The Reserve Bank of India’s (RBI) February 2018 circular, Resolution of Stressed Assets – Revised Framework, is expected to push the gross non-performing assets (NPAs) of banks to the north of Rs 9 trillion. The stress in coal-fired thermal power capacity has increased to an alarming level due to reasons pertaining to poor feedstock policies, power purchase agreement (PPA) issues, inefficient monitoring and credit lending, unviable tariffs, etc. With this background, the power sector is expected to lead the list of bank NPAs. In this article, we will cover on-ground power demand-related aspects, NPA issues, the RBI circular and its impact, stakeholder views and Deesha Power’s recommendations on value unlocking. To start with, let’s look at power purchase-related aspects and realistic options therein.

Realistic power purchase by discoms

Historically, power purchase by discoms has been governed by three factors, namely demand growth and load shedding, power exchange prices, and the discoms’ financial health. Of late, there has been an improvement on all the factors, as mentioned below:

- Increasing economic activity and ease of access to electricity in rural areas with the prime minister announcing the achievement of the 100 per cent village electrification target.

- Rising power prices on the power exchange (round-the-clock average price of Rs 3.26 per kWh for 2017-18 and Rs 4.27 per kWh for year to date May 24, 2019), which will force discoms to opt for more stable, cheap and reliable power through medium/long-term PPAs.

- Reduction in the gap between the average cost of supply (ACS) and the average revenue realised (ARR), which has came down from Rs 1.27 per kWh in 2012-13 to Re 0.43 per kWh in 2017-18.

This will drive power purchase by discoms, going forward. Further, experts paint a scenario where with greenfield thermal power supply choking and double-digit demand growth, the demand-supply gap could increase and power planners will be left with brownfield stressed thermal capacity. Such brownfield plants could supply power not only when solar is unavailable in the system, but also on a 24×7 basis. A country with a GDP of over $2 trillion definitely requires reliable and quality power supply to drive its growth. In such a scenario, the resolution of stressed power appears to be a national requirement.

NPA issue: Size and genesis

A report of the Parliamentary Standing Committee on Energy has identified 34 coal-fired thermal power plants (TPPs) as stressed cases. Till June 2017, the total gross loan to the sector stood at Rs 5.69 trillion, of which total NPAs accounted for 18 per cent, including restructured standard advances. Of the total NPAs, the generation segment accounted for a 91 per cent share, followed by distribution and transmission with a 6 per cent and a 3 per cent share respectively.

