The Ministry of Power (MoP) recently released the 14th Integrated Rating and Ranking Report, which presents a comprehensive assessment of the operational and financial performance of 65 power distribution companies (discoms) for FY 2024-25. The latest ratings highlight a mixed performance across utilities. As per the report, 31 discoms have been graded in the A+ or A category, 23 utilities fall under the B or B- category, while 11 utilities have been assigned C or C- grades. Notably, 12 utilities achieved scores of over 90 out of 100, reflecting strong improvements in both operational efficiency and financial discipline.

Key highlights from the latest ratings exercise and the performance of discoms…

Ratings assigned

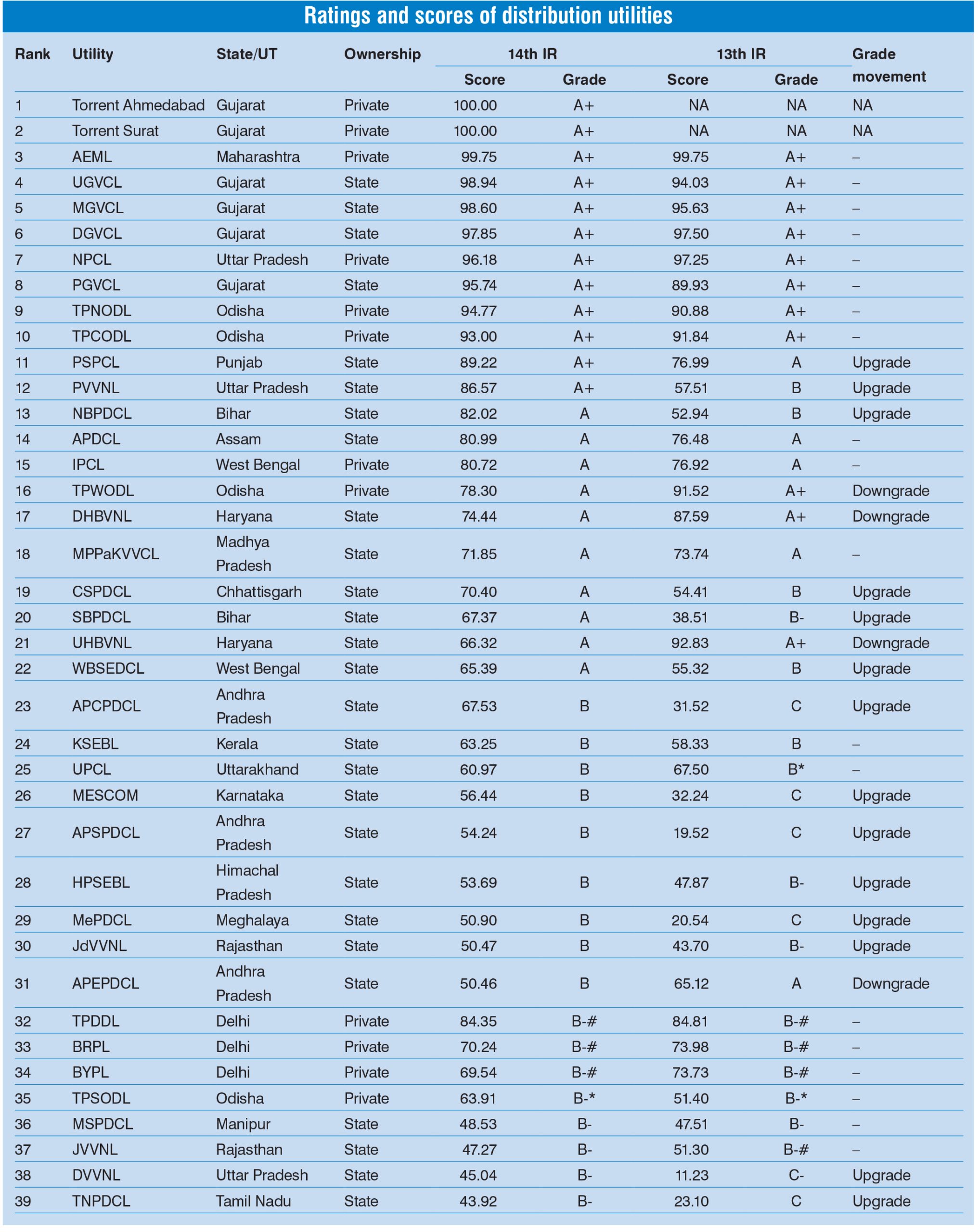

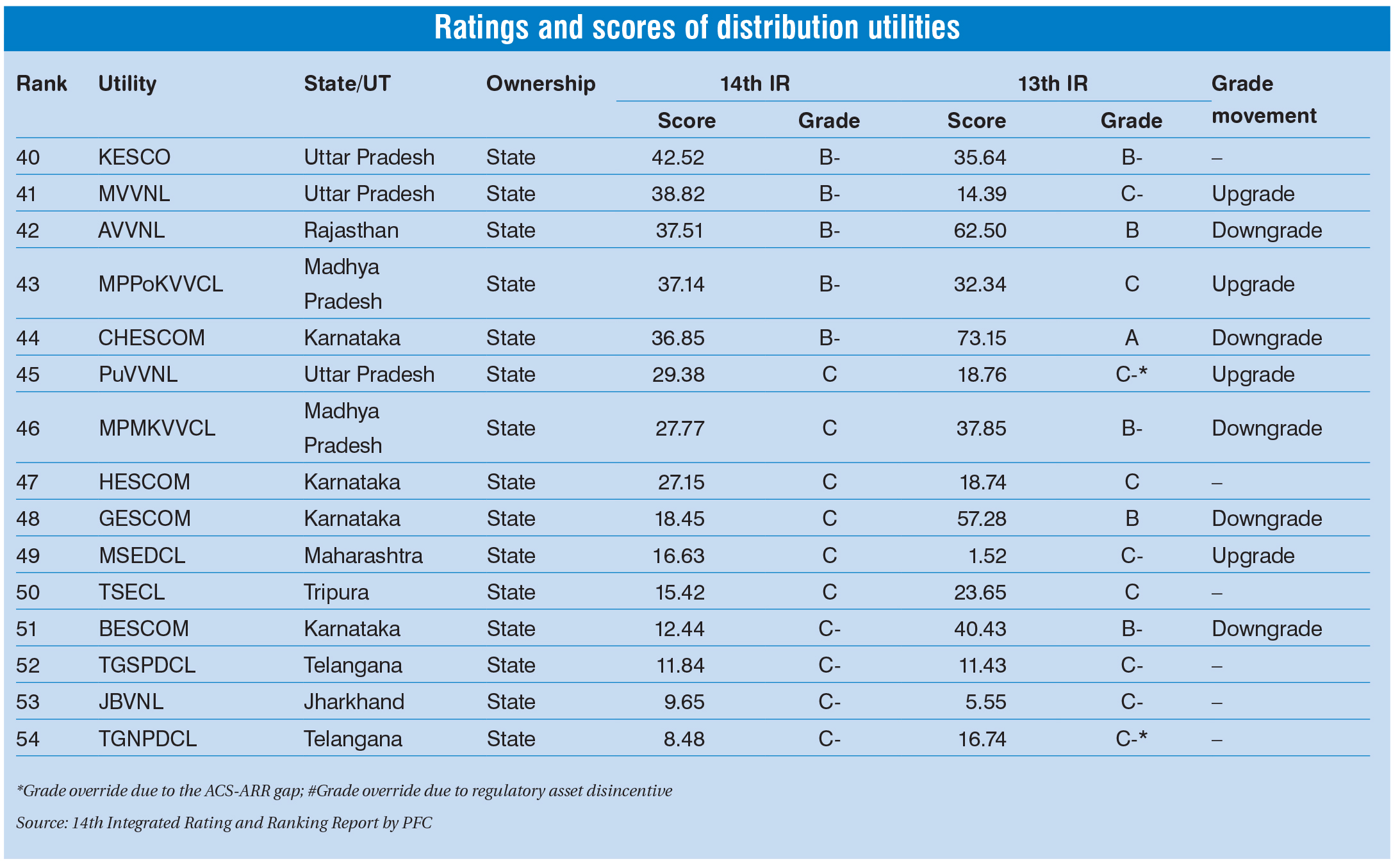

Of the 72 power distribution utilities operating across the country, 65 have been rated under the 14th Integrated Rating, up from 63 utilities covered in the 13th edition. Out of these 65 discoms, 22 witnessed improved scores. The top 10 performing discoms were Torrent Power Ahmedabad, Torrent Power Surat, Adani Electricity Mumbai Limited (AEML), Uttar Gujarat Vij Company Limited, Madhya Gujarat Vij Company Limited, Paschim Gujarat Vij Company Limited (PGVCL), Dakshin Gujarat Vij Company Limited, Noida Power Company Limited, TP Northern Odisha Distribution Limited (TPNODL) and TP Central Odisha Distribution Limited (TPCODL).

Of the 65 discoms, a total of 31 utilities earned a rating of A+ or A, 23 utilities received a B or B- grade, while 11 recorded C or C- in the 14th ratings report (2024-25).

