Hydropower remains a cornerstone of India’s renewable energy mix, offering a unique combination of clean generation, grid stability and long-duration storage. Following a period of slowdown, the sector is regaining momentum, marked by rapid capacity additions, renewed policy focus and a growing emphasis on pumped storage projects (PSPs), restoring its strategic importance in India’s energy transition. In addition, the government has set ambitious goals to increase the contribution of hydropower within the overall energy mix, supported by policy frameworks, financial incentives and measures to improve project viability. These initiatives have revived interest among both domestic and international investors, creating momentum for the development of new hydropower projects across the country.

Segment size and growth

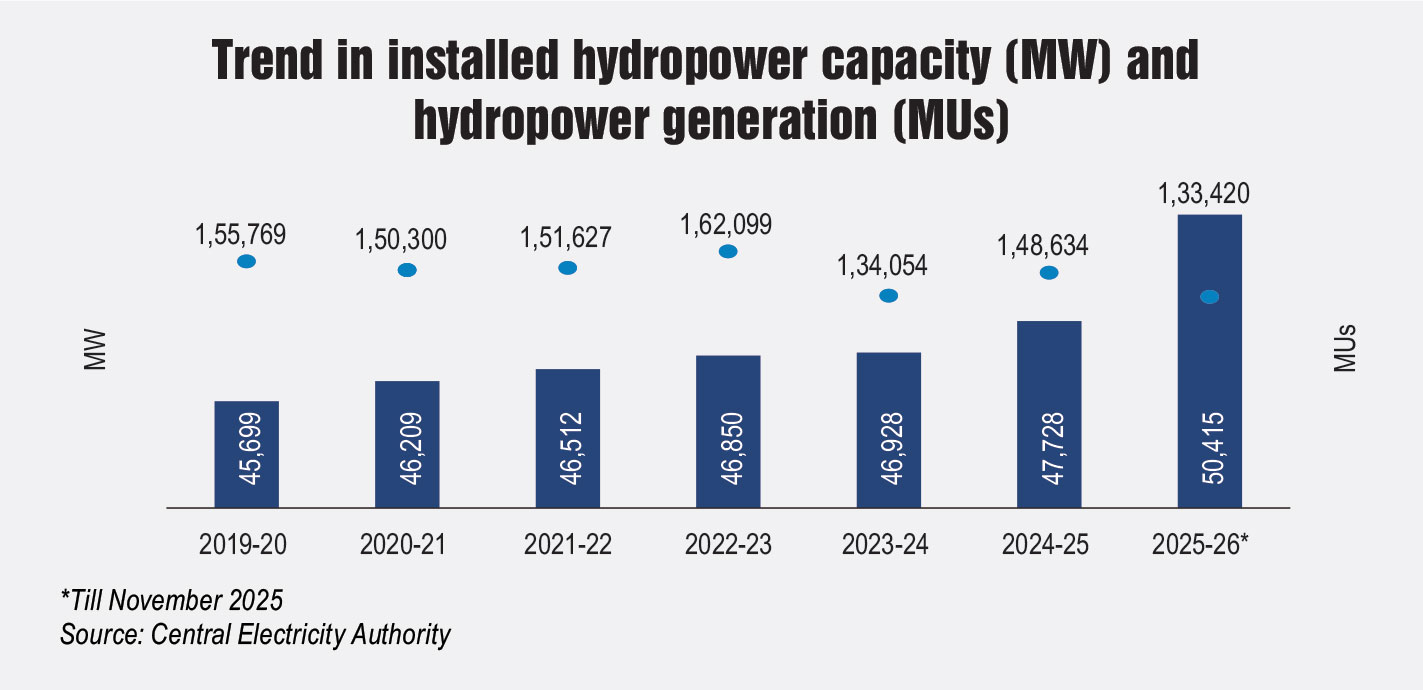

As of November 2025, the country’s installed hydropower capacity stood at 50,414.66 MW for large hydro and 5,158.61 MW for small hydro. During 2024-25, 799.99 MW of hydropower capacity (large hydro) was added, a sharp increase from the 60 MW added in 2023-24. Key projects commissioned in 2024-25 were NHPC Limited’s Parbati II hydroelectric project (HEP) Units 1, 2 and 3 (3×200 MW); Beas Valley Power Corporation Limited’s Uhl III HEP Units 1, 2 and 3 (3×33.33 MW); the Kerala State Electricity Board’s (KSEB) Pallivasal Extension HEP Units 1 and 2 (2×30 MW); and KSEB’s Thottiyar HEP Units 1 (10 MW) and 2 (30 MW).

During 2025-26, a total of 2,620 MW of large-hydro power capacity has been added as of November 2025. This includes Greenko Energies’ Pinnapuram HPS Unit 5 (240 MW); NHPC’s Parbati II HEP Unit 4 (200 MW); THDC’s Tehri PSP Units 1 and 2 (2×250 MW); JSW Energy’s Kutehr HEP Units 1, 2 and 3 (3×80 MW); Greenko’s Pinnapuram HEP Units 1-5 (5×240 MW); and Greenko’s Pinnapuram Units 7 and 8 (2×120).

Large-hydro generation during AprilNovember 2025 reached 133.42 billion units (BUs), reflecting a 13.3 per cent increase over the same period in the previous year. Meanwhile, small-hydro generation rose by 6.59 per cent to 9.55 BUs. During 2024-25, hydropower (large and small) accounted for 40 per cent of total renewable energy generation and 8.76 per cent of overall power generation.

Market drivers

