India’s generation mix is witnessing a major shift from fossil fuels to renewables. As of August 2023, the country’s installed capacity stands at 424 GW, with conventional sources (thermal and nuclear) and renewable energy sources (including large hydro) contributing approximately 58 per cent and 42 per cent respectively. This is significant, given that just four years ago, in March 2019, the share of conventional sources in the installed capacity mix was 65 per cent, and the share of renewables (including large hydro) was 35 per cent. The expansion of India’s renewable energy is being supported by effective policies and increased investment. This expansion is expected to accelerate with the government’s focus on energy transition and climate change mitigation.

India’s generation mix is witnessing a major shift from fossil fuels to renewables. As of August 2023, the country’s installed capacity stands at 424 GW, with conventional sources (thermal and nuclear) and renewable energy sources (including large hydro) contributing approximately 58 per cent and 42 per cent respectively. This is significant, given that just four years ago, in March 2019, the share of conventional sources in the installed capacity mix was 65 per cent, and the share of renewables (including large hydro) was 35 per cent. The expansion of India’s renewable energy is being supported by effective policies and increased investment. This expansion is expected to accelerate with the government’s focus on energy transition and climate change mitigation.

Along with the changing capacity mix, the power sector dynamics are evolving rapidly. The role of coal-based power plants is shifting from providing baseload power to supporting the balancing of intermittent renewable energy. This requires thermal power plants (TPPs) to be retrofitted and modernised to operate efficiently under flexible conditions. In addition, hydropower holds significant importance in balancing intermittent renewable energy, given its ramping capabilities and black start characteristics. There is a growing interest among developers and investors in pumped storage projects, which is currently the most cost-effective energy storage solution.

An overview of the country’s power generation segment…

Segment growth and performance

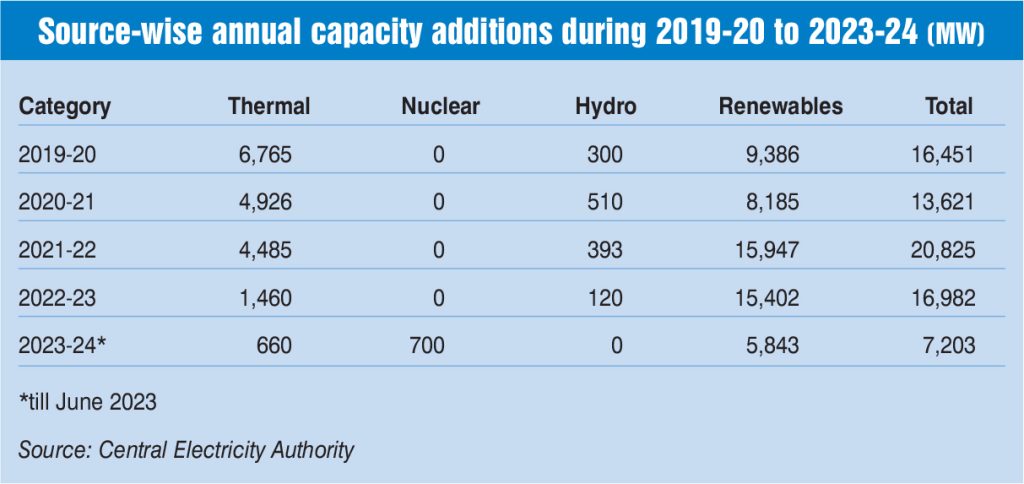

As of August 2023, the total installed capacity in the power sector stood at 424 GW. Fuel-wise, coal- and lignite-based power had the highest share in the total installed power capacity at 50 per cent, followed by solar at 17 per cent. Large hydro contributed to 11 per cent of the capacity, followed by wind at 10 per cent, gas at 6 per cent, bioenergy at 3 per cent, nuclear at 3 per cent and small hydro at 1 per cent. The installed power capacity grew at a compound annual growth rate (CAGR) of 4 per cent between 2018-19 and 2022-23. While conventional power capacity has grown a CAGR of 1.2 per cent during the past five years, renewable energy has grown at a CAGR of 8.8 per cent. Conventional capacity addition has considerably slowed down in recent years, with generators and lenders moving away from coal/gas-based projects due to environmental concerns. Meanwhile, renewable capacity addition has continued to grow due to increased tendering activity, reduced execution risks and cost-reflective tariffs. In absolute terms, around 16,562 MW of net capacity was added in 2022-23, of which 1,159 MW was based on thermal power sources and 15,402 MW on renewables (including large hydro).

