Battery energy storage systems (BESS) are emerging as a critical enabler of India’s energy transition as the power system grapples with rising renewable energy penetration and associated grid stability challenges. With the rapid expansion of solar and wind capacity, maintaining grid reliability becomes increasingly complex at higher levels of renewable integration, making storage essential for balancing intermittency. By storing surplus renewable generation during low-demand periods and discharging during peak hours, BESS supports renewable integration, peak demand management and grid reliability, while also helping avoid high-cost, variable power procurement.

In addition, BESS contributes to cost optimisation by reducing exposure to volatile short-term market prices and aligns with national and state clean energy targets, including renewable consumption obligations. Given its critical role, BESS is projected to scale significantly in India over the long term, with battery-based systems expected to complement pumped-hydro storage, support renewable energy growth and enhance system resilience.

Key policies and regulations

In line with the Ministry of Power guidelines, the second tranche of the viability gap funding (VGF) scheme was announced in June 2025 to support 30 GWh of BESS capacity, signalling a transition from regulatory enablement to large-scale, implementation-driven deployment.

The VGF for BESS proposes to develop 4,000 MWh of BESS capacity by 2030–31 with budgetary support of up to 40 per cent of capital costs and a total outlay of Rs 94 billion, including direct budgetary support of Rs 37.6 billion. This framework has since been expanded with the MoP extending VGF support to cover a total BESS capacity of 13,220 MWh across the central public sector undertaking, state and Power System Development Fund components, involving implementing agencies such as NVVN Limited, Solar Energy Corporation of India Limited, NTPC Limited, NHPC Limited and SJVN Limited.

In parallel, successive MoP orders issued between November 2021 and June 2025 extended waivers of interstate transmission system charges for electricity drawn from renewable energy sources for use in BESS, subject to minimum renewable energy sourcing conditions and project commissioning timelines up to June 2028. At the state level, policy interventions have gathered momentum, with several states introducing storage-specific targets, incentives and procurement frameworks.

In parallel, successive MoP orders issued between November 2021 and June 2025 extended waivers of interstate transmission system charges for electricity drawn from renewable energy sources for use in BESS, subject to minimum renewable energy sourcing conditions and project commissioning timelines up to June 2028. At the state level, policy interventions have gathered momentum, with several states introducing storage-specific targets, incentives and procurement frameworks.

According to state renewable energy policies and regulations, Assam has notified rules for energy storage procurement, Andhra Pradesh has set long-term storage targets covering both battery and pumped storage, Rajasthan has specified storage obligations linked to captive generation, Tamil Nadu has identified energy storage as a key enabler for meeting solar targets and states such as Telangana, Bihar, Odisha, Madhya Pradesh, Maharashtra and Uttar Pradesh have incorporated energy storage into their renewable, hybrid and incentive frameworks. Collectively, these measures reflect growing alignment between central financial support mechanisms and state-level policy signals to accelerate the commercial deployment of BESS.