Out of the 42 state government power utilities rated, the ones belonging to Gujarat, Punjab, Uttar Pradesh, Bihar, Assam, Haryana, Madhya Pradesh, Chhattisgarh and West Bengal earned a rating of either A+ or A. All 12 private power discoms received a performance rating of either A+, A, or B-.

The 14th edition also gave integrated performance ratings to the power departments (PDs) of 11 states and union territories. Among these, the Thrissur Corporation Electricity Department of Kerala, the Brihanmumbai Electric Supply & Transport Undertaking (BEST) of Maharashtra, and the New Delhi Municipal Council (NDMC) of Delhi emerged on top with an A+ rating, followed by the PDs of Goa at fourth and Sikkim at fifth positions, with an A rating.

Parameter-wise performance

Parameter-wise performance

AT&C losses: Aggregate technical and commercial (AT&C) losses declined from 15.97 per cent in FY 2023-24 to 15.04 per cent in FY 2024-25. During FY25, 38 utilities – comprising 33 discoms and five PDs – reported AT&C losses below 15 per cent. Further, 22 utilities registered an improvement of more than 2 percentage points in AT&C losses compared to the previous year.

Billing efficiency: Billing efficiency improved marginally from 86.99 per cent in FY 2023-24 to 87.59 per cent in FY 2024-25. As many as 21 utilities achieved billing efficiency at or above the upper scoring threshold – 92 per cent for discoms and 90 per cent for PDs. Overall, billing efficiency improved across 46 utilities, with 13 utilities recording a significant