The past year has seen notable shifts in the operational performance of utilities across the power sector in India. Power demand surged significantly, leading to higher operational efficiency in thermal power plants (TPPs), as reflected in the improved plant load factor (PLF). However, the transmission sector experienced varied outcomes, with some utilities successfully reducing transmission losses and others facing setbacks with rising losses. On a more positive note, distribution companies (discoms) showed remarkable progress, achieving a steady decline in aggregate technical and commercial (AT&C) losses, which declined to 15.37 per cent in 2022-23 compared to 16.23 per cent in 2021-22 and 21.91 per cent in 2020-21.

Power Line presents an overview of the performance of utilities across the power sector during the past year…

Generation

The national PLF of TPPs stood at 69.09 per cent during 2023-24, an increase of 5.14 percentage points from the 63.95 per cent recorded in 2022-23. Of the 34 utilities tracked by Power Line Research during 2023-24, 24 reported an increase in PLF over the previous year. The highest PLF (93.52 per cent) was reported by Sasan Power Limited, which operates the 3,960 MW Sasan ultra mega power project in Madhya Pradesh, followed by Torrent Power Limited with a PLF of 90.95 per cent.

Sector-wise, the central sector recorded the highest PLF during 2023-24. The average PLF of central sector-owned plants stood at 75.09 per cent, higher than the 74.61 per cent recorded in the previous year. In the state sector, PLF was recorded at 64.7 per cent during 2023-24, significantly higher than the 61.73 per cent recorded a year ago. In the private sector, PLF increased from 56.19 per cent in 2022-23 to 67.65 per cent in 2023-24.

Among central utilities, NTPC Limited recorded a PLF of 76.84 per cent during 2023-24, 1.2 percentage points higher than its previous year’s record of 75.64 per cent. NTPC’s best performing plant during 2023-24 was the Korba super thermal power station (STPS) in Chhattisgarh, which recorded a PLF of 89.84 per cent, whereas its lowest PLF of 50.53 per cent was recorded at its Barauni TPS in Bihar. Among other central sector utilities, the Damodar Valley Corporation recorded an increase of 3.38 percentage points in its PLF from 73.43 per cent during 2022-23 to 76.81 per cent during 2023-24, whereas the PLF of NLC India Limited decreased from 68.87 per cent to 61.14 per cent during 2023-24.

At the state level, Chhattisgarh State Power Generation Company Limited (CSPGCL) was the best performing utility with an impressive PLF of 84.45 per cent during 2023-24, well above the average state sector PLF of 64.7 per cent as well as the national average. Singareni Collieries Company Limited was the second-best performing state utility with a PLF of 83.99 per cent, followed by West Bengal Power Development Corporation Limited (WBPDCL) with a PLF of 82.31 per cent and Telangana State Power Generation Corporation Limited (TSGenco) with a PLF of 79.64 per cent during 2023-24. Eight state utilities, SSCL, WBPDCL, Uttar Pradesh Rajya Vidyut Utpadan Nigam Limited, Tenughat Vidyut Nigam Limited, Haryana Power Generation Corporation Limited, Gujarat State Electricity Corporation Limited, Durgapur Projects Limited and Gujarat Mineral Development Corporation Limited recorded a decline in PLF during 2023-24 compared to 2022-23, while the rest reported an increase from the previous year’s level. The highest increase in PLF was reported by CSPGCL and TSGenco. CSPGCL’s PLF increased by 13.27 percentage points from 71.18 per cent during 2022-23. Meanwhile, TSGenco recorded an increase of 7.99 percentage points, from 71.65 per cent during 2022-23 to 79.64 per cent during 2023-24.

