India’s short-term power market maintained its upward trajectory in 2024-25, driven by higher demand, new technologies and supportive policies, which have improved liquidity, flexibility and market access for discoms, generators and open access consumers. The rapid scale-up of the real-time market (RTM) has enabled participants to manage procurement closer to delivery, while green market platforms such as the green day-ahead market (G-DAM) and the green term-ahead market (GTAM) are accelerating renewable energy integration. At the same time, the growth of ancillary service markets has strengthened grid reliability, and reforms such as virtual power purchase agreements (VPPAs), carbon credit trading and electricity derivatives are creating new avenues for hedging and compliance.

Looking ahead, the Central Electricity Regulatory Commission’s (CERC) plan to introduce market coupling from January 2026 is expected to be a structural turning point, enabling uniform clearing prices across exchanges and enhancing market liquidity. However, persistent challenges such as recurring price crashes in the RTM underscore the urgent need for storage and demand-side flexibility to ensure the long-term stability and resilience of the trading ecosystem.

Power Line presents a round-up of the key trends and developments in the power trading market during the past year…

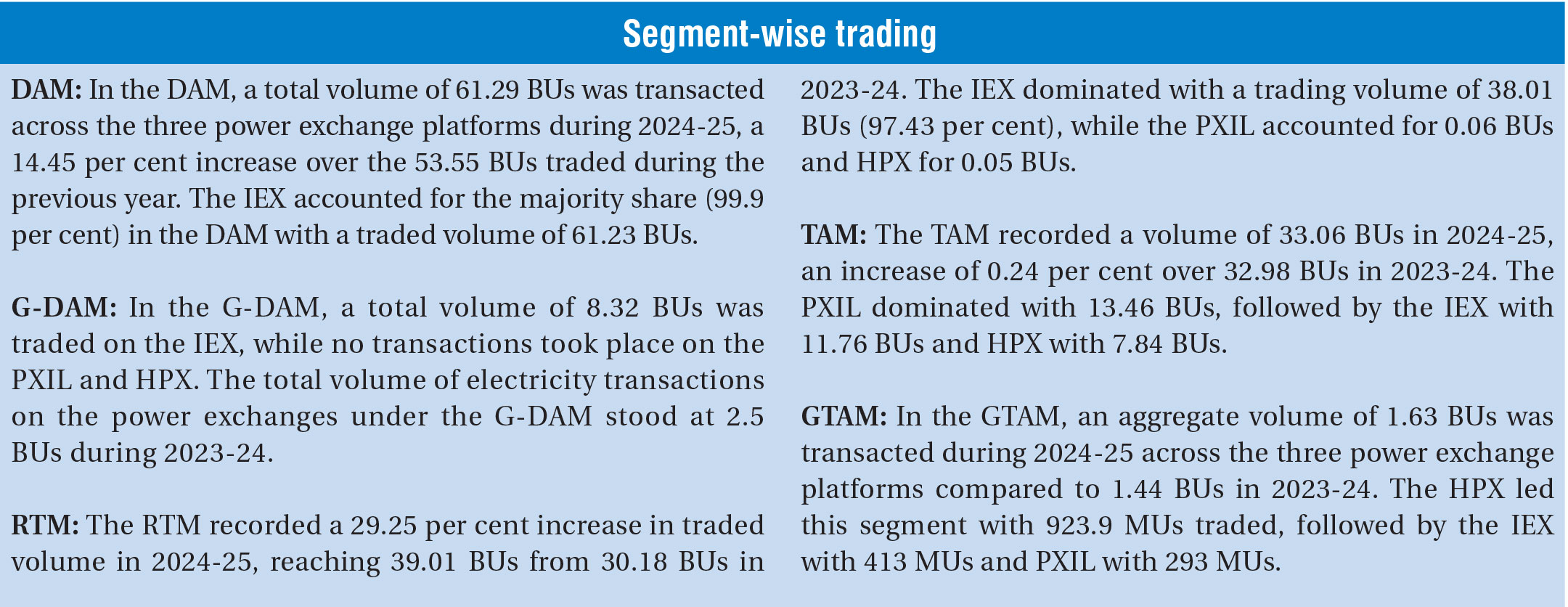

Power exchange and bilateral transactions

The total volume of short-term electricity transactions, including the deviation settlement mechanism (DSM), increased from 65.9 BUs in 2009-10 to an all-time high of 238.35 BUs in 2024-25. Year on year, this marked a growth of 9.22 per cent over the 218.22 BUs registered in 2023-24. Short-term trading and DSM together accounted for about 15 per cent of total electricity generation in FY 2025.