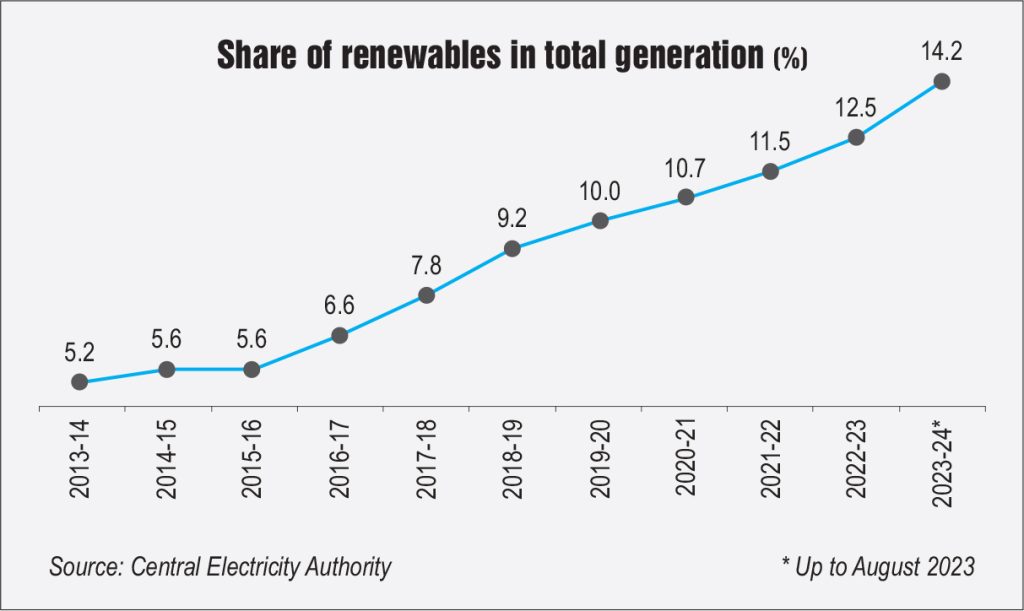

Meanwhile, the total recorded generation (including renewable energy sources) stood was 1,618 BUs in 2022-23. In terms of fuel sources, thermal power accounted for the largest share of the generation mix at 75 per cent, followed by renewable sources at 23 per cent and nuclear power at approximately 3 per cent. The total generation grew at a CAGR of 4.2 per cent between 2018-19 and 2022-23. Thermal generation grew at 3 per cent and renewable energy generation at 12.6 per cent during this period. During 2023-24 (as of May 2023), the total generation has been recorded at 286.18 BUs.

Meanwhile, the total recorded generation (including renewable energy sources) stood was 1,618 BUs in 2022-23. In terms of fuel sources, thermal power accounted for the largest share of the generation mix at 75 per cent, followed by renewable sources at 23 per cent and nuclear power at approximately 3 per cent. The total generation grew at a CAGR of 4.2 per cent between 2018-19 and 2022-23. Thermal generation grew at 3 per cent and renewable energy generation at 12.6 per cent during this period. During 2023-24 (as of May 2023), the total generation has been recorded at 286.18 BUs.

On the operational performance front, the thermal plant load factor (PLF) improved to 64.15 per cent in 2022-23 from 58.87 per cent in 2021-22. This could be attributed to healthy demand growth and limited capacity addition, leading to improved capacity utilisation. During 2023-24 (as of May 2023), the PLF of TPPs has been recorded at 70.26 per cent.

Captive power

According to the Central Electricity Authority (CEA), the installed generation capacity of captive power plants across industries with a demand of over 1 MW has been estimated at 83 GW, as of March 2022. It recorded a CAGR of 9.9 per cent between March 2017 and March 2022. Approximately 61.6 per cent of the installed captive capacity is steam-based, followed by diesel-based (21.4 per cent) and gas-based (8.9 per cent), with the remaining 8.1 per cent comprising renewables and hydro-based plants. Notably, large industries in the metals and mining, cement, and petrochemicals sectors prefer coal-based or natural gas-based plants owing to the economies of scale they offer. Meanwhile, smaller plants (of less than 10 MW) are typically based on solar energy, diesel and other liquid fuels. In recent years, industries have been increasingly focusing on setting up solar-based captive plants due to falling capital costs and zero fuel cost.