increase of more than two percentage points. These include PGVCL; Odisha utilities – TPNODL, TPCODL and TPSODL; South Bihar Power Distribution Company Limited (SBPDCL); Rajasthan utilities – Jodhpur Vidyut Vitran Nigam Limited (JdVVNL), Jaipur Vidyut Vitran Nigam Limited (JVVNL) and Ajmer Vidyut Vitran Nigam Limited (AVVNL); Dakshinanchal Vidyut Vitran Nigam Limited; Hubli Electricity Supply Company Limited (HESCOM); NDMC; Mizoram PD; and the Andaman & Nicobar PD. However, among the 65 rated utilities, billing efficiency for 10 utilities remained below the lower threshold for scoring, which is 82 per cent for discoms and 75 per cent for PDs.

Collection efficiency: Collection efficiency across power distribution utilities improved from 96.6 per cent in FY 2023-24 to 97 per cent in FY 2024-25, indicating better revenue realisation across the sector. In FY25, 17 utilities achieved 100 per cent collection efficiency, while 29 utilities recorded an improvement over the previous year. Notably, 12 utilities registered a significant increase of more than two percentage points, including utilities in Andhra Pradesh – Andhra Pradesh Central Power Distribution Corporation Limited (APCPDCL), Andhra Pradesh Southern Power Distribution Company Limited (APSPDCL) and APEPDCL; Karnataka – Mangalore Electricity Supply Company Limited (MESCOM) and HESCOM; Rajasthan – JdVVNL, JVVNL and AVVNL; as well as Maharashtra State Electricity Distribution Company Limited; SBPDCL; Jharkhand Bijli Vitran Nigam Limited (JBVNL); and Tripura State Electricity Corporation Limited (TSECL).

