The transmission sector in India has undergone a remarkable transformation, transitioning from a fragmented network to a fully integrated and interconnected grid. This sector has made significant strides in terms of enhancing the physical grid infrastructure and adopting advanced technologies, establishing India’s electricity grid as one of the world’s largest synchronised grids. A key driver for the further expansion of the grid is the evacuation of power from upcoming renewable energy projects. Moreover, as electricity demand continues to surge and distribution networks expand, there is a critical need for distribution towers. These structures serve as the backbone of reliable electrical supply systems, facilitating the safe and efficient supply of power. The growing distribution network, driven by urbanisation, industrialisation and the integration of renewable energy sources, has heightened the importance of the installation and maintenance of distribution towers. To meet this demand, utility companies and infrastructure developers are investing in innovative designs, materials and technologies to ensure the resilience and sustainability of the grid, providing reliable power to meet the country’s evolving energy needs.

Given the enhanced focus on the transmission and distribution segments, the importance of critical infrastructure in this space becomes evident, especially for transmission lines and towers. Power Line takes a look at the key trends, growth drivers, issues and challenges in this segment…

Given the enhanced focus on the transmission and distribution segments, the importance of critical infrastructure in this space becomes evident, especially for transmission lines and towers. Power Line takes a look at the key trends, growth drivers, issues and challenges in this segment…

Size and growth

As of September 2023, the total transmission line length (at the 220 kV level and above) stands at 476,547 ckt. km, total alternating current (AC) substation at 1,202 GVA and high voltage direct current (HVDC) system substation at 33,500 MW. Between 2016-17 and 2022-23, the line length has grown at a compound annual growth rate (CAGR) of 4.2 per cent, while AC and HVDC substation capacities have grown at 8 per cent and 9.4 per cent respectively. In absolute terms, about 103,490 ckt. km of lines, 425,587 MVA of AC substation capacity and 14,000 MW of HVDC substation capacity have been added during this period. The interregional transfer capacity has also grown considerably over the years, from approximately 75,050 MW in 2016-17 to 112,250 MW in 2022-23, recording a CAGR of 6.9 per cent.

In order to fast-track the development of the country’s transmission network, tariff-based competitive bidding (TBCB) was introduced in 2006. As of September 2023, 84 interstate transmission network (ISTS) projects have been bid out to public and private players since 2009 under the TBCB mechanism (excluding four cancelled projects or those under litigation). Of these, 32 projects have been secured by Power Grid Corporation of India Limited (Powergrid) and 52 have been won by private players. Of the private sector projects won so far, 30 have been commissioned and the remaining 22 are under construction. Of Powergrid’s projects, 16 have been commissioned and 16 are under construction. The key private players in the transmission segment include Sterlite Power Transmission Limited, Adani Energy Solutions Limited, India Grid Trust, ReNew Transmission Ventures Private Limited and Apraava Energy Private Limited.

Growth drivers

One of the key growth drivers for transmission network expansion and strengthening is the growing renewable energy capacity. It helps evacuate power from renewable energy plants and manage the intermittent nature of renewable energy. Thus, significant transmission network expansion is being carried out under the Green Energy Corridors (GEC) project. With the government’s target of setting up 500 GW and meeting 50 per cent of its energy requirement through renewable energy, by 2030, transmission systems will require significant expansion and strengthening. Besides the evolving energy generation mix, consumers are becoming prosumers since they both consume and produce electricity; and decentralised generation of energy is witnessing increasing uptake. Together, they make the grid even more complex as it becomes the centre of both generation and consumption. In the future, there will be a need to manage bidirectional flows and multiple feeding points, making green grids and GECs even more important.

Another growth driver for transmission infrastructure is the government’s focus on creating a regional power grid to optimally utilise resources in the South Asian region and stabilise the Indian grid in the wake of the increasing share of renewables. The existing cross-border interconnections have a transmission capacity of about 4,230 MW. This capacity is planned to be increased to about 6,450 MW progressively over the next few years. Several interconnections have been planned between India and neighbouring countries, including a new 765 kV Katihar-Parbatipur-Baranagar link between India and Bangladesh; and the 400 kV New Gorakhpur-New Butwal transmission line between India and Nepal. Additionally, India and Nepal plan to expand the capacity of the 400 kV Dhalkebar-Muzaffarpur cross-border transmission line to transmit up to 1,000 MW of power, up from the previously agreed upon 800 MW. Further, there are plans to develop an overhead electricity link with Sri Lanka, after the earlier proposal to set up an undersea power transmission link was shelved due to its high cost.