In the private sector, PLFs varied widely, ranging from 38.23 per cent to 93.52 per cent. Sasan Power Limited, Torrent Power Limited (Sabarmati TPP), RattanIndia Power Limited, Jindal India Thermal Power Limited (JITPL), Adani Power Limited, CESC Limited, Essar Power Madhya Pradesh Limited, Essar Power Gujarat Limited, Coastal Gujarat Power Limited, Tata Power (Trombay TPS) and JSW Energy Limited witnessed an increase in PLFs during the review period. Meanwhile, Adani Electricity Mumbai Limited (AEML) (Dahanu TPP) registered a decline in PLF from 79.88 per cent in 2022-23 to 73.96 per cent in 2023-24. Five private utilities reported PLFs higher than the national average. These are JITPL, RattanIndia, AEML, Sasan Power Limited and Torrent Power Limited (Sabarmati TPP). The highest year-on-year increase in PLF was reported by Essar Power Madhya Pradesh Limited, which registered a PLF of 63.91 per cent during 2023-24, against 35.99 per cent during 2022-23.

Transmission

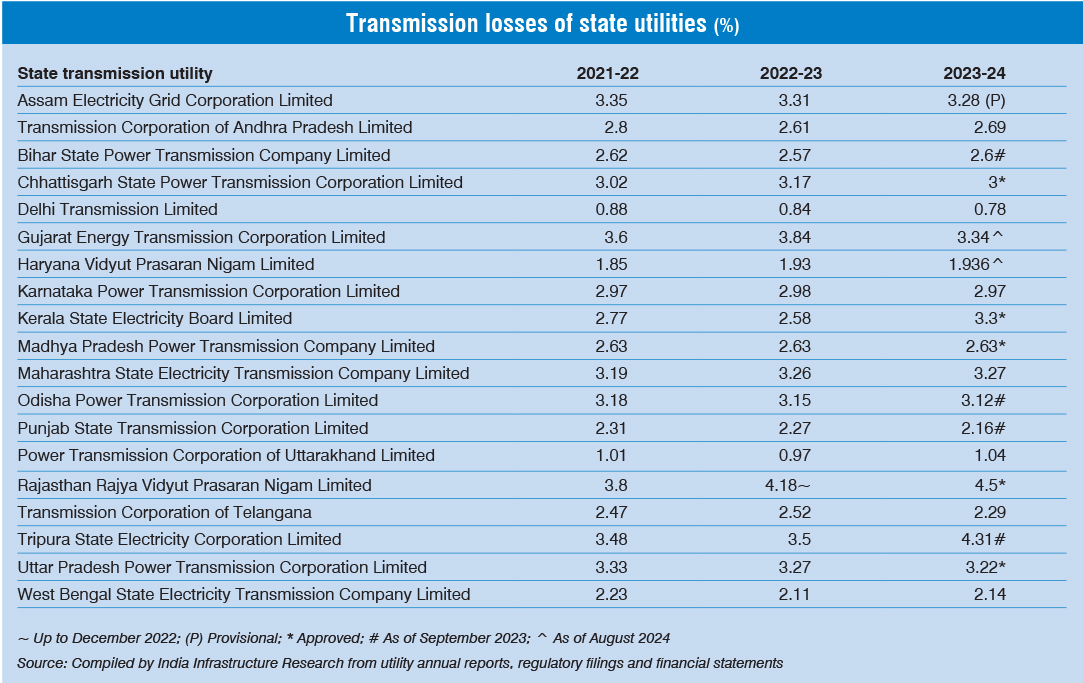

The performance of state transmission utilities exhibited a mixed trend in 2023-24, with utilities tracked by Power Line Research reporting transmission losses in the range of 0.78 per cent for Delhi Transmission Limited (DTL) to 4.5 per cent (approved) for Rajasthan Rajya Vidyut Prasaran Nigam Limited (RRVPNL) during 2023-24.

Of the 19 utilities for which data is available for 2023-24, nine registered a decline in their transmission losses over the previous year. Meanwhile, nine other utilities – RRVPNL, Tripura State Electricity Corporation Limited, Maharashtra State Electricity Transmission Company Limited, Kerala State Electricity Board Limited (KSEBL), Transmission Corporation of Andhra Pradesh Limited (AP Transco), Power Transmission Corporation of Uttarakhand Limited (PTCUL), Bihar State Power Transmission Company Limited (BSPTCL), Haryana Vidyut Prasaran Nigam Limited (HVPNL), and West Bengal State Electricity Transmission Company Limited (WBSETCL) – registered an increase. One utility, Madhya Pradesh Power Transmission Company Limited (MPPTCL), did not register any change.