ACS-ARR gap: The ACS-ARR gap (cash adjusted) improved by Re 0.25 per kWh, narrowing from Re 0.32 per kWh in FY24 to Re 0.07 per kWh in FY25, indicating a notable strengthening of the sector’s overall cost recovery position. Significant improvements of over Re 0.50 per kWh from FY24 to FY25 were recorded by several utilities, including Torrent Power Ahmedabad and Surat, Andhra Pradesh discoms (APCPDCL and APSPDCL), Delhi discoms (BSES Rajdhani Power Limited and BSES Yamuna Power Limited), JBVNL, MESCOM, Kerala State Electricity Board Limited, Ladakh PD, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited, AEML, BEST, Meghalaya Power Distribution Corporation Limited, TSECL, Mizoram PD, Puducherry PD and Sikkim PD. These gains reflect enhanced operational efficiency, improved revenue realisation, and stronger financial performance. Conversely, a deterioration in the ACS-ARR gap was observed in NDMC, Bengaluru Electricity Supply Company Limited, Chamundeshwari Electricity Supply Corporation Limited, Manipur State Power Distribution Company Limited, AVVNL, Kanpur Electricity Supply Company Limited, Madhyanchal Vidyut Vitran Nigam Limited and Purvanchal Vidyut Vitran Nigam Limited, indicating widening financial gaps that could pose challenges to the long-term sustainability of their operations.

PAT and subsidy realised: The power distribution sector achieved a positive profit after tax (PAT) on an accrual basis at the all-India level for the first time, posting a combined PAT of Rs 27.01 billion in FY25, compared to a loss of Rs 270.22 billion in FY24. The ACS-ARR gap on a tariff-subsidy-received basis narrowed sharply to Re 0.06 per kWh in FY25 from Re 0.20 per kWh in FY24, underscoring improved cost recovery. Subsidy realisation rose to 98.9 per cent in FY25 from 97.45 per cent in FY24, with full subsidy dues for the last three years cleared in multiple states.

PAT and subsidy realised: The power distribution sector achieved a positive profit after tax (PAT) on an accrual basis at the all-India level for the first time, posting a combined PAT of Rs 27.01 billion in FY25, compared to a loss of Rs 270.22 billion in FY24. The ACS-ARR gap on a tariff-subsidy-received basis narrowed sharply to Re 0.06 per kWh in FY25 from Re 0.20 per kWh in FY24, underscoring improved cost recovery. Subsidy realisation rose to 98.9 per cent in FY25 from 97.45 per cent in FY24, with full subsidy dues for the last three years cleared in multiple states.

Days receivable and payable: Days receivable remained broadly stable at 112 days, with 26 discoms achieving receivables of ≤60 days, while 19 discoms continued to exceed 120 days. Days payable to gencos and transcos improved significantly to 113 days from 132 days, with 33 discoms showing better payment discipline and 20 discoms achieving payables of ≤60 days.

On the regulatory side, FY26 tariff orders were issued on time in 23 states/UTs, FY24 true-up orders were issued for 52 of 65 utilities, and 30 regulators implemented automatic fuel cost pass-through, supporting timely recovery of power purchase costs.

Conclusion

The 14th Integrated Rating and Ranking Report indicates an improvement in the power distribution sector performance, marked by improving operational efficiencies, stronger financial discipline, and positive PAT at the all-India level. While leading utilities continue to set benchmarks through sustained reforms, digitalisation and prudent cost recovery, the performance divergence across discoms highlights the need for targeted interventions in weaker utilities. Going forward, timely regulatory actions, continued subsidy discipline, and accelerated adoption of best practices will be critical to sustaining gains and ensuring the long-term financial viability of India’s power distribution segment.

Akanksha Chandrakar