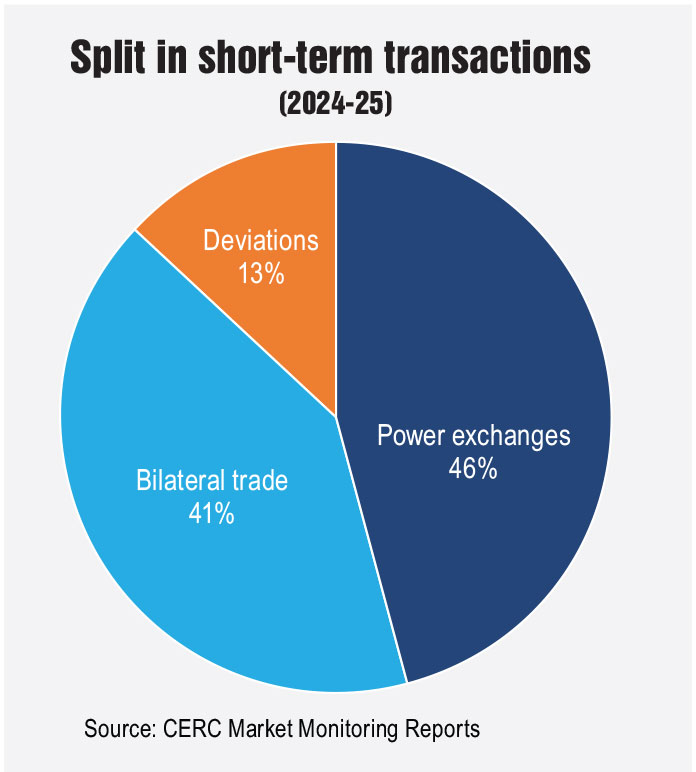

During 2024-25, a total of 1,572 BUs of electricity was supplied in the country. Of this, 108.62 BUs was traded through the three power exchanges (Indian Energy Exchange Limited [IEX], Power Exchange India Limited [PXIL] and Hindustan Power Exchange [HPX]), 97.58 BUs was transacted through bilateral trade, and 32.14 BUs was transacted through deviations. In comparison, in 2023-24, the total supply was 1,739.09 BUs, including 121.49 BUs through the power exchanges, 69.94 BUs through bilateral trade and 26.78 BUs through deviations, reflecting a shift in the composition of short-term transactions.

Electricity traded through traders stood at 41.02 BUs during 2023-24, accounting for 18.8 per cent of the total transaction volume in the short-term market. This marked a 21.36 per cent increase from the 33.8 BUs recorded in the previous financial year. During 2023-24, 4 per cent of the electricity volume transacted through traders was priced below Rs 5 per kWh while 91 per cent was priced below Rs 9 per kWh. The weighted average trading margin charged by trading licensees in 2023-24 stood at Re 0.029 per kWh, in line with the CERC Trading License Regulations, 2020.

The total size of the bilateral electricity market (through traders) and the power exchange market increased from Rs 176.22 billion in 2009-10 to Rs 1,007.29 billion in 2023-24, recording a CAGR of 13.3 per cent.

Price and volume behaviour

Price and volume behaviour

In 2024-25, the DAM maintained steady liquidity, with monthly volumes ranging from 4,131 MUs in April 2024 to a peak of 6,643 MUs in December 2024. Weighted average prices, however, trended downward for much of the year, slipping from Rs 4.63 per kWh in April 2024 to Rs 3.52 per kWh in November 2024, before stabilising in the Rs 4.20-Rs 4.40 per kWh range in early 2025. The PXIL and HPX saw limited DAM participation, with higher price volatility due to thin trading.

The RTM recorded strong growth, with the IEX’s monthly volumes ranging from 2,628 MUs (April 2024) to a peak of 3,913 MUs (September 2024). On the price side, RTM clearing rates broadly tracked day-ahead levels but were more volatile due to the segment’s closer alignment with real-time supply-demand fluctuations. The weighted average prices at the IEX started at Rs 4.78 per kWh in April 2024, but softened through the monsoon months to Rs 3.42 per kWh in November 2024, and recovered modestly in early 2025. By March 2025, RTM prices were hovering around Rs 4.10-Rs 4.30 per kWh. The prices on the PXIL and HPX, however, touched Rs 9-Rs 10 per kWh.