The government’s ambitious target of achieving 500 GW of renewable energy capacity by 2030 is expected to strengthen the role of hydropower, which currently accounts for around 11 per cent of the country’s total installed capacity. With its ability to provide stable and despatchable power, hydropower is well positioned to support the country’s growing energy needs. The government’s continued focus on renewable energy expansion has encouraged private and institutional investors to consider hydropower as a viable long-term investment option. Its long asset life, predictable generation profile and potential for stable returns enhance its attractiveness. Public–private partnerships are expected to play an increasingly important role in financing new projects.

Government policy support remains a key enabler for the hydropower market. A series of initiatives, including financial incentives, viability gap funding and streamlined regulatory processes, have been introduced to promote renewable energy and attract private sector participation.

Technological advancements are further transforming the hydropower landscape. Innovations in turbine design, automation, digital monitoring and grid integration are improving efficiency, reliability and operational performance. The adoption of smart grid and digital technologies is enhancing forecasting, scheduling and energy management.

With growing concerns around climate change and emissions, hydropower is being viewed as a clean and renewable alternative to fossil fuels. India’s commitment to emission reduction and its broader energy transition goals support the expansion of hydropower projects.

Recent developments

Recent developments

In January 2026, the Adani Group commenced construction of the 570 MW Wangchhu HEP in Bhutan in partnership with the Druk Green Power Corporation (DGPC). Under the project structure, DGPC will hold a 51 per cent equity stake, while the Adani Group will own the remaining 49 per cent. The project entails an estimated investment of around Rs 60 billion and is targeted for completion within five years. Earlier, in May 2025, the Adani Group had signed an MoU with DGPC to jointly develop 5,000 MW of hydropower projects in Bhutan. This strategic collaboration builds on the existing partnership for the Wangchhu hydropower project and envisages the development of additional hydropower and pumped storage projects, which will be identified, planned and implemented in phases.

In December 2025, Patel Engineering Limited signed an MoU with the Arunachal Pradesh government for the restoration and development of the 144 MW Gongri hydropower project. Situated near Dirang town on the Gongri river, the project was earlier terminated but has now been revived under the Arunachal Pradesh Restoration of Terminated Large Hydropower Policy under Special Circumstances, 2025. The total project cost is estimated at Rs 17 billion, with construction expected to be completed over a period of around four years.