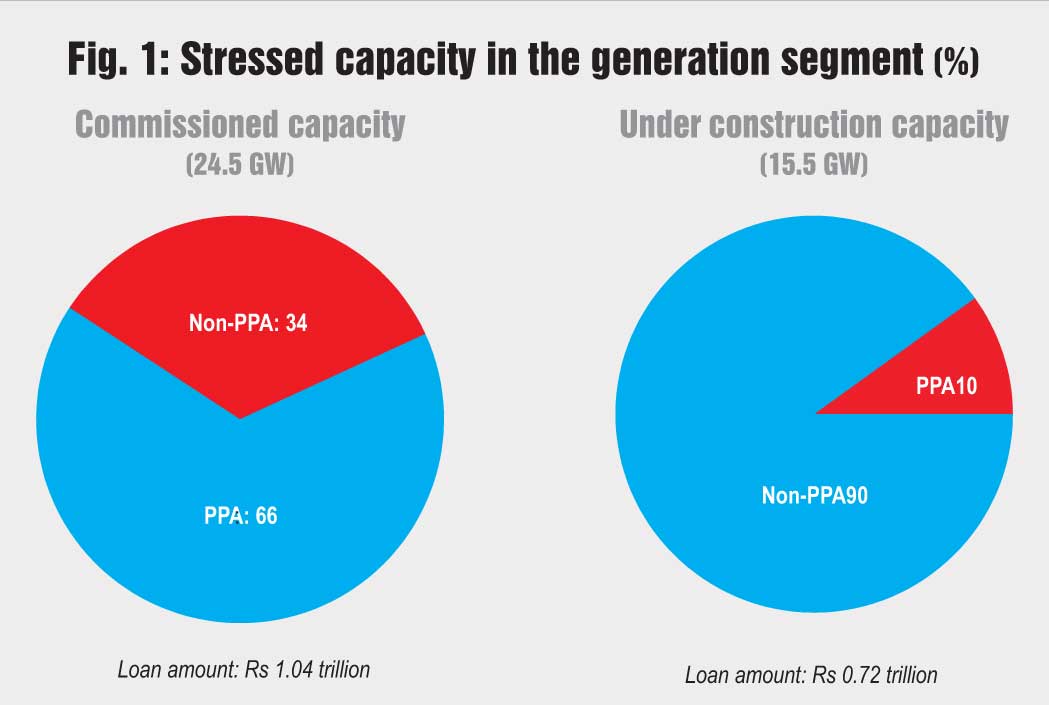

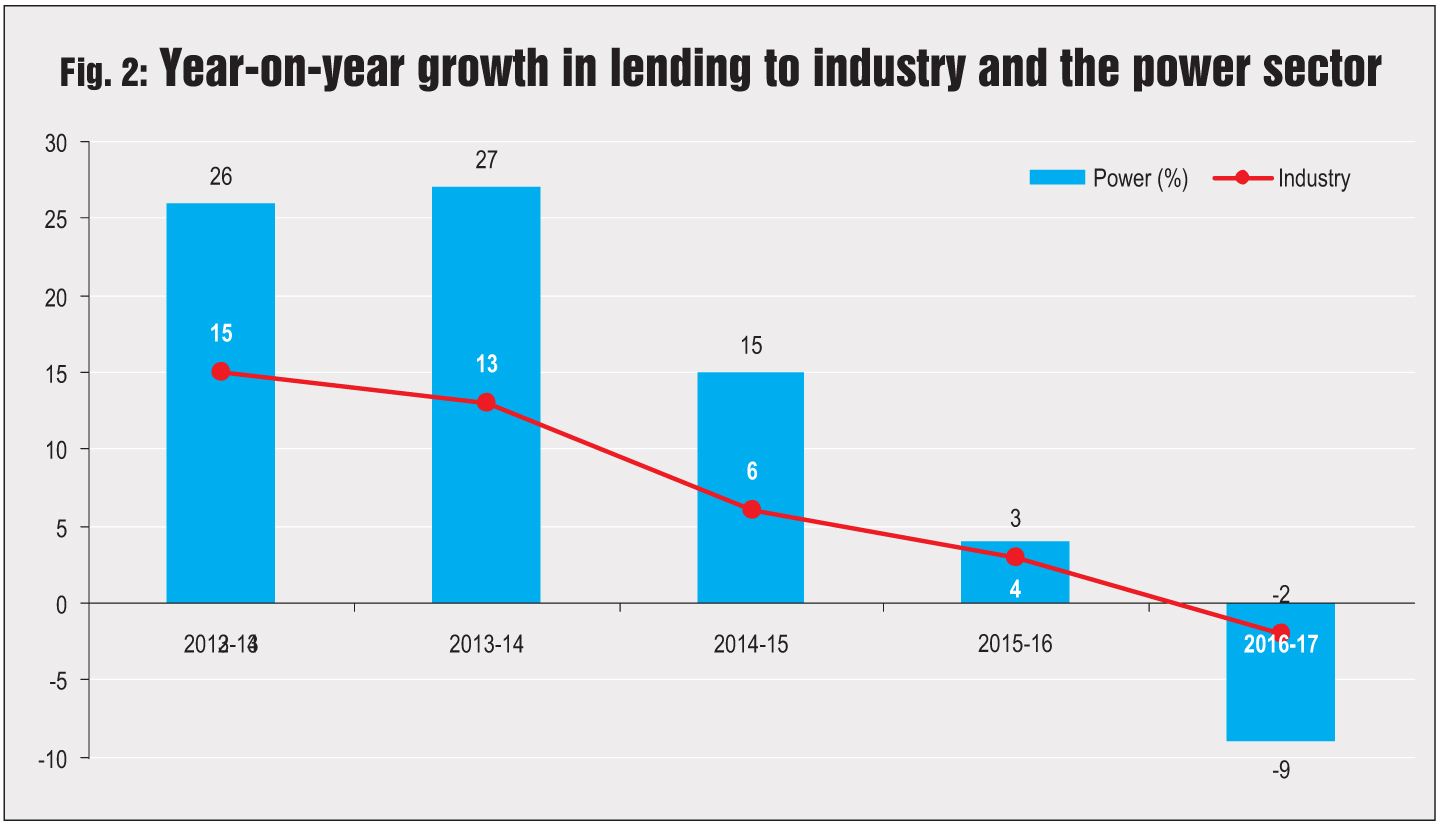

The total stressed TPP capacity is estimated at 40 GW with an outstanding debt of Rs 1.76 trillion. This is further bifurcated in Fig. 1. Almost 90 per cent of the under construction capacity is without PPAs, which is unlikely to be addressed easily. Some of the major reasons for stress are non-availability of coal due to coal block cancellations or no linkages, no PPAs, unviable tariffs and poor financial health of discoms. In addition, promoters’ inefficiency to infuse equity and low off take are making projects unviable. Higher-than-normal credit flow to the power sector was observed during 2012-13 to 2014-15, as seen in Fig. 2. Tight monitoring could have reduced the severity of bad loans by at least 30-40 per cent.