Recently, the IEX RTM witnessed frequent price crashes, even during peak summer, due to unseasonal rains, cooler temperatures and surplus generation from thermal, hydro, solar and wind sources. For example, on May 25, 2025, prices fell to near zero between 09:00 and 13:00, as sell bids outnumbered buy bids fivefold, dropping below the exchange fee of Re 0.02 per kWh. This reflects a deeper supply-demand imbalance, particularly affecting solar developers, as India still lacks a demand response market. This highlights the growing need for battery energy storage systems (BESSs) to store surplus energy during low-demand periods and release it during peaks.

The TAM reflected more balanced participation across the exchanges. On the IEX, monthly volumes were largely stable in the 1,100-1,400 MUs range, while the PXIL registered sizeable flows towards the year end, crossing 1,500 MUs in February 2025 and 1,700 MUs in March 2025. Prices in the TAM remained higher than the DAM/RTM, hovering around Rs 6-Rs 9 per kWh, reflecting the premium attached to forward procurement. The PXIL largely mirrored this trend, while the HPX saw occasional spikes near Rs 10 during September-October before easing.

In the GDAM, trading was concentrated on the IEX, with volumes peaking at around 968 MUs in July 2025 and remaining strong during May-August, in line with higher renewable injections. Prices followed DAM trends but at consistently lower levels, falling from Rs 4.36 per kWh in April 2024 to the Rs 3.20-Rs 3.60 per kWh band by late 2024, before recovering to Rs 4.31 per kWh in February 2025. The PXIL and HPX participation was negligible, often leading to sporadic and higher price signals due to thin liquidity.

The GTAM remained modest, with the IEX and PXIL clearing volumes in the tens of MUs, while the HPX reported marginally higher volumes. Prices hovered in the Rs 5-Rs 8 per kWh range on the IEX, commanding a premium over the GDAM due to its longer-term contracting nature. the PXIL registered scattered trades at comparable levels, while the HPX fluctuated more widely due to thin participation.

High-price products remained niche. HP-DAM recorded negligible activity, but whenever trades occurred, prices hit the regulatory ceiling of Rs 12-Rs 15 per kWh, underscoring its role as an emergency tool during stress events. HP-TAM displayed similar patterns, with episodic trades clearing at Rs 14-Rs 17, mainly on the PXIL and HPX during April-May 2024.