Tariff trends

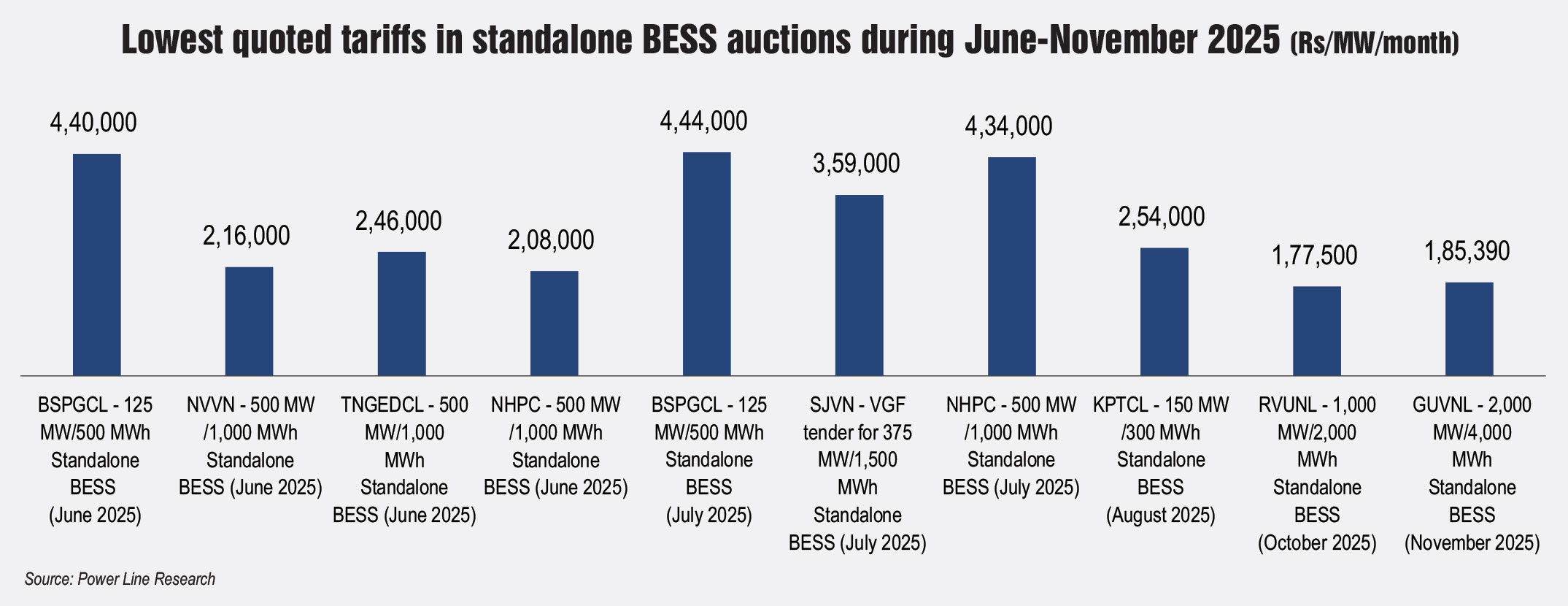

Based on the 2025 auction results presented, India’s standalone battery energy storage market shows a clear downward trajectory in tariff discovery during the year in addition to a notable increase in the number of tendering agencies. Early auctions in June-July 2025 largely discovered tariffs of Rs Rs 216,000-Rs 444,000 per MW per month, with relatively smaller tender sizes of 125-500 MW.

As the year progressed, a combination of larger tender sizes and improved bidder confidence translated into significantly lower tariffs. The August 2025 KPTCL auction for 150 MW/300 MWh saw tariffs decline to around Rs 254,000 per MW per month, while the October and November 2025 auctions conducted by Rajasthan Rajya Vidyut Utpadan Nigam Limited and GUVNL marked a further step change as tariffs clustered in the range of Rs 177,500–Rs 185,390 per MW per month despite much larger procurement volumes of 1,000 MW/2,000 MWh and 2,000 MW/4,000 MWh respectively. This inverse relationship between project size and discovered tariffs reflects the growing impact of economies of scale and lower per-unit financing costs.

Variations across nodal agencies and states also highlight the influence of procurement design and risk allocation on tariff outcomes. Tenders backed by clearer payment security mechanisms, central or financially stronger state utilities, and alignment with VGF frameworks appear to have attracted more aggressive bidding. Overall, the 2025 auction trajectory suggests that India’s standalone BESS market has moved decisively from pilot-scale experimentation towards utility-scale deployment.

The key factors driving this momentum include the VGF framework, which has reduced upfront cost barriers, accelerated state-led procurement and led to the emergence of standardised bidding structures. In addition, policy emphasis on critical minerals and recycling is expected to support longer-term cost stability and supply chain resilience for battery systems.

Key challenges and outlook

Key challenges and outlook

Despite the rapid scale-up of battery energy storage deployment, several structural and regulatory challenges remain. A key concern is the absence of a clearly defined framework for the disposal and recycling of batteries after the expiry of power purchase agreements with ambiguity around the ownership of residual assets and responsibility for end-of-life management. At present, there is no storage-specific treatment under environmental or e-waste regulations for large-scale grid batteries, which creates uncertainty around compliance and cost recovery. High disposal and recycling costs, which are not yet reflected in prevailing tariffs or project structures, further compound this challenge, alongside the limited availability of certified recycling facilities for lithium-ion and advanced battery

chemistries in India.

In addition, continued efforts are required to reduce technology costs, develop standardised safety and reliability guidelines, and strengthen domestic supply chains to reduce dependence on imported raw materials. Looking ahead, greater clarity on end-of-life obligations, sustained policy support for research and development, progress on recycling and critical mineral recovery, and increased awareness among distribution companies of the system-level benefits of storage will be critical to ensuring that BESS transitions from policy-led deployment to a reliable and scalable pillar of India’s power system.