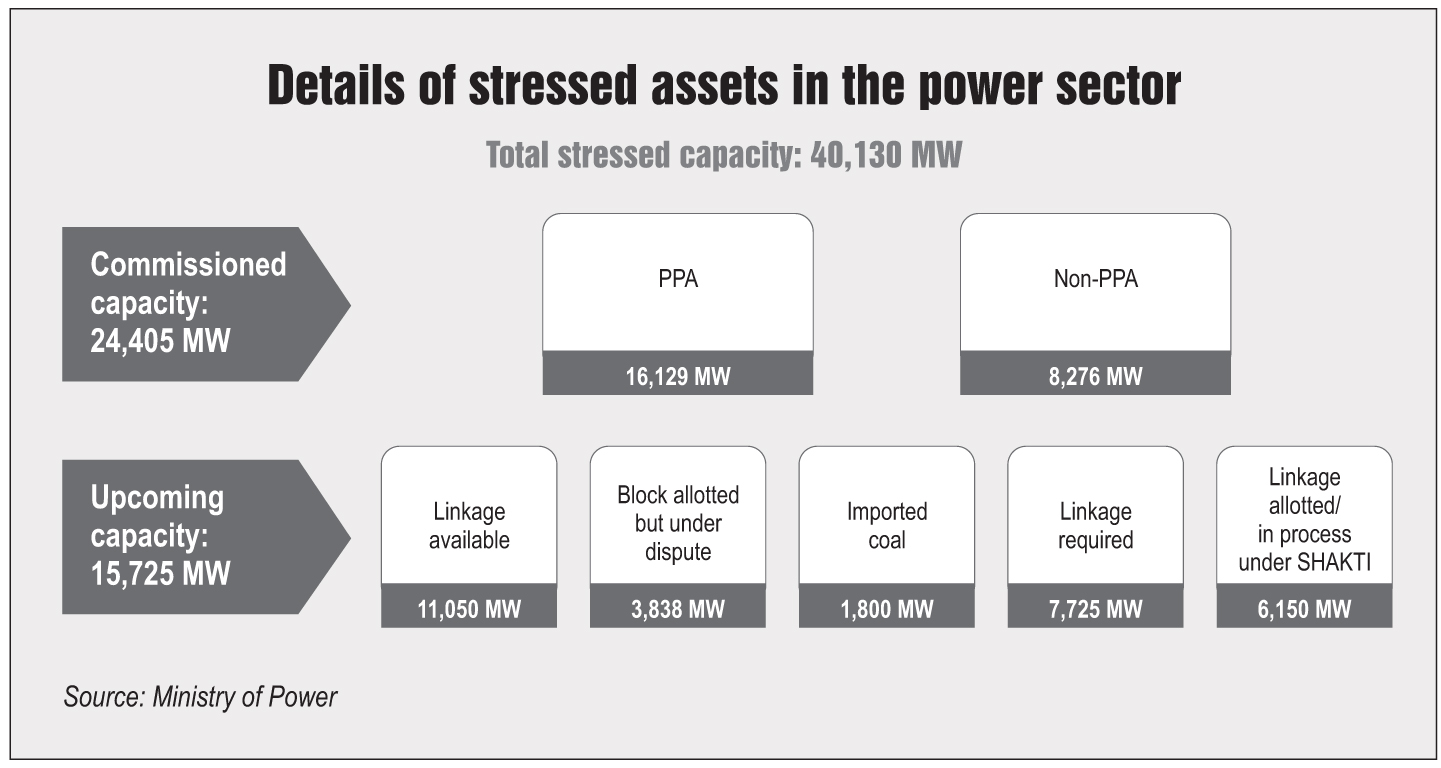

In a significant development, the Reserve Bank of India (RBI) has rejected the Ministry of Power’s (MoP) plea, seeking a reprieve for the power sector from the RBI guidelines issued in February this year.

At a high-level meeting convened on June 21, 2018, attended by senior officials from the finance, power and coal ministries as well as the Association of Power Producers and other industry executives, the RBI has reiterated its stand that stressed assets can be resolved within the time period specified in the February guidelines. These guidelines for the early identification of stressed assets and their resolution had created a furore in the power sector as the failure to meet the strict 180-day timeline for banks to agree on a resolution plan have threatened to push mammoth power assets into the category of NPAs. About 60-70 GW of power projects could fall into this category as per industry estimates. The power ministry had thus requested the RBI to extend the deadline. Meanwhile, given that the build-up of stressed infrastructural assets has been plaguing the banking sector for a while now, a number of models and schemes have been under deliberation by the power and finance ministries, banks, financial institutions and state-owned developers, among others in the past few weeks.