Recent developments

- RGO: In February 2023, the Ministry of Power (MoP) notified the renewable generation obligation (RGO),

which mandates power generation companies that own coal- and lignite-based plants with commercial operation dates (CODs) on or after April 1, 2023, to establish renewable power capacity equivalent to at least 40 per cent of their plant capacity, or procure and supply equivalent renewable energy. For generating stations with CODs between April 1, 2023, and March 31, 2025, 40 per cent compliance with the RGO is required by April 1, 2025. Plants with CODs after April 1, 2025, will need to comply with the RGO starting from their CODs.

which mandates power generation companies that own coal- and lignite-based plants with commercial operation dates (CODs) on or after April 1, 2023, to establish renewable power capacity equivalent to at least 40 per cent of their plant capacity, or procure and supply equivalent renewable energy. For generating stations with CODs between April 1, 2023, and March 31, 2025, 40 per cent compliance with the RGO is required by April 1, 2025. Plants with CODs after April 1, 2025, will need to comply with the RGO starting from their CODs. - Scheme for pooling of tariff: In April 2023, the MoP launched a scheme for the pooling of tariffs of efficient coal- and gas-based power generating stations whose PPAs have expired. As per the scheme, effective from July 1, 2023, a genco-wise common pool of power will be created from stations with a lifespan of 25 years or more. Interested state governments or discoms can approach the genco with a letter of intent to procure power from the common pool for a minimum period of five years. The states/discoms will be billed a uniform capacity charge based on the percentage of allocation and the total capacity charge of power from the common pool.

- Revision in biomass co-firing policy: In June 2023, the MoP revised the biomass co-firing policy to facilitate the purchase of biomass pellets by TPPs at benchmark prices. This price benchmarking of pellets will enable both TPPs and pellet vendors to establish a sustainable supply mechanism to facilitate the co-firing of pellets. The benchmarked price will be effective from January 1, 2024. Following the mandate of co-firing biomass with coal in TPPs, approximately 0.21 million tonnes (mt) of biomass fuel has been co-fired in coal-based TPPs, leading to a reduction of over 0.25 mt of carbon dioxide emissions. There are 47 TPPs that have carried out the co-firing of agro-residue-based biomass pellets with coal. The MoP, in a modification issued in June 2023, mandated 5 per cent biomass co-firing in TPPs from 2024-25, which will increase to 7 per cent from 2025-26.

- Order to compensate ICB plants for higher running costs: In order to ensure that power producers maintain and operate their plants, generating power for supply to procurers in compliance with the directions of the MoP under Section 11 (1) of the Act, the Central Electricity Regulatory Commission, in an order dated January 2023, decided to fully compensate power producers operating imported-coal-based (ICB) plants for higher running costs incurred while supplying electricity under forced circumstances. The compensation will cover the costs, along with a reasonable profit margin.

- Flexibilisation: In March 2023, the CEA released a comprehensive report on the flexibilisation of coal-fired power plants. It focuses on operating procedures, challenges, retrofits and a roadmap for achieving a minimum technical load of 40 per cent. As per the report, the flexible operation of coal power plants can be made technically feasible by upgrading and tuning controls. Further, the report proposed a phasing schedule with a minimum period of eight years to ensure that 600 units are compliant, allowing for up to 40 per cent load flexibility and higher ramp rates. The complete refurbishment work is estimated to conclude by December 2030.

- Update on emission norms: In September 2022, the Ministry of Environment, Forest and Climate Change extended the deadline for TPPs to reduce sulphur emissions by two years. For coal-based units that fall under Category A, the deadline for emission norm compliance has been extended till December 31, 2024; for TPP units under Category B, the deadline has been pushed to December 31, 2025; and for other TPPs under Category C, the deadline has been extended till December 31, 2026. This is a major relief for thermal gencos because flue gas desulphurisation systems have been implemented across only 23 units, accounting for 9,940 MW of the total capacity of over 211.52 GW spread across 600 units, as of July 2023.

Issues and challenges

Issues and challenges

In order to integrate growing renewable energy capacity, coal-based TPPs need to flexibilise their operations in order to increase operational efficiency and increase the risk of failure because of wear and tear. TPPs need to undergo retrofits in order to prepare for flexible operations. Another challenge that coal-based plants often face in the power generation segment is the shortage of fuel at power plants. While coal production has been increasing steadily to meet the growing demand, logistical constraints often lead to coal shortage at power plants, particularly during peak power demand seasons. Apart from this, outstanding dues from discoms have hindered the growth of the generation segment. Although there has been some improvement with the implementation of late payment surcharge rules, there is a need to make discoms financially sustainable. As per the PRAAPTI portal (accessed on August 18, 2023), the total outstanding dues of discoms stand at Rs 792 billion. Apart from this, the slow resolution of stressed thermal assets poses a significant challenge in the sector. It is estimated that coal-based capacity of about 41 GW is stressed, owing to issues such as the lack of long-term PPAs, insufficient coal linkages and promoters’ inability to secure funding for project completion.