Another key trend would be the focus on offshore wind transmission. India has set a goal of installing 37 GW of offshore wind energy by 2030, primarily off the coasts of Gujarat (Gulf of Khambhat) and Tamil Nadu (Gulf of Mannar). Further, the Indian government has taken a proactive stance towards the early construction of infrastructure for the hydrogen economy in the nation. While the planned transmission system will be sufficient for the early green hydrogen production initiatives, as production increases and more prospective areas for renewable energy emerge, additional transmission systems will be designed and prioritised for deployment. Further, to fast-track transmission development, the Ministry of Power (MoP) has set a target of completing the development of 27,000 ckt. km of ISTS lines under the PM Gati Shakti National Master Plan by 2024-25. The proposed transmission projects under the programme are expected to further facilitate the evacuation of power from generation projects.

The demand for transmission equipment will also come from the renovation and modernisation of sub-transmission networks. As per the MoP’s order in 2021, all 33 kV systems, which are currently maintained by state distribution companies, will be brought under the state transmission utilities in a phased manner to facilitate better planning, loss reduction and increased supply reliability.

Technology trends

There have been significant improvements in transmission tower designs and these developments have reduced the right-of-way requirement, minimised the visual impact, enabled faster execution and provided ease of installation. With new designs, it has become easier to expand the transmission network to remote areas.

Technology upgrades in tower foundation designs are being carried out by utilities through the implementation of multicircuit multivoltage solutions, which involves upgrading the transmission lines with multiple voltage circuits on the same tower. To upgrade the voltage, line capacity is increased by changing the system voltage from a lower value to a higher value in the same corridor. The power transfer capacity can be increased by over four times using this technology. Moving forward, there is a need for utilities to adopt tower designs that can withstand natural disasters such as emergency restoration system towers and monopoles with smaller spans in disaster-prone areas.

Outlook

Significant investments are required to strengthen and ramp up the country’s transmission infrastructure to meet future peak loads as well as to integrate expanding renewable energy capacity. The National Infrastructure Pipeline has estimated a capex of about Rs 3,040 billion for the power transmission segment between 2020 and 2025. State utilities are expected to lead the transmission segment with a projected capex of Rs 1,900 billion.

The planning and execution of transmission infrastructure has taken centre stage with the goal of improving renewable energy evacuation. The Central Electricity Authority released a report titled “Transmission System for Integration of over 500 GW RE Capacity by 2030”, planning a transmission system for about 537 GW of renewable energy capacity in major renewable energy-potential zones, including the Leh renewable energy park in Ladakh; Fatehgarh, Bhadla and Bikaner in Rajasthan; the Khavda renewable energy park in Gujarat; Anantapur and Kurnool renewable energy zones in Andhra Pradesh; and offshore wind farms in Tamil Nadu and Gujarat.

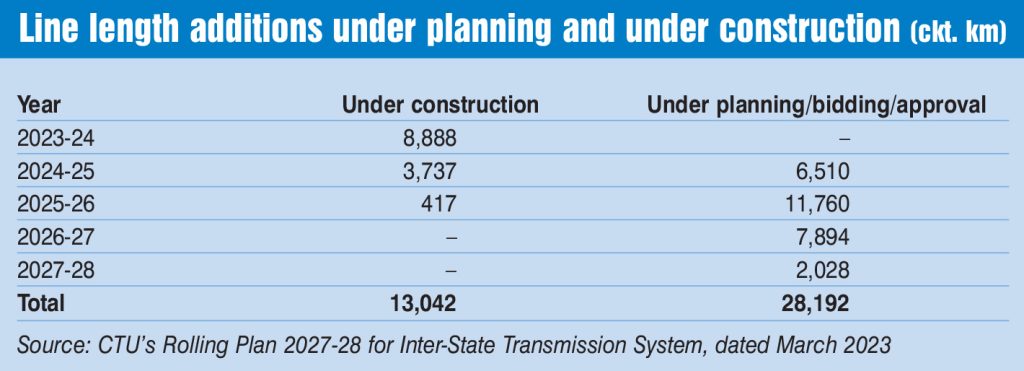

There is a significant pipeline of projects under bidding, primarily for evacuation of power from renewable energy-potential zones, to be implemented in TBCB mode. Currently, 31 transmission projects have been notified for bidding by PFC Consulting Limited and REC Power Development and Consultancy Limited. Of these, five are intra-state projects, while the remaining 26 are inter-state projects. Meanwhile, as per the ISTS rolling plan 2027-28, 13,042 ckt. km of transmission line length is under construction and 28,192 ckt. km of line length is under planning.

Overall, the transmission tower and structure segment is experiencing robust growth, driven by the ever-increasing electricity demand, grid modernisation, technological advancements, infrastructure investment, rural electrification and cross-border energy trade. Given the increased focus on the transmission segment, the role of critical infrastructure in this space, particularly transmission lines and towers, has become even more critical. In order to address this escalating demand, transmission tower manufacturers will need to continue their efforts to innovate, pioneer new technologies and embrace emerging trends.

Akanksha Chandrakar