Impact of RBI’s circular

The RBI notification mandates banks to categorise even one day of delay in debt servicing as default. Experts opine that even better positioned power plants are finding it difficult to service their debt due to high receivables from financially weak discoms. The move is likely to impact more than 51 GW of existing capacity and 28 GW of under construction capacity. New regulations disincentivise any loan restructuring and push for the sale or change of control of any stressed assets, thereby increasing the risk for developers and equity investors in a short-term scenario. The debt servicing capability has been greatly affected with regulators not permitting pass-through of coal costs to developers owing to the following coal-related issues:

- Coal India supplies only 60 per cent of the coal required to supply power as per the PPA (quantity variation)

- Higher price of coal procured through e-auctions (rate variation).

- Under these circumstances, experts opine that a debt haircut of at least 35 per cent seems to be a viable option towards resolution.

- Stakeholder views

- The views of stakeholders, including banks, asset reconstruction companies (ARCs), special situation funds, original equipment manufacturers (OEMs), independent power producers (IPPs) and regulators were sought through a structured questionnaire. It’s summary is given below:

- Sector issues coupled with the limited availability of options for disposal are the main challenges for revival

- The execution of a resolution plan is likely to face bottlenecks in the form of difficulty in raising funds and limited bidders

- Fear of vigilance action coupled with banks having small exposures holding on to better deals are major bottlenecks for driving revival proceedings by banks

- RBI’s circular will deal flow but the absence of a revival ecosystem could choke its speed

- Adopting a patient approach for absorbing losses arising out of restructuring coupled with sectoral reforms in distribution could help in the long term.

Some suggestions for the revival of stressed power assets received during primary interactions with stakeholders are:

Some suggestions for the revival of stressed power assets received during primary interactions with stakeholders are:

“Give more time to banks (say four to eight quarters) to absorb losses arising out of actions (restructuring, sale of assets, etc.) to revive the unit. This will enable them to realise more value and find meaningful solutions. Issues related to the distribution segment, like open access, should be addressed.” Chief executive officer (CEO) of a leading ARC

“Provide more flexibility for lender haircuts and a better-defined approach where there is serious emphasis on completing resolution plans and revival of companies before reaching the National Company Law Tribunal (NCLT). The number of cases going to the NCLT should be greatly reduced and the aim should be to find a resolution outside the NCLT.” Senior vice-president of an investment bank

“Retire environmentally non-compliant capacity. State gencos, backed by their respective governments, in view of their ageing installed capacities could consider taking equity in stressed projects.” CEO of an IPP

“The National Investment and Infrastructure Fund (NIIF) along with NTPC and Bharat Heavy Electricals Limited could identify 10 GW of capacity with the intent of revival. Special medium/ long-term power purchase or tolling programmes by discoms targeting stressed capacities should be introduced.” Partner of an infrastructure fund

Deesha Power’s recommendations

Deesha Power’s recommendations

- Low-hanging fruit may be identified and an exercise to develop asset-specific strategy should be undertaken, as different assets have different types of challenges

- The NIIF, along with central public sector units, could take decisive steps for the resolution of stressed capacity

- Old, inefficient and environmentally non-compliant capacity may be retired on priority

- A mechanism needs to be developed to ensure that revivable stressed capacity is put to use. A tolling arrangement and the DEEP (Discovery of Efficient Electricity Price) portal can provide a better platform for revival

- Anti-dumping duty, collected from Chinese imports, could be used for establishing the viability of domestic solar manufacturing capacity

- Some value-unlocking options could be “as is” sale, sale to an ARC, sale to a financial investor/strategic investor, NIIF revival and lender revival

- Selling assets without any value addition would attract a steep discount from the buyer

- Resolution strategies should depict realistic value-unlocking options related to the project.

Conclusion

With demand increasing and exchange prices firming up, there will be a requirement for 24×7 reliable and quality power supply. Stressed thermal assets are best suited to meet this systemic requirement. Through this article, it is our sincere objective to share the thought process with people at large and seek a consensus on a resolution of stressed assets.