Future outlook

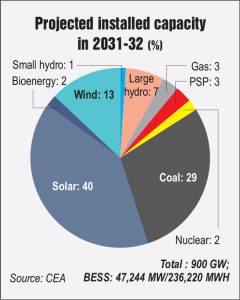

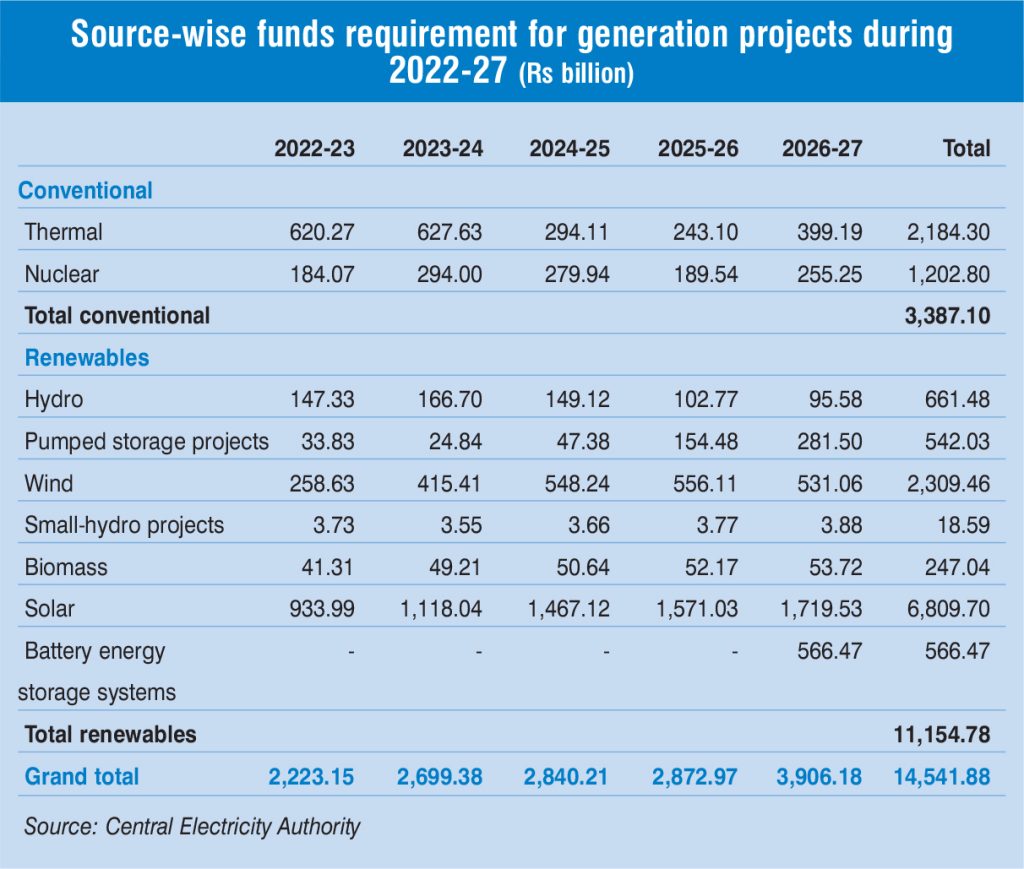

Recently, the CEA notified the National Electricity Plan (NEP), Volume I: Generation, for the period 2022-32. As per the plan, the all-India installed capacity is likely to reach 900,422 MW by 2031-32. The NEP envisages that the share of non-fossil-based capacity is likely to increase to 68.4 per cent by 2031-32, from around 42.5 per cent as of April 2023. Notably, India will not add any new coal capacity in the next five years, except for plants already at various stages of planning. Meanwhile, renewable energy capacity is expected to double the current levels and surpass coal capacity by 2026-27. Overall, the projected total capacity addition aligns with the country’s target to achieve a non-fossil-based installed capacity of 500 GW by 2029-30. The required funding for generation capacity addition is estimated to be Rs 14,541.88 billion for 2022-27 and Rs 19,064.06 billion for 2027-32.

Overall, the power generation segment has a favourable outlook owing to the healthy growth in electricity demand, improved visibility on new PPAs and the implementation of the late payment surcharge scheme, which enables the recovery of overdues from discoms.