In October 2025, the CEA issued a Rs 6.4 trillion transmission master plan to evacuate over 76 GW of hydropower capacity from the Brahmaputra basin by 2047. As per the CEA, the plan proposes the development of 208 large hydro projects across 12 sub-basins in the north-eastern states, with 64.9 GW of hydropower and 11.1 GW of pumped storage capacity. The master plan also emphasises the development of high-capacity transmission corridors, pooling stations and substations to connect projects in remote hilly terrains to the national grid, along with redundant corridors to enhance resilience against natural disasters. The two-phase plan involves an investment of Rs 1.91 trillion until 2035 and Rs 4.52 trillion until 2047.

In September 2025, the central government inaugurated infrastructure projects worth Rs 51.25 billion in Arunachal Pradesh, which include two hydropower projects the 186 MW Tato-I and 240 MW Heo to be developed jointly by the Arunachal Pradesh government and North Eastern Electric Power Corporation Limited on the Yarjep river in Shi Yomi district. The Tato I project is expected to generate 802 MUs of electricity annually, while the Heo project is projected to generate 1,000 MUs annually.

In August 2025, the Ministry of Power (MoP) issued a notification revising the concurrence requirement for hydro generating stations under the Electricity Act, 2003. As per the notification, schemes involving an estimated capex exceeding Rs 30 billion will require the CEA’s approval. Off-stream closed-loop pumped storage schemes are exempted from this requirement, regardless of their capex.

In May 2025, the Ministry of New and Renewable Energy issued revised guidelines for small-hydro power schemes. The revised guidelines apply to all small-hydro projects sanctioned under previous schemes and aim to address ongoing sectoral challenges faced by stakeholders. For the release of the remaining central financial assistance (CFA), projects must now achieve at least 80 per cent of the projected generation for any one corresponding month as per the detailed project report (DPR), otherwise, the second CFA instalment will be reduced proportionally. If a project achieves 73 per cent of the projected generation for three consecutive months or cumulative annual generation for one year as envisaged in the DPR, the second CFA instalment will be calculated on a pro-rata basis, with the methodology being provided in the policy document.

Challenges and outlook

Despite its significant growth potential, the hydropower segment continues to face multiple challenges. These include disputes over water rights, environmental and ecological concerns, a limited pool of financially robust civil contractors, complexities related to resettlement and rehabilitation, and unforeseen geological conditions. Such issues frequently result in project delays and cost overruns, highlighting the need for comprehensive and coordinated strategies to address these constraints and unlock India’s full hydroelectric potential. According to the CEA, around 1,236 MW of hydropower capacity is currently stalled.

As per the CEA’s National Electricity Plan 2023, the installed hydropower capacity is projected to reach 88 GW by 2031-32, including 26 GW from PSPs, requiring an estimated investment of Rs 3.2 trillion. As of December 2025, 24,593.5 MW of large-hydro power projects (including PSPs) are under construction, with 10,682 MW in the central sector, 6,241.5 MW in the state sector and 7,670 MW in the private sector. About 860 MW of new capacity is expected to be commissioned in 2025-26.

Going forward, the hydropower market is increasingly being shaped by trends centred on digitalisation, sustainability and strategic collaboration. Innovation and deeper integration of advanced technologies are becoming critical to project development and operations. Strategic partnerships are expected to play a key role in defining the sector’s future, helping companies strengthen capabilities, mitigate risks and expand their market footprint.

Overall, India’s hydropower sector stands at a critical juncture, supported by rising demand, strong policy backing and the expanding role of pumped storage in balancing variable renewable energy. With large-scale capacity under construction, growing private sector participation and increasing adoption of digital and sustainable technologies, hydropower is well positioned to play a central role in ensuring reliable, round-the-clock clean power and strengthening India’s energy security in the coming decades.