India’s power sector is witnessing a significant transformation, driven by the rapid integration of variable renewable energy into the grid. This transition has disrupted traditional load patterns, creating an urgent need for greater flexibility in grid operations. In response, utilities are increasingly adopting stand-alone battery energy storage systems (BESSs) across the power sector supply chain, encompassing generation, transmission and distribution. For utilities, BESS is emerging as a key enabler for meeting peak power demand, ensuring power quality, supporting renewable integration and enhancing overall grid reliability.

The rationale behind this lies in the evolving nature of India’s electricity demand curve, which has become significantly peakier. While solar generation peaks in the afternoon when demand is relatively low, the demand surges in the evening hours when solar output declines sharply. This mismatch between supply and demand has created a need for storage solutions that can bridge this gap.

Given the limitations of thermal plants in ramping up and down quickly, the evening peak deficit poses significant operational challenges for grid operators. The absence of flexible generation leads to curtailment of surplus solar during the day. This is where BESSs prove crucial, as these systems can store excess solar power during the day and discharge it in the evening to meet the peak demand, thereby avoiding both curtailment of renewables and inefficient coal cycling. Thus, BESS offers a viable solution by supporting grid balancing and enhancing renewable energy utilisation.

Recognising this, the government has given a strong push to the BESS segment through the viability gap funding (VGF) scheme launched in March 2024, with an initial target of 4 GWh. With battery prices falling, the scheme has been rapidly scaled up, first to 13.2 GWh in early 2025 and then by an additional 30 GWh sanctioned in June 2025, taking the approved capacity to over 40 GWh. Backed by an outlay of Rs 54 billion, the scheme is expected to mobilise Rs 330 billion in investments and help meet the country’s storage requirements by 2028. To benefit from this, several states have issued a series of standalone BESS tenders in recent months. According to Renewable Watch Research, around 12 tenders have been auctioned since January 2025. This article provides an overview of tenders that have been auctioned since January 2025…

