Indonesia, the world’s fourth-largest producer of coal and Southeast Asia’s largest gas supplier, has a strong reliance on fossil fuels. However, the country’s population have become increasingly supportive of climate goals, and the challenge for Indonesian policymakers lies in balancing the need for economic development, energy security, increased access to energy and affordability with the growing demand for a shift towards renewable energy sources (RES). The country’s reliance on fossil fuels and its abundant coal resources could prolong the use of existing infrastructure, complicating the energy transition. To address this, Indonesia is considering a multi-faceted approach that includes a clear and consistent regulatory framework for RES development, a re-evaluation of its fossil-heavy strategy and the creation of a transparent project procurement process. Its final draft Rencana Umum Ketenagalistrikan Nasional (RUKN) or the National Electricity General Plan, released in November 2023, provides a pathway for achieving net zero emissions in energy by 2060 (or sooner).

To aid the country in achieving its energy goals, in November 2023, Indonesia’s Just Energy Transition Partnership (JETP) unveiled the Comprehensive Investment and Policy Plan (CIPP) 2023, a roadmap for the country’s energy transition, with an initial commitment of $20 billion. This was following the launch of the JETP by the Indonesian government and the International Partners Group (IPG) on the sidelines of the G20 Summit in Bali, Indonesia, in November 2022. The IPG comprises the governments of Japan and the US, who are co-leaders of the partnership, and Canada, Denmark, the European Union, Germany, France, Norway, Italy, and the UK and Northern Ireland.

The CIPP, prepared by the JETP Secretariat team, outlines various scenarios with RES and carbon dioxide reduction targets, recommends policy reforms and establishes a transition framework. It sets out five JETP investment focus areas (IFA) up to 2030, the first of which is transmission lines and grid deployment (IFA 1), which involves 8,000-14,000 circuit km (ckt km) at an investment of $19.7 billion. IFA 2 is early coal-fired power plant retirement, as well as managed phase-out coal flexibility retrofits and early retirements, with an investment of $2.4 billion; IFA 3 is dispatchable RES acceleration involving a build-out of 16.1 GW at $49.2 billion; IFA 4 is variable renewable energy (VRE) acceleration involving a build-out of 40.4 GW at $25.7 billion; and IFA 5 is RES supply chain enhancement.

By 2030, Indonesia’s annual average power sector investments are expected to exceed $15 billion, rising to over $25 billion during 2031-40 and nearly $30 billion over the 2041-50 period. Hydropower will account for the largest portion, with cumulative investments of over $100 billion by 2040. Geothermal and solar photovoltaic (PV) investments will each total over $55 billion by 2040. Investments in electricity networks, including $42 billion in transmission and $9 billion in distribution, will total over $50 billion by 2040.

Power system overview

Power system overview

Indonesia has been working on fostering competition and reducing the monopoly of the state-owned utility, PT Perusahaan Listrik Negara (PLN), since the opening up of its electricity market in 2009. This move enabled independent power producers (IPPs) to generate and distribute electricity to consumers. However, PLN and its subsidiaries still control the majority of the country’s installed capacity, as they hold the right of first refusal for electricity purchase and manage the transmission sector.

Approximately 65 per cent of Indonesia’s installed electricity capacity of 71 GW in September 2023 was generated by PLN. Of this, 59 per cent was from thermal sources, 5 per cent from hydro and 1 per cent from RES. The remaining 35 per cent was contributed by IPPs and rented diesel.

The Indonesian power system is marked by an excess of power capacity in densely populated areas and shortages in remote regions. The lack of interconnections among the major islands hinders the utilisation of surplus power. Four main power systems account for 95 per cent of the country’s electricity demand: Java-Madura-Bali (JMB) system (70 per cent), Sumatra (17 per cent), Kalimantan (5 per cent) and Sulawesi (3 per cent). Regions such as Maluku, Papua and Nusa Tenggara have significant RES potential but low electricity demand due to underdeveloped generation and grid infrastructure.

As of September 2023, Indonesia’s transmission network comprised 63,433 ckt km of alternating current (AC) lines at the 150 kV to 500 kV voltage levels. The transformer capacity stood at 164 GVA as of September 2023. The country’s transmission grid is mainly made up of 150 kV lines, with a limited number of 275 kV and 500 kV lines, concentrated in Java-Bali and Sumatra.

