Coal is the primary source of power generation in the country, accounting for around 60 per cent of the total installed base and 78 per cent of the total power generation. However, over the past few years, the segment has been witnessing low power offtake from discoms. In order to address this issue, several efforts are being made. On the policy level, the Ujwal Discom Assurance Yojana (UDAY) is expected to help restore the financial health of the state discoms and allow them to procure power.

More recently, two important policy announcements have been made – amendments to the Mega Power Policy, 2009 and release of the methodology for flexibility in the use of coal by independent power producers (IPPs). While the former is expected to provide relief to as much as 27 GW of capacity, the latter is expected to lower the cost of coal-based power generation by bringing down coal transport costs. Besides, developers are increasingly focusing on renovation and modernisation (R&M), and life extension of existing power plants in order to improve the generation efficiency and increase the environment friendliness of coal-based power.

Power Line looks at the key trends in the coal-based power segment, the recent developments and the future outlook…

Sector size and growth

As of February 2017, the total installed coal-based capacity in the country stood at 189 GW. Of this, the private sector holds the highest share (38.7 per cent), followed by the state (33.8 per cent) and central (27.5 per cent) sectors.

Since February 2016), the country’s coal-based installed capacity has grown by 5.3 per cent.

In the first 11 months of 2016-17 (April 2016-February 2017), 3,875 MW of coal-based capacity was added, which accounted for 22.31 per cent of the total capacity addition during the period. Of this, the private sector contributed over 90 per cent. However, the capacity addition during the period was 65 per cent lower than that in the corresponding period of the previous year.

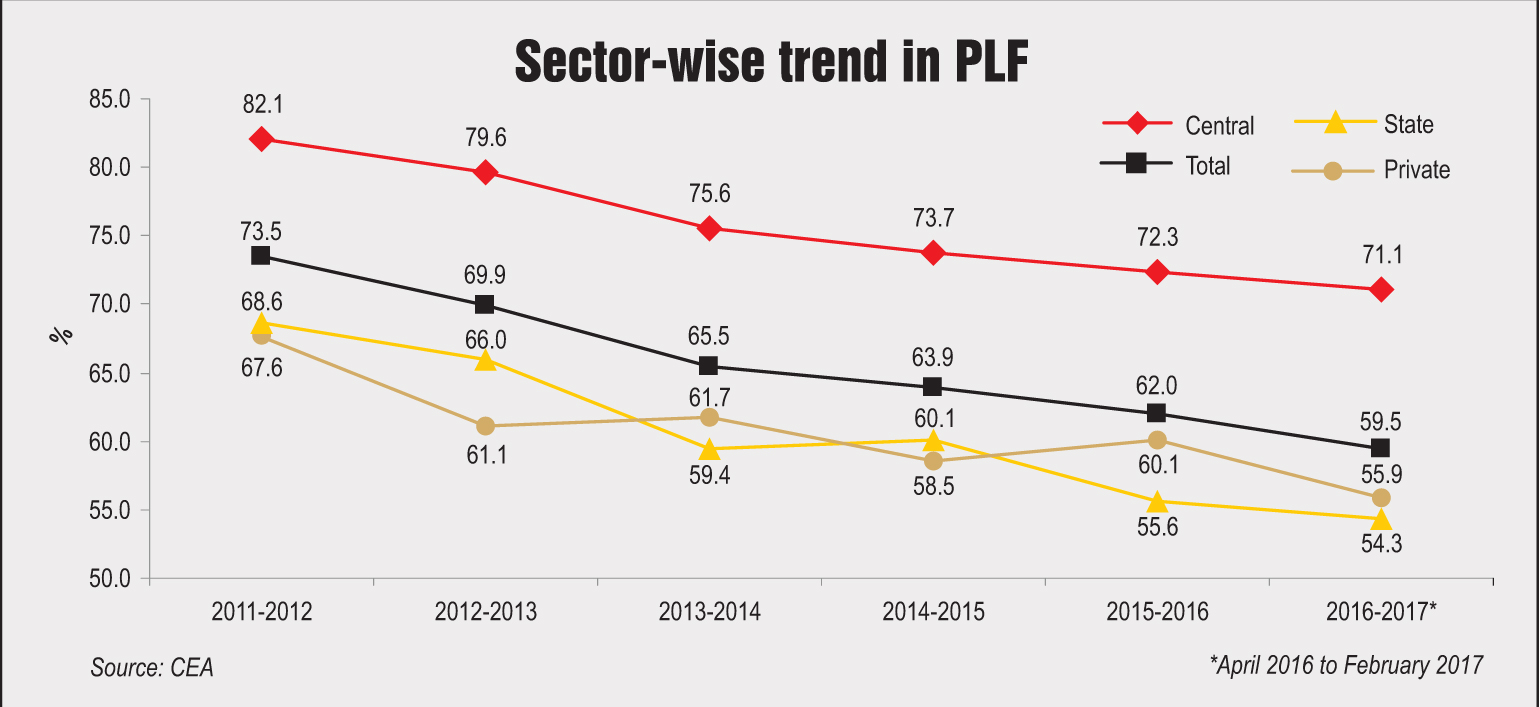

Generation performance

In the first 11 months of 2016-17 (April 2016 to February 2017), coal-based power generation in the country was recorded at 827.1 BUs, marking an increase of 5.5 per cent over the corresponding period of the previous year. Ownership-wise, the private sector accounted for the majority share (36.5 per cent), followed by the central sector (32.5 per cent) and the state sector (31 per cent).