Auction trends

Auction trends

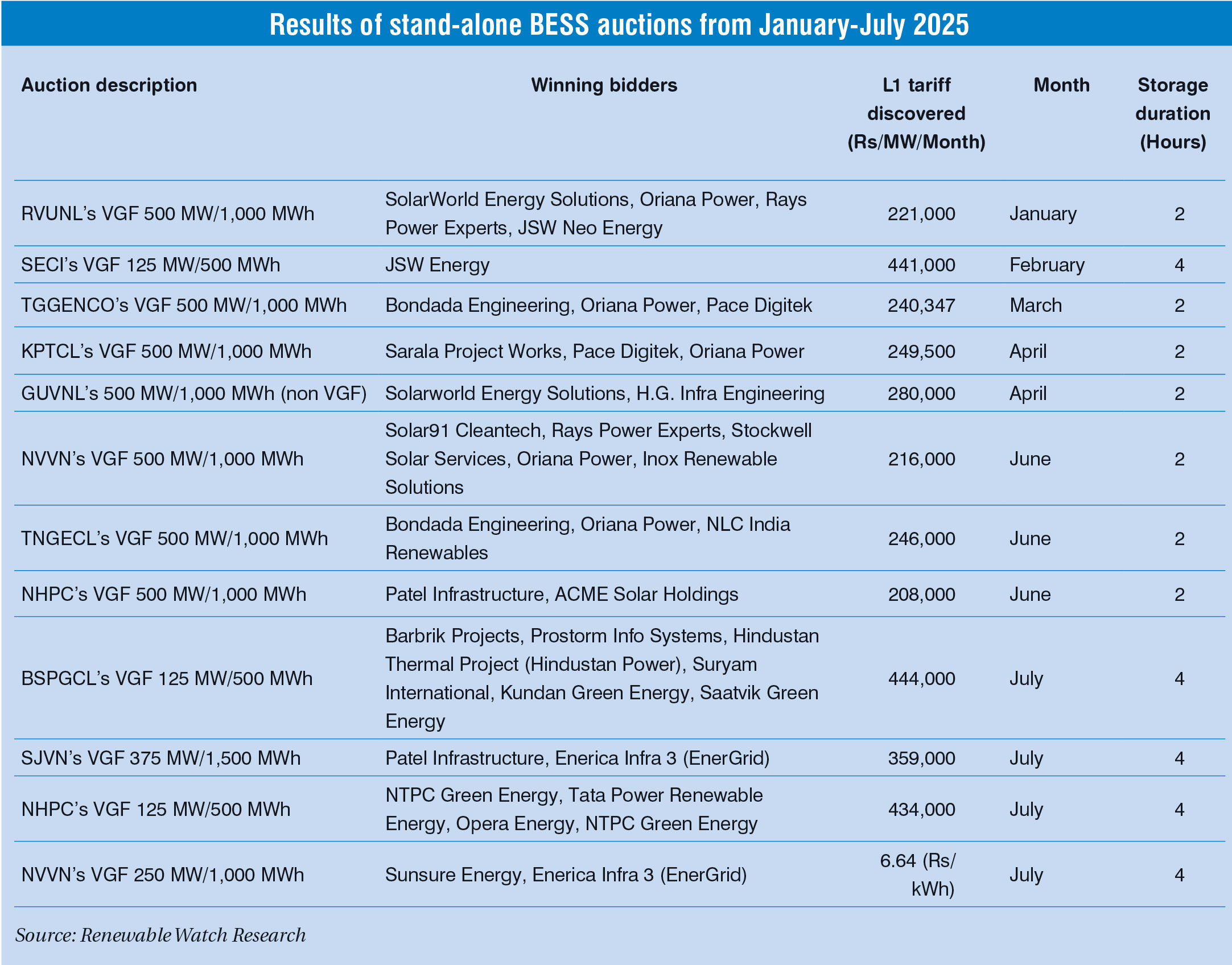

India’s recent stand-alone BESS auctions have highlighted distinct tariff patterns influenced by VGF support and storage design, as seen in the table.

The discovered tariffs for two-hour storage projects, including both VGF and non-VGF-based tenders, ranged between Rs 208,000 per MW per month and Rs 280,000 per MW per month. The winning bidders comprised a diverse mix of established renewable energy developers, engineering firms and new entrants, highlighting growing competition and confidence in the BESS segment. NHPC’s VGF-backed tender for 500 MW/1,000 MWh capacity recorded the lowest bid at Rs 208,000 per MW per month. Meanwhile, GUVNL’s non-VGF 500 MW/1,000 MWh tender discovered a tariff of Rs 280,000 per MW per month.

Longer duration projects with a four-hour storage capacity have also been auctioned during the year. These projects yielded higher tariffs than their two-hour counterparts, mainly due to doubling of the storage requirement. The tariff for such projects ranged from Rs 359,000 per MW per month to Rs 444,000 per MW per month, for SJVN’s VGF 375 MW/1,500 MWh capacity auction and BSPGCL’s VGF 125 MW/500 MWh capacity auction, respectively.

Future outlook

The year 2025 has been quite eventful, witnessing successful auctions and the discovery of competitive tariffs. There has also been an uptick in tender activity for stand-alone BESS, which is encouraging for the market. Going forward, the momentum in the storage market is expected to grow with the decline in battery prices and initiatives such as production-linked incentives, VGF and evolving regulatory instruments such as energy storage obligations, which are providing the necessary fillip.

A major challenge is the sourcing of battery cells, as highlighted by Debmalya Sen, President, India Energy Storage Alliance. Almost all winning developers continue to import battery packs, primarily from China, given India’s limited domestic manufacturing capacity. For this, Sen shared that the government should explore mechanisms such as the Approved List of Battery Manufacturers, akin to the Approved List of Models and Manufacturers for solar modules.

Going forward, the outlook for the BESS market remains optimistic, especially as the economics of storage continue to improve and grid flexibility becomes non-negotiable in a renewables-dominated future. With India’s BESS auction pipeline rapidly expanding, it will be interesting to see whether this momentum can be sustained in the coming years.

Preeti Wadhwa