Among the utilities tracked, DTL reported the lowest transmission losses at 0.78 per cent, followed by PTCUL at 1.04 per cent and HVPNL at 1.94 per cent (as of September 2023). Meanwhile, Chhattisgarh State Power Transmission Corporation Limited, Transmission Corporation of Telangana, AP Transco Limited, Karnataka Power Transmission Corporation Limited, MPPTCL, WBSETCL, Punjab State Transmission Corporation Limited and BSPTCL recorded losses of 2-3 per cent during 2022-23. The remaining state transcos reported losses in the range of 3.12-4.5 per cent, including state utilities of Assam, Gujarat, Kerala, Rajasthan, Tripura, Uttar Pradesh, Odisha and Maharashtra. The transco with the highest loss of 4.5 per cent (approved) was RRVPNL.

Distribution

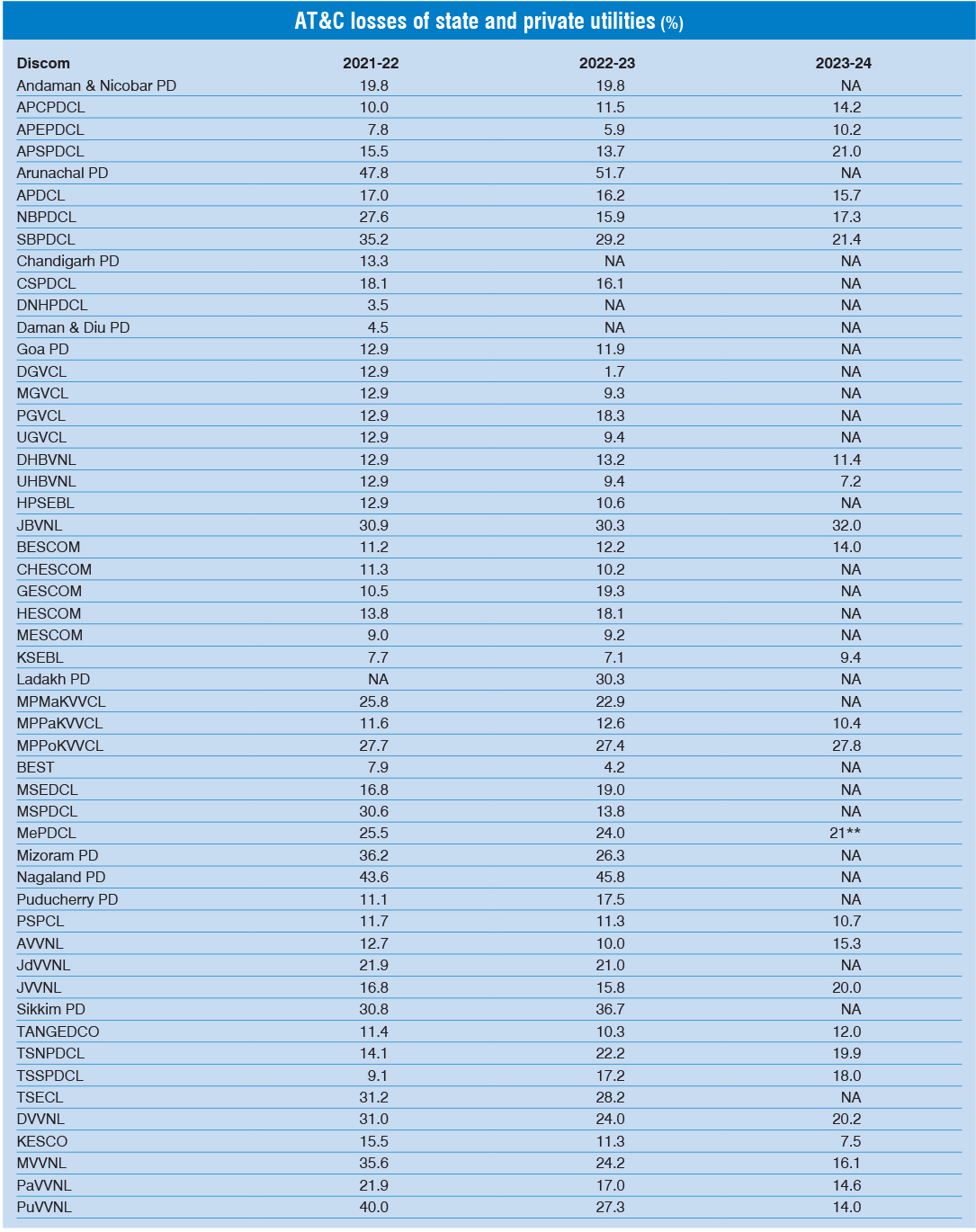

Data was collated by Power Line Research for 64 discoms (51 state-owned distribution utilities and 13 private utilities) from tariff orders, the BEE energy audit report and company reports. It was observed that among the state utilities, AT&C losses ranged from as low as 1.68 per cent for Dakshin Gujarat Vij Company Limited (DGVCL) to as high as 51.7 per cent for the Power Department of Arunachal Pradesh during 2022-23. A total of 43 state utilities reported a decline in AT&C losses during 2022-23 compared to 2021-22. The most significant improvements were reported by TP Central Odisha Distribution Limited, DGVCL, Madhyanchal Vidyut Vitaran Nigam Limited (MVVNL), North Bihar Power Distribution Company Limited, Purvanchal Vidyut Vitaran Nigam Limited (PuVVNL) and Manipur State Power Distribution Company Limited, which reported a reduction of 16-11 percentage points in AT&C losses.

Among the state utilities, DGVCL was the best performer, with AT&C losses of 1.68 per cent during 2022-23. In addition, 21 state-owned utilities reported/estimated AT&C losses of less than 15 per cent during 2022-23. These are DGVCL, Brihanmumbai Electricity Supply and Transport Undertaking, Andhra Pradesh Eastern Power Distribution Company Limited (APEPDCL), KSEBL, Mangalore Electricity Supply Company Limited, Madhya Gujarat Vij Company Limited, Uttar Gujarat Vij Company Limited, Uttar Haryana Bijli Vitran Nigam Limited (UHBVNL), Ajmer Vidyut Vitran Nigam Limited, Chamundeshwari Electricity Supply Corporation Limited, Tamil Nadu Generation & Distribution Corporation Limited (TANGEDCO), Himachal Pradesh State Electricity Board Limited, Punjab State Power Corporation Limited (PSPCL), Kanpur Electricity Supply Company Limited (KESCO), Andhra Pradesh Central Power Distribution Corporation Limited (APCPDCL), Goa Power Department, Bangalore Electricity Supply Company Limited (BESCOM), Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (MPPoKVVCL), Dakshin Haryana Bijli Vitran Nigam Limited (DHBVNL), Andhra Pradesh Southern Power Distribution Company Limited and Manipur State Power Distribution Company Limited. The worst performing state-owned utilities during 2022-23 were the Arunachal Power Department, the Nagaland Power Department and the Sikkim Power Department, with AT&C losses of 51.7 per cent, 45.81 per cent and 36.69 per cent respectively.

Meanwhile, private sector discoms continued to report steady performance, with losses of less than 10 per cent over the past couple of years. Only the four Odisha discoms acquired by Tata Power during 2019-20 and 2020-21 reported losses of 17-31 per cent. In Gujarat, the AT&C losses of Torrent Power-Surat and Torrent Power-Ahmedabad stood at 3.69 per cent and 4.04 per cent, respectively. Meanwhile, AEML reported AT&C losses of 6.48 per cent during 2022-23. Among the Delhi discoms, Tata Power Delhi Distribution Limited (TPDDL) recorded AT&C losses of 6.98 per cent, whereas BSES Rajdhani Power Limited (BRPL) and BSES Yamuna Power Limited (BYPL) recorded AT&C losses of 7.16 per cent and 7.25 per cent, respectively. Meanwhile, Noida Power Company Limited, India Power Corporation Limited and Calcutta Electric Supply Corporation recorded AT&C losses at 8.36 per cent, 6.56 per cent and 8.28 per cent, respectively.

