 167.5 GVA recording a CAGR of over 46 per cent. In the HVDC segment while ±500 kV transformer capacity remained constant at 13,500 MVA since 2012-13, significant growth was recorded in the ±800 kV HVDC segment, with the addition of 9,000 MW since 2015-16.

Market size and trends

The total size of the domestic transformer market is estimated at Rs 123 billion in 2016-17, as per the Indian Electrical and Electronics Manufacturers’ Association. Distribution transformers hold a 52.5 per cent share in the market while the rest is held by power transformers. The transformer market consists of few organised players such as Bharat Heavy Electricals Limited, ABB, CG (formerly Crompton Greaves), GE (formerly Alstom) and Transformers & Rectifiers India Limited (TRIL) and several unorganised players.

The transformer industry witnessed strong growth during April-September 2017. The growth index of power transformers stood at 13.2 per cent while that of distribution transformers stood at 7.7 per cent owing to high demand driven by various government schemes as well as exports.

In terms of manufacturing, the overall installed capacity is estimated at about 420,000 MVA. The transformer manufacturing capacity witnessed significant growth during the period 2008-09 to 2013-14, with the production increasing at a CAGR of about 18 per cent as per Edelweiss Research. However, demand started declining post 2012-13 due to economic slowdown and policy paralysis. As a result, the capacity utilisation factor (CUF) declined from 86 per cent in 2008-09 to 47 per cent in 2014-15.

Some revival in demand was seen in 2015-16 when the CUF increased to 55 per cent. The trend in demand growth is expected to continue and reach about 68 per cent by 2017-18 in view of increased spending by Power Grid Corporation of India Limited (Powergrid) and state transmission utilities.

Key drivers

Key drivers

The various reform measures initiated by the government are driving the demand for transmission and distribution (T&D) equipment including transformers. Schemes such as the Deendayal Upadhyaya Gram Jyoti Yojana and the Integrated Power Development Scheme, which are aimed at strengthening sub-T&D networks in rural and urban areas respectively, have resulted in increased transformer demand from utilities as they replace their ageing and inefficient fleet and augment capacity. The Ujwal Discom Assurance Yojana has also improved the financial health of discoms, thereby freeing up funds to invest in the augmentation of distribution infrastructure including lines and transformers.

With the launch of the Saubhagya scheme, which is aimed at extending last mile connectivity to unelectrified consumers across the country, the demand for power and T&D equipment, especially distribution transformers, is set to further increase. Meanwhile, as part of the central government’s Green Energy Corridor programme, launched to facilitate the grid integration of large scale renewable energy at an investment of Rs 380 billion, a significant number of transmission lines and substations are being constructed. The first phase of the programme envisages the construction of an interstate transmission network for connecting 33 GW of solar and wind power, while the second phase will link about 20 GW of capacity.

Also, ambitious solar capacity addition plans, growing focus on HVDC systems and FACTS (flexible AC transmission system), as well as upcoming smart grids and smart cities are creating greater demand for advanced transformers equipped with intelligent electronic devices and HVDC converter transformers. Besides an increase in domestic demand for transformers, exports are expected to increase as transformer manufacturers are looking to secure orders from Africa, Latin America and Southeast Asia.

TBCB projects

Of late, the award of transmission projects through the tariff-based competitive bidding (TBCB) route has slowed down. The value of projects awarded through this route has declined from about Rs 212 billion in 2015-16 to Rs 98 billion in 2016-17. The government has awarded 39 transmission projects through the TBCB route, as of November 30, 2017. Of these, 13 projects have already been commissioned or are ready for commissioning while 22 are under construction. Of the remaining projects, three are stalled due to litigation and other issues and one was cancelled by the Central Electricity Regulatory Commission.

There are currently four projects under bidding – the Transmission Scheme for the Evacuation of Power from Generation Projects in the Kameng River basin; the New Western Region–Northern Region 765 kV Inter-Regional Corridor; the Transmission System for Ultra Mega Solar Park in Fatehgarh; and Connectivity and Long Term Access to Himachal Pradesh Power Corporation Limited from the 450 MW Shongtong Karcham HEP.

Issues and challenges

The key issues affecting the transformer industry are related to the new quality control order, import of cold-rolled grain-oriented (CRGO) steel, absence of standardised specifications, payment delays from state utilities and lack of adequate testing facilities.

As per a notification by the Bureau of Energy Efficiency, the distribution transformer manufacturers in India would now have to obtain a certification from the agency for energy-efficient distribution transformers under the IS:1180 Part 1/2014. The manufacturers already need to apply for a certification from the Bureau of Indian Standards for the same. Now they would require dual certification for the same product, which is a lengthy and costly process. The Indian Transformers Manufacturers Association has requested the Ministry of Power to look into the issue.

Another long-standing issue is regarding CRGO steel, which is used in the manufacture of transformer cores. Manufacturers have to entirely rely on the import of this critical raw material, which accounts for about 35 per cent of the cost of a transformer. The need for setting up a CRGO steel manufacturing facility has been mooted by transformer industry associations at various forums but no concrete steps have been taken by the government on this front.

Also, domestic transformer manufacturers are increasingly facing competition from foreign manufacturers, especially those from China and South Korea as the latter offer a price advantage to consumers. Another concern is the lack of adequate testing facilities for transformers, especially in the high voltage and ultra high voltage segments. There is also a lack of standardisation of specifications. All state utilities have different sets of specifications, even for a repeat order. It becomes difficult for transformer manufacturers to meet these requirements. Utilities need to firm up ratings and technical specifications and define losses, impedance and other parameters. Further, logistical constraints are posing a challenge for transformer manufacturers. As transformer rating is increasing, the size and volume of transformers are also increasing. Meanwhile, the transportation of transformers from the manufacturing facility to the customer location is a task in itself.

The way forward

The demand for transformers is expected to increase in the coming years. As per the Central Electricity Authority’s (CEA) draft National Electricity Plan 2016, an investment of Rs 2,600 billion will be required during the 2017-22 period for the transmission system. Of this, Powergrid is expected to invest around Rs 1,000 billion. CEA estimates the total installed transformer capacity (at 220 kV and above) to reach 979,637 MVA by March 2022. This translates into a significant market opportunity for T&D equipment manufacturers over the next four to five years.