Meanwhile, low plant load factors (PLFs) continue to be a cause for concern. During the first 11 months of 2016-17 (April 2016 to February 2017), the PLF of coal-based plants stood at 59.45 per cent, as against 61.87 per cent over the corresponding period of the previous year. Ownership-wise, the PLF of central sector plants at 71.1 per cent was significantly higher than that of the private sector (55.9 per cent) and state sector plants (54.3 per cent).

R&M, life extension and replacement of old plants

In the Twelfth Plan period (2012-17) (up to December 2016), R&M works have been completed at 11 power plant units aggregating 2,060 MW of capacity. Meanwhile, life extension works have been completed in 21 power units aggregating 2,641 MW.

Moreover, around 12,934 MW of capacity is currently undergoing R&M. This includes NTPC’s 38 thermal power units aggregating 12,304 MW, and the state sector’s five power plant units aggregating 630 MW. Further, three units aggregating 520 MW in the state sector are under life extension works.

Meanwhile, 5,228 MW of thermal power units are being retired and replaced with new supercritical units totalling 10,180 MW of capacity. In the state sector, 13 units aggregating 4,098 MW are being replaced with 8,200 MW of capacity, while in the central sector Damodar Valley Corporation’s (DVC) 1,130 MW of thermal power capacity is being replaced with 1,980 MW of supercritical capacity.

Key recent developments

One of the recent positive policy announcements for the coal-based power generation segment is the amendment to the Mega Power Policy, 2009. The amendment provides a five-year extension to 25 large power projects (around 27 GW of coal-based capacity) for signing long-term power purchase agreements (PPAs). As a result, these plants can avail of customs and excise duty benefits on equipment until 2022. Further, the amendment allows accruing mega policy benefits in proportion to the quantum of capacity tied up under a long-term PPA, once the specified threshold capacity gets commissioned. Reportedly, only 11,000 MW of capacity has been commissioned, with the remaining at various stages of implementation. The relaxation in the time frame will help these projects unlock benefits of over Rs 100 billion (ranging from Rs 3 million to Rs 4 million per MW) under the policy.

Another important policy development for coal-based power plants was the issue of the methodology for the use of domestic coal allocated to states by IPPs. The methodology aims to bring down the cost of power generation by reducing coal transportation charges. Broadly, it lays down that the state supplying coal will invite tariff bids from IPPs for the use of domestic coal from its aggregated coal allocation and the IPPs will supply power to the state in lieu of the transfer of such coal. Released in February 2017, this was in continuation of the methodology for flexibility in the utilisation of coal among state and central generating stations released by the Central Electricity Authority (CEA). Another related development was the launch of the Coal Mitra web portal to bring about flexibility in the utilisation of domestic coal by transferring the reserves to more cost-efficient state/centre-owned or private sector generating stations.

For power plants operating on imported coal, an important development was the Central Electricity Regulatory Commission’s computation of compensatory tariffs in accordance with the APTEL’s directions. The order allowed tariff relief to the imported coal-based projects of Adani Power Limited and Coastal Gujarat Power Limited under force majeure following the rise in coal prices due to a change in Indonesian regulations. However, in march 2017, the SC disallowed any relief to both the power generators, resulting in a major setback to both companies and setting a precedent for other coal-based plants.

Another crucial area of concern for thermal power plant developers is compliance with stricter emission and water consumption norms set by the Ministry of Environment, Forest and Climate Change (MoEFCC). The majority of the plants are yet to comply with these norms, notified in December 2015, even though there is less than a year left to meet the deadline of December 2017. Reportedly, the power ministry has recently sought an extension of the deadline from the MoEFCC by two years, and modification of the norms to make them more practicable for power plants of varying vintages and capacities. The technology solutions entail high costs and require additional land. For old plants, this is not a viable option given the remaining life of the power plant.

Future outlook

In terms of capacity addition in the coal-based segment, no new plants have achieved financial closure in the past two to three years. The draft National Electricity Plan, released in December 2016 by the CEA for the period 2017-22, has indicated that no new coal-based capacity addition is required over the next decade as coal-based capacity of 50,025 MW is already under construction. These plants are likely to yield benefits during 2017-22, and will fulfil the capacity requirement for the period 2022-27.

Given the lack of new projects in the pipeline, going forward, the focus is expected to be on improving the operational performance of the existing power plants. Poor offtake demand is in part responsible for low PLFs in the country and the build-up of stressed assets. As per KPMG estimates, nearly 50 GW of the 70 GW of operational coal-based power plants in the private sector are stressed. Further, around 80-90 per cent of under-construction plants in the private sector are stressed. In this regard, the UDAY scheme is expected to bring a turnaround in the discom financial position.

In addition, the coal-based power plant are facing challenges due to the large-scale integration of renewable energy sources. Thus, developers are working out strategies for flexibilisation of their plants to cope with scheduling. Besides, the use of clean coal technologies is expected to improve the case for coal-based power in light of tougher environment norms.

To conclude, although the growth of the coal-based power generation segment has slowed down, introducing conducive policy measures and taking other positive initiatives are likely to revive coal-based power generation in the country.