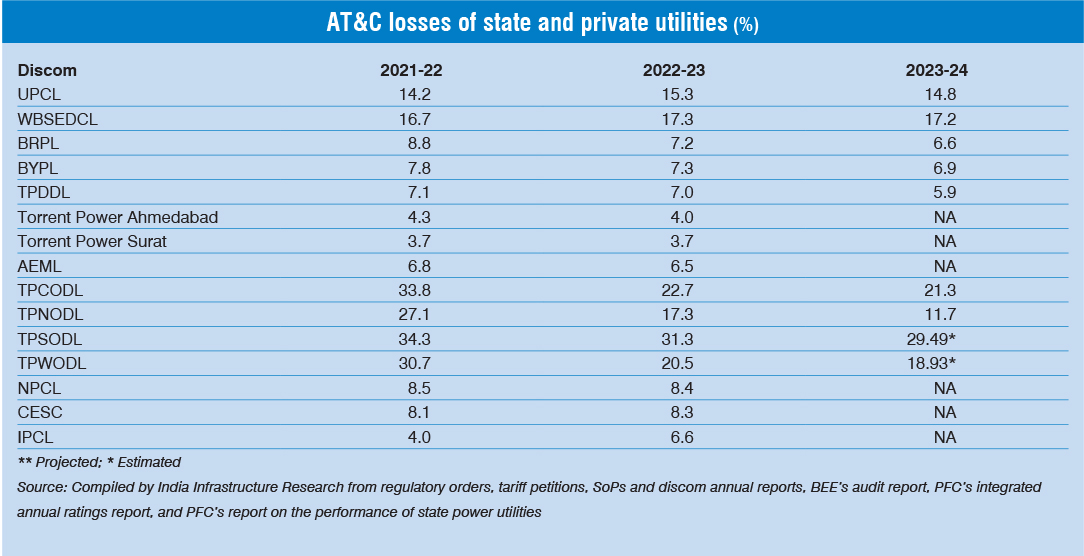

Data was compiled by Power Line Research for 34 discoms, including 27 state-owned and seven private utilities, using information from tariff orders, the BEE energy audit report and company reports. Among state utilities, AT&C losses in 2023-24 ranged from a low of 5.9 per cent for TPDDL to a high of 32.04 per cent for JBVNL. Notably, 22 state utilities saw a reduction in AT&C losses compared to 2022-23, with the most significant improvements observed in PuVVNL, MVVNL, SBPDCL and TP Northern Odisha Distribution Limited, which reduced losses by 5-13 percentage points.

UHBVNL emerged as the top performer, with AT&C losses of 7.19 per cent in 2023-24. Additionally, 13 state-owned utilities recorded or estimated losses below 15 per cent, including UHBVNL, KESCO, KSEBL, APEPDCL, Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited, PSPCL, DHBVNL, TANGEDCO, BESCOM, PuVVNL, APCPDCL, Pashchimanchal Vidyut Vitaran Nigam Limited and Uttarakhand Power Corporation Limited. The worst performers were JBVNL, MPPoKVVCL and SBPDCL, with losses of 32.04 per cent, 27.78 per cent and 21.42 per cent, respectively. In the private sector, discoms generally reported a decline in losses. The four Odisha discoms acquired by Tata Power had losses between 11 per cent and 29 per cent. In Delhi, TPDDL recorded losses of 5.9 per cent, while BRPL and BYPL reported losses of 6.6 per cent and 6.9 per cent, respectively.

Conclusion

The performance of India’s power utilities in 2023-24 underscores both advancements and persistent challenges. The generation segment saw an encouraging rise in PLFs, particularly in the central and state sectors, driven by increased power demand. However, transmission losses varied across states, reflecting a need for further improvements in efficiency. In distribution, the reduction in AT&C losses for a majority of state utilities is a positive trend, though certain utilities still lag behind. Private sector utilities continue to show steady performance, especially in the distribution space.

Moving forward, the government’s Revamped Distribution Sector Scheme is expected to strengthen the distribution network and improve the operational and financial performance of utilities. Additionally, the implementation of the Late Payment Surcharge Rules will help discoms in clearing their outstanding dues through equated monthly instalments, thereby enhancing the financial position of the segment, which has historically been the weakest link in the electricity value chain.

Akanksha Chandrakar