Renewable energy certificates

Renewable energy certificates

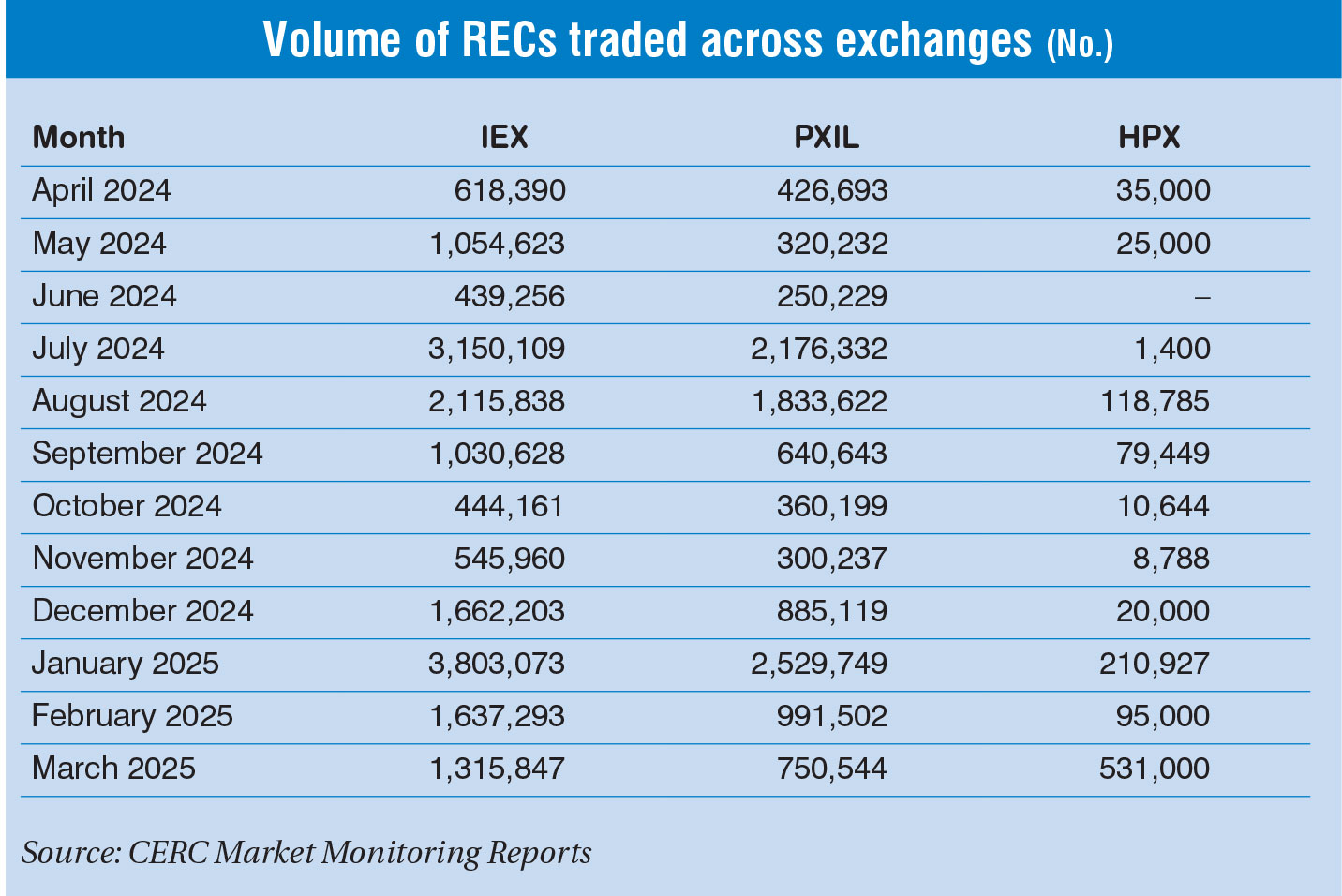

According to the CERC Annual Report on Market Monitoring, 11.6 million renewable energy certificates (RECs) were transacted in 2023-24. Based on data collated from monthly reports, a total of 30.42 million RECs were traded on the exchanges in 2024-25.

The volume of RECs transacted through trading licensees increased from 0.09 million in 2022-23 to 2.19 million in 2023-24, whereas the weighted average price of these RECs declined from Rs 925 per MWh in 2022-23 to Rs 452 per MWh in 2023-24.

ESCerts trading

The Perform, Achieve and Trade (PAT) mechanism, a market-based initiative launched by the government, is designed to improve energy efficiency across industries. Under this system, energy-intensive industries are identified as designated consumers (DCs) and are assigned specific energy efficiency targets. DCs that exceed their targets are awarded energy saving certificates (ESCerts), while those that fall short must purchase ESCerts to cover the shortfall. In FY 2025, a total of 69,935 ESCerts were traded on the IEX.

Cross-border update

India’s cross-border electricity trade remained active in 2024-25, with imports of 4,466.45 MUs from Bhutan and 497.23 MUs from Nepal, while exports to Bangladesh and Myanmar stood at 8,118.27 MUs and 9.01 MUs respectively.

On the IEX DAM, neighbouring countries, including Nepal and Bhutan, purchased 409.2 MUs, while no electricity was sold by them. No cross-border transactions were recorded on the PXIL and HPX. In the IEX RTM, neighbouring countries sold 3.42 MUs and purchased 87.32 MUs under cross-border trade. Similarly, the PXIL and HPX did not record any cross-border transactions during this period.

A major milestone was achieved in November 2024 with the implementation of the tripartite energy trade agreement between Nepal, India and Bangladesh, enabling Nepal to export surplus hydropower to Bangladesh through India’s transmission network. Further, Bangladesh continues to import electricity from India through NVVN Limited and Adani Power, although the latter faces challenges in recovering dues following the political crisis in Bangladesh in August 2024. India’s role as a regional facilitator is reinforced by its extensive cross-border transmission links (11 kV-400 kV) with neighbouring countries, supporting bilateral flows with Bhutan and Nepal and supplying them power during lean hydro periods.