Future plans

Future plans

Generation

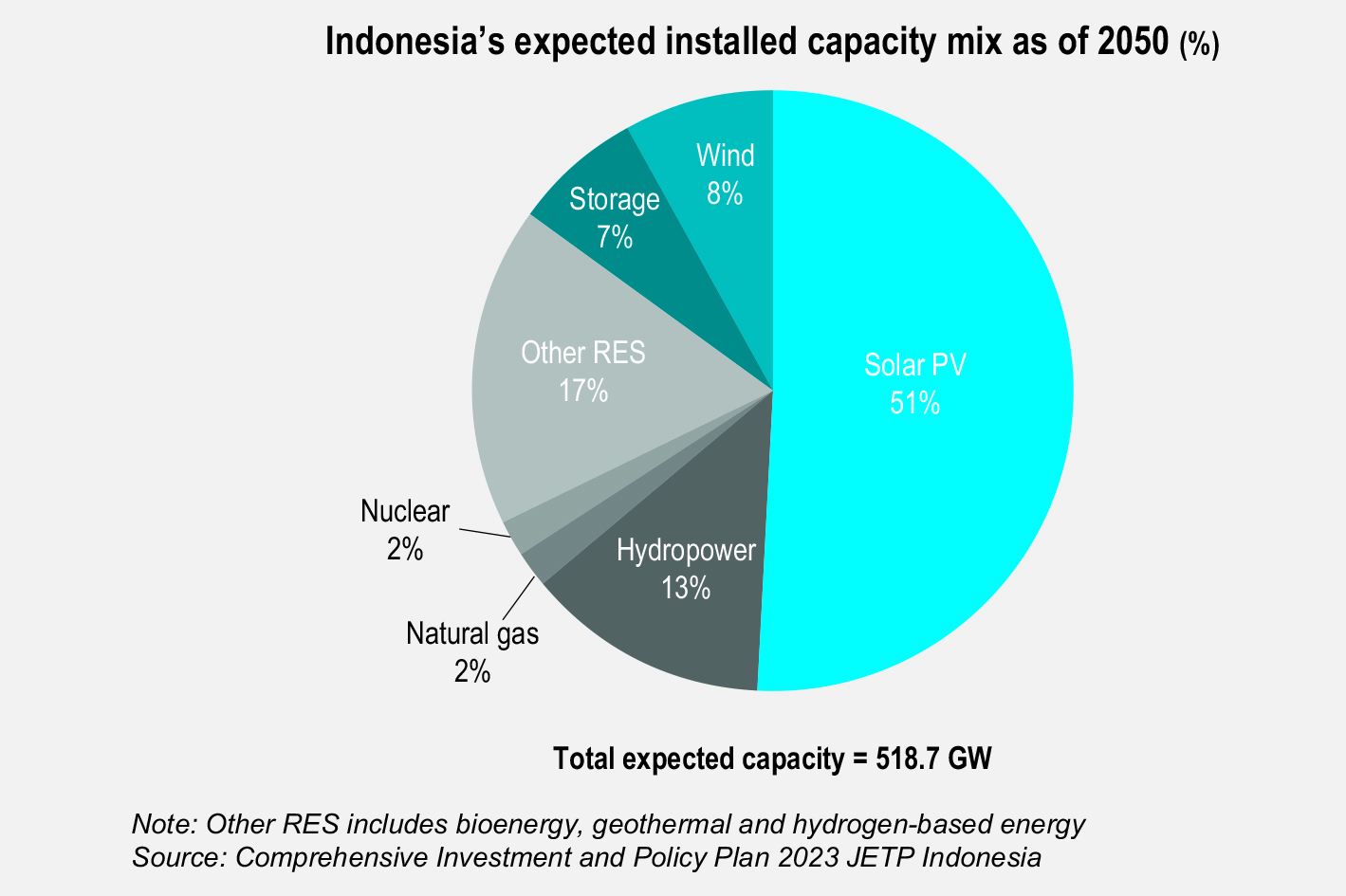

To deliver Indonesia’s long-term emissions reduction goals and economic growth targets, the country is working towards decarbonising its fossil-fuel-dependent power sector. The JETP scenario under the CIPP 2023 considers only grid-connected power sector emissions and targets, with a strong role for new transmission interconnections, policy reforms to accelerate RES deployment and measures to reduce the role of coal in the power mix. The targets are quite ambitious compared to the main scenario of the final draft RUKN. By 2030, the JETP scenario aims for an RES share of 44 per cent compared to 25 per cent in the final draft RUKN scenario. In addition, several captive coal plants (off-grid) planned for industries including nickel, cobalt and aluminium smelters, will have to be addressed to fully decarbonise the economy. Nevertheless, by 2050, Indonesia’s generation mix is set to undergo a significant transformation, with a strong RES focus. Currently, RES development is primarily centred on dispatchable RES sources such as hydropower, geothermal and bioenergy. By 2050, the country aims to rely heavily on VRE sources such as solar PV and wind for electricity generation.

Transmission

Indonesia’s power grid needs significant upgrades to interconnect island systems and integrate RES. The CIPP’s IFA 1 has set a target of 8,000-14,000 ckt km by 2030. However, it acknowledges PLN’s plan of adding 6,000 km of lines by 2030 and 15,000 km by 2040. To achieve these goals, Indonesia needs to sustain an annual network investment of around $3 billion by 2030, with over 80 per cent of it required for transmission. For transmission, around $42 billion of cumulative capital investment is projected by 2040 to support island-level systems and interconnections between JMB and other islands, including Sumatra, Kalimantan and Nusa Tenggara, to help bring RES generation to the JMB system. In the JETP scenario, significant inter-island high voltage direct current (HVDC) interconnection will also be required in 2035-50 to transmit clean power from Kalimantan to Java.

In the medium term, a stronger backbone has to be built to ensure bulk transmission capacity and improved power quality. Apart from the JMB and Sumatra systems, the islands currently have relatively dispersed and separated power systems. The JMB system already has two 500 kV corridors in the north and south forming the basic foundation for RES integration and does not require any major transmission investments in the immediate term. Investments in other islands need to be stepped up to evacuate RES to meet strong demand beyond 2030. Particularly, the interregional transmission lines connecting subsystems in Sumatra must be reinforced first, which is included in the JETP priority project list.

Conclusion

Indonesia’s JETP has outlined the CIPP for the country’s energy transition and aims to produce an ambitious pathway for the power sector. It aims to modernise the power supply chain and optimise grid operations with investments in electricity networks vital for interconnecting island systems and RES integration. The JETP agreement has secured financing, but much greater funding from diverse sources of capital is required to realise the outlook. The success of the JETP’s efforts will be crucial for Indonesia to achieve its long-term emissions reduction goals and economic growth.