Power Line takes a look at the recent developments in the stressed power assets space…

RBI’s meeting with stakeholders

This month’s meeting was convened in response to a directive issued by the Allahabad High Court after a writ petition was filed in May 2018 by the Independent Power Producers Association challenging the RBI circular. The high court had ordered that no action be taken against the power sector under the revised framework. It further directed the finance secretary to hold a meeting with his counterparts in the power and coal ministries, along with representatives of the RBI and the Insolvency and Bankruptcy Board of India in June to discuss ways to address the issues faced by stressed power plants.

As per news reports, during the June 21, 2018 meeting, the RBI contended that its framework provides enough space for the resolution of bad loans and does not stop the restructuring of assets within the available time frame. A broad consensus emerged on the setting up of a task force of experts to analyse the issues facing the sector regarding fuel supply, power purchase agreements (PPAs) and delays in payments by discoms. The finance secretary has asked the stakeholders to submit their views in writing, after which the next course of action would be decided.

Earlier, the MoP had approached the finance ministry seeking relief for the sector from the RBI’s new guidelines. However, the finance ministry has refused to extend any sector-specific leniency in the execution of the guidelines.

Other strategies in the making

One of the schemes under consideration is the Scheme of Asset Management and Debt Change Structure (Samadhan), which is being formulated by the State Bank of India, Power Finance Corporation (PFC) and other banking institutions. The scheme would cover 11 stressed projects aggregating 12 GW of capacity, with a cumulative debt burden of Rs 800 billion-Rs 900 billion. These projects are either complete or are nearing completion.

Under the Samadhan scheme, the lead lender to the project would appoint the rating agencies (CRISIL and India Ratings & Research) to ascertain sustainable and unsustainable portions of the project debt. The unsustainable debt would be converted into equity to be held by the lender, who could then bid it out to developers willing to run the plants. The existing promoters would not be allowed to hold or retain over 24.5 per cent stake in the project.

Another similar scheme is the Power Asset Warehousing and Revitalisation (Pariwartan) scheme, being formulated by the Rural Electrification Corporation. Under this scheme, a special purpose vehicle (SPV), a subsidiary company to securitise assets, would be set up with PFC and the lending banks. The SPV would be supervised by an asset management company (AMC). The AMC would take on assets aggregating 40,000 MW at the net book value and seek 4-5 per cent of equity from the National Infrastructure Investment Fund to run power projects to service the current debt, and look at breaking even before the lenders decide to take over or sell the assets. The electricity produced during a 48-month period under the plan would also be sold on the power exchanges and short-term PPAs would be sought from the state governments.

Another model for the revival of stressed assets being worked out by the MoP along with public and private financial lenders and NTPC Limited is the warehousing model. The model aims to revive the projects by signing PPAs with the central public sector undertakings and later selling them as profitable assets once power demand picks up. The majority stake in the projects would be retained by the government agencies, which would allow them to change the promoter and project management. The possibility of reviving projects aggregating 45,000 MW, which are completed or nearing completion could be explored under this model. These projects entail an investment of around Rs 4 trillion (Rs 1 trillion in equity and Rs 3 trillion in debt). The operational projects among these are running at a high plant load factor; however, they face the issue of inadequate revenue for servicing debt and require customised solutions for revival.

Stressed asset sale by PFC

To resolve its bad loans, power sector financier PFC has put up four projects in which it has debt exposure for sale to independent power producers (IPPs), financial institutions and private equity firms. These are GMR’s 1,370 MW Raikheda thermal power plant (TPP), KSK’s 2,400 MW Mahanadi TPP, Essar Power’s 1,200 MW Mahan TPP and the Avantha Group’s 600 MW Jhabua TPP.

Close to a dozen Indian and foreign financial institutions and funds, and developers have expressed interest in buying the stressed projects. IPPs such as Adani Power, JSW Energy, NLC India, Torrent Power and Vedanta have evinced interest in the projects. Meanwhile, domestic and global financing agencies such as the Bank of America Merrill Lynch, Edelweiss, JM Financial, Lone Star-IL&FS, Resurgent Power, SC Lowy, Torrent, Varde Partners, SSG Asia, Worlds Window EXIM and National Investment and Infrastructure Fund are likely to place bids for the stressed projects. Global financial institutions and PE-backed funding platforms of power companies such as Lone Star and Resurgent Power are also in the race.

According to industry observers, the heightened interest among financial institutions, IPPs and integrated utilities for these assets is owing to the revised fixed charges following possible haircuts by the lenders. The lenders are expecting to take a haircut of more than 50 per cent, following which the projects would supply power at Rs 2.50-Rs 3 per unit.

Conclusion

Conclusion

Although the generation segment is facing headwinds for now, in the longer run, once power demand picks up with the realisation of huge latent demand and faster economic growth, the stressed TPPs are expected to become viable. That said, in order to avoid distress selling of assets, finalising the best suited model for the resolution of stressed assets at the earliest remains an immediate priority for the sector, since the resolution deadline for some of the plants is September 2018.