Regulatory updates

Regulatory updates

In September 2025, the CERC notified the draft CERC (Terms and Conditions for Renewable Energy Certificates for Renewable Energy Generation) (First Amendment) Regulations, 2025. The draft amendments proposed key changes to align the REC framework with evolving market structures and compliance mechanisms. As per the amendments, captive renewable energy generating plants used for self-consumption that do not fulfil conventional captive criteria have been brought under the REC framework.

In July 2025, the CERC issued a suo motu order to roll out market coupling under its Power Market Regulations, 2021. The plan is to synchronise the DAM across all power exchanges using a round-robin system by January 2026, while the RTM and TAM coupling will be tested later via shadow pilots. The move is expected to introduce uniform prices across exchanges, improve price discovery, enhance market liquidity and create a more level playing field for participants.

In the same month, the Securities and Exchange Board of India approved the launch of monthly baseload electricity derivatives on the Multi Commodity Exchange and the National Stock Exchange (NSE). The MCX launched its contracts on July 10, 2025, followed by the NSE on July 14, 2025. To encourage participation, both exchanges have introduced incentives such as liquidity schemes and fee waivers. These contracts provide generators, discoms and large consumers with a mechanism to hedge against price volatility from demand, weather and fuel costs, strengthening India’s electricity derivatives market.

In June 2025, the CERC released draft amendments to the Power Market Regulations, 2021. These recognise VPPAs, expand over-the-counter markets to include battery storage and banking contracts, and enhance regulatory oversight. The reforms are aligned with new transmission access rules and are expected to deepen liquidity, accelerate renewable procurement and improve operational flexibility. In May 2025, the CERC issued draft guidelines for VPPAs, offering corporates a flexible route to meet renewable obligations through bilateral contracts.

In April 2025, the CERC passed a suo motu order, titled the CERC (Power Market) (Revised Trading and Contract Design) Order, 2025, under the CERC (Power Market) Regulations, 2021, to standardise short-term electricity contracts and improve efficiency in power trading across exchanges. In the day-ahead contingency segment, exchanges are now required to use a uniform price step auction mechanism instead of continuous matching, enhancing transparency and preventing price manipulation. For the TAM, all custom and overlapping time slots, including those under the green TAM and the HP TAM, are to be discontinued, with exchanges reverting to standard hourly blocks to consolidate liquidity.

In January 2025, the CERC issued the draft CERC (Cross Border Trade of Electricity) (Second Amendment) Regulations, 2024, under the Electricity Act, 2003. The draft introduced key amendments to the 2019 regulations to streamline processes in line with the general network access principles for cross-border electricity trade.

In November 2024, the CERC notified the draft CERC (Terms and Conditions for Purchase and Sale of Carbon Credit Certificates) Regulations, 2024 to create a framework for the exchange of carbon credit certificates (CCCs) for both obligated and non-obligated entities on the power exchanges. As per the draft, the Grid Controller of India will act as the registry for CCC exchanges. The Bureau of Energy Efficiency will manage the CCCs under the Energy Conservation Act. It will collaborate with the CERC on transactions, compliance and information sharing with stakeholders. The CCCs will be traded monthly on the power exchanges, divided into compliance and offset markets, with trading limits based on each entity’s CCC holdings to prevent defaults.

Outlook

India’s power trading ecosystem is undergoing a significant transformation, driven by rising market volumes, green energy integration and progressive regulatory reforms. Market-based mechanisms such as the DAM, RTM and GDAM are gaining traction. Yet, challenges such as price volatility and oversupply, particularly in real-time markets, highlight the need for demand-side flexibility and storage solutions such as BESS.

A key step forward is the proposed introduction of the green RTM, which will enable the real-time trading of renewable energy. This will ensure better balancing of variable generation with demand, enhance grid stability and accelerate the integration of clean energy into the system.

Recent regulatory moves, including electricity derivatives, VPPAs and carbon credit trading, represent significant strides towards a mature, transparent and risk-resilient market. Going forward, deeper digitalisation, advanced grid-balancing tools and cross-border trade will be essential to building a competitive and sustainable power market aligned with India’s clean energy goals